The Color of Money

USDT, USDC, USDS stablecoin business models side by side

For the avoidance of doubt, in this article we use the term 'fractional reserve' to refer to stablecoins that hold a portion of their reserves in non-cash assets such as commercial paper, secured loans, commodities, or other yield-generating instruments. This does not imply undercollateralization or insolvency.

By reserve we refer to the proportion of assets that are cash equivalent or fully liquid:

Full reserve: only cash

Fractional reserve: not only cash

No reserve: only not cash

Insolvent: undercollateralized (algorithmic, endogenously collateralized, etc)

tldr

Taking advantage of uneventful slow news days, we analyzed different stablecoin business models, comparing full vs fractional reserve balance sheets. Using data from Tether, Circle and Sky, we showcase how return on equity differs based on balance sheet structure.

While much attention has focused on regulatory compliance and technical risks, less analysis has been done on their economics and long-term sustainability. This piece provides a framework for evaluating stablecoin business models through the lens of return on equity (ROE), revealing tradeoffs between liquidity, profitability, and growth.

Full reserve stablecoins need long-term non-interest income to be sustainable

Fractional reserve stablecoins trade liquidity for surplus accumulation

Return on equity decomposition reveals the impact of these tradeoffs

These ROE differences highlight a tension in stablecoin design: full reserve models like Circle prioritize liquidity but struggle with profitability, while fractional reserve models like Tether achieve higher returns but take on more risk. This suggests the stablecoin market may segment into different tiers for different use cases.

The tradeoffs of different stablecoin business models

Prior work: Cryptodollars and the hierarchy of money (Substack, SSRN), Operating Manual for Decentralized Stablecoins v1 (Steakhouse)

Stablecoins are on-chain liabilities that promise to maintain value relative to a reference asset, with cryptodollars a subset of stablecoins that are redeemable at par for higher-level money. They come in three main types:

Full reserve (like USDC): Fully backed by liquid assets (e.g. bank deposits, Treasury bills, overnight repo, or directly convertible instruments like fiat-backed stablecoins)

Fractional reserve (like Tether and USDS): Partially invested in higher-yielding, less liquid assets

No-reserve (like LUSD): Credit-based instruments without direct fiat backing

As described in our Stablecoin Operating Manual1, a stablecoin can be approximated by an optimization problem:

Maximize return on equity

subject to constraints of liquidity and solvency

where user demand for a stablecoin = monetary yield + non-monetary (utility) yield

Many paths exist to maximize return on equity. It’s reasonable to trade-off short-term profitability for long-term balance sheet growth. It’s reasonable to take higher risk/return on reserves as long as liquidity and solvency are not compromised. Full versus fractional distinctions describe the limitations that stablecoins may choose in pursuit of those goals.

Full reserve stablecoins serve users that value liquidity over other features. As the likelihood of generating sustainable yield from reserves is lower, full reserve stablecoins should prioritize adjacent business models that can create long-term non-interest income, including fees on transaction volume, platform-type services like APIs,or additional credit businesses down the money hierarchy that can generate wider spreads. Circle’s acquisition of Hashnote and its focus on building SDKs2 is coherent with that goal.

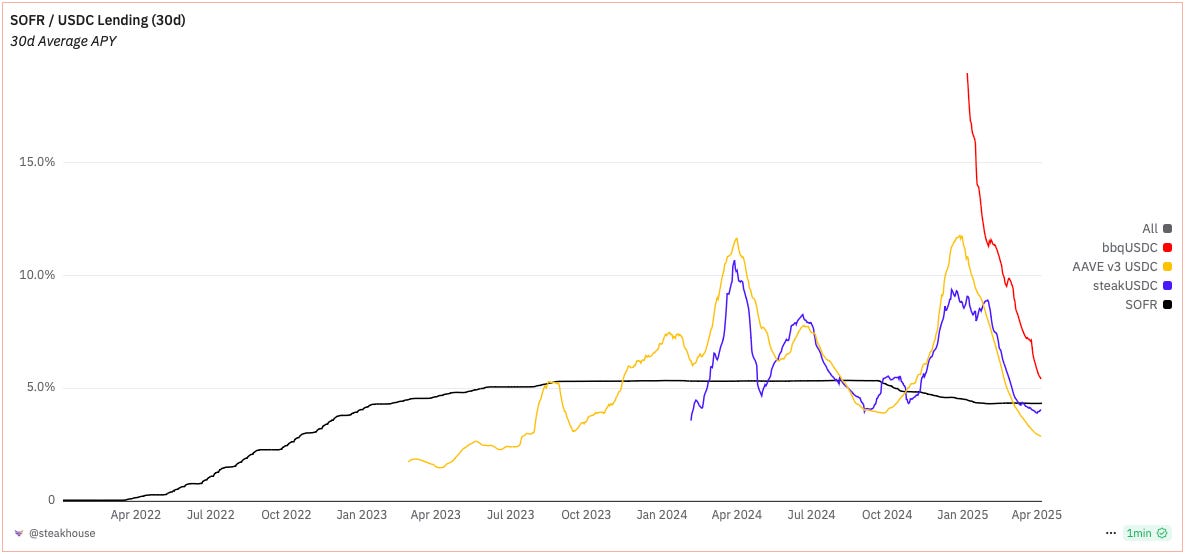

Fractional reserve stablecoins accept some liquidity risk by investing in less liquid but higher-yielding assets. This creates a positive spread to earn a surplus against potential losses or pay for a competitive funding rate. In traditional banking, asset-liability management committees regularly review expected deposit outflows over the next 30d, allowing liquidity reallocation if user behavior is expected to remain stable. The same principle applies to a fractional reserve stablecoin, with the added benefit of visible on-chain user interaction history for more precise estimation.

Common size comparison of major stablecoins

Based on Tether’s attestations, Circle’s S-1 filing, and our Dune dashboards for Sky, we show a simplified comparison of key financial metrics for the three major stablecoins. A caveat: Tether doesn’t disclose its operating expenses. We conservatively assume it’s 2x Circle’s total operating expenses based on the relative balance sheet sizes (ca. $1bn a year). This is likely overstated due to significant operating leverage possible on scaling a balance sheet through stablecoin liabilities.

Liquidity Management

Circle’s gross interest income from liquid reserves appears low. Sky, being an on-chain protocol, expects full exposure to the Federal Funds rate to be difficult, especially as it has to channel it through USDC. However, Circle generated approximately 4.75% on its liquid reserves in 2024, compared to Tether’s 7% (based on $7bn reported returns from “Treasuries and repo agreements” and a $100bn average asset balance). The definitions of cash & equivalents matter. Both Circle and Tether overindex on cash or Treasury securities with less than 90d maturity, but 7% in 2024 was objectively high-yield and likely not achievable with low-risk Treasuries and repo agreements alone.

Tether has been unwinding bank deposits since December 2022 and seems to have succeeded. This mitigates credit risk from a bank deposit institution and offers more competitive yield advantages without increasing liquidity risk. However, we’d welcome more detail on the overall return composition, as 7% on low-risk money market instruments seems unlikely, and the cash & equivalents book may contain more risk - or we misunderstood the asset base. Both scenarios would resolve with greater disclosure.

Long-term investments

The key distinction between Tether and Sky as fractional reserve systems is that Sky’s is user-driven. Crypto rates are largely uncoupled from traditional rates. When liquidity enters the on-chain economy, speculative activity increases, driving rates higher. When people take out crypto-backed loans from Sky through a core vault or sub-DAOs like Spark, liquidity is reallocated away from cash to borrowing.

For a constant demand for the stablecoin:

Borrower collateralizes loan with wstETH

Borrower takes out USDS loan

Borrower sells USDS to create the position (to lend at a higher rate or purchase more collateral and repeat)

Downward pressure on USDS secondary market price incentivizes arbitrage out of cash & equivalents

Cash & equivalents is reallocated to secured loans

Crypto-backed loans are fully secured, as user equity serves as the first buffer for liquidations if the collateral price declines and the loan needs to be cured. We consider them in the same category as Tether’s Secured Loan portfolio, though the collateral composition is likely different.

In December 2022, Sky faced the bottom of the bear market after FTX’s collapse. By 2024, animal spirits had returned and increased the proportion of USDS minted from crypto-backed loans versus USDC or real-world assets. If the crypto market declines in 2025, we expect the balance sheet to swing back to cash & equivalents or originate secured loans in the real world that can earn a positive spread over the risk-free rate without being collateralized by crypto.

Tether’s returns have a large component from unrealized mark-to-market gains in commodity reserves. In 2024, nearly half the total return came from unrealized P&L on gold and bitcoin. Commodity reserves provide a useful source of diversification, which, if sufficiently liquid, can serve as good reserve assets. However, their performance in a downturn if unhedged is uncertain. Some return tradeoff may be worthwhile to insure the portfolio against market downturns that can worsen if Tether has to rapidly liquidate reserves to remain overcollateralized.

You can’t escape ROE

In summary, we see the impact of collective decisions on the decomposition of sources of return on equity:

1. Net interest spread

Tether and Sky have competitive returns on assets, in line with a cash & equivalents and secured loans portfolio. Sky faces a higher monetary funding cost, which is part of the value proposition that makes USDS appealing. If fewer USDS tokens than 100% convert to the rewards-bearing version, Sky can waterfall the difference to equity or increase the savings rate. Tether’s lack of funding cost (a big assumption) illustrates its dominance in network effects and utility.

Circle’s balance sheet seems expensive from a funding cost perspective. Consistent with its strategy of becoming a platform rather than a unit of account for users, the funding cost is distributed to channel partners, who can use the proceeds to reward users or reinvest in platform products using USDC. However, it leaves a large gap to cover as the remaining spread is quite shallow.

2. Other changes to return on assets

Tether adds kerosene to this return through unrealized P&L recognized in non-interest income. This could be positive or negative, representing the largest source of solvency and liquidity risk in our view. For instance, YTD, the portfolio’s unrealized P&L is down ~$650m (increase in gold M2M of ~$750m and decrease of bitcoin M2M of ~$1.4bn). Neither Circle nor Sky have meaningful non-interest sources of income in 2024 or commodity reserves.

None of the stablecoins provision for credit-related losses, though it is implied in all that the surplus is partly there to buffer against losses.

From an operating expense perspective, we can only assume Tether’s spend, while we can review Circle’s S-1 or our Dune dashboards for Sky. Even assuming Tether spent 2x on total operating expenses as Circle, given the size of its balance sheet, this represents a smaller proportion of assets overall.

3. Balance sheet leverage

Finally, on leverage, Tether appears prudently levered. For average equity, we take the previous year’s ending equity and add the operating income, prior to distributions within Tether Group. Circle’s balance sheet is more levered than Tether and could be much higher given the low-level of risk. Sky can afford a very high degree of balance sheet leverage as user equity isn’t counted in the surplus, i.e. secured loans hit user collateral with considerable margin before hitting the Sky surplus. This is one illustration of capital efficiency from the stablecoin point of view, a distinct advantage of decentralized crypto stablecoins. This level of leverage would be practically impossible without total transparency for users. Thankfully, as Sky is fully on-chain, so its economic position is available to anyone at any time.

What value?

The question of valuation is still open for debate. All stablecoins are relatively new in capital markets, so there’s no track record of what is ‘fair’ value. Furthermore, the largest stablecoin (Tether), is privately owned, making peer comparison difficult.

Price to Book isn’t suitable as stablecoins can be lightly capitalized. Price to assets depends on asset monetization perspectives, which may differ between full reserve and fractional reserve stablecoins. Price to Operating Income or Earnings has distortions, like non-interest income, making comparison difficult. New reasoning may be needed to find a suitable valuation framework for stablecoins and investors.

Endnotes

Sources

Tether operating expenses assumed 2x Circle

Disclaimer

The information contained in this analysis is provided for general informational purposes only and is not intended to be, and should not be relied upon as, legal, financial, or professional advice. Steakhouse Financial assumes no liability or responsibility for any errors or omissions in the content of this assessment or for any actions taken based on the information provided herein.

This analysis is based on the information available at the time of its preparation and is subject to change without notice. The assessment is not a guarantee of future performance or results, and past performance is not necessarily indicative of future results.

You should seek professional advice from a qualified attorney or financial advisor before making any decisions or taking any actions based on the information contained in this assessment. Steakhouse Financial disclaims all liability and responsibility for any actions taken or not taken in reliance on the information contained in this analysis.