DeFi Markets Update 2026-05-19

Grove Basin, Lending Market Divergence, AUSD Opportunities

Welcome to another DeFi Markets Update—your no-nonsense briefing on the cryptobanking plumbing and market pulse.

More Products, More Growth for Grove

Grove, the institutional credit infrastructure protocol within the Sky ecosystem, has grown to more than $2.5bn in TVL and continues expanding across both onchain savings and tokenized real-world asset infrastructure.

Last week, Grove introduced Basin, a programmable liquidity layer for tokenized real-world assets. It gives eligible holders instant onchain stablecoin liquidity when they redeem, sell, or transfer supported RWAs instead of the traditional redemption wait lockup.

Tokenized Treasuries and money market funds can move onchain 24/7, but redemption still follows traditional finance settlement timelines of 1-2 days wait. Basin finances the settlement timing gap while the relevant fund, issuer, transfer agent, broker-dealer, or tokenization platform completes its existing workflow.

Over time, Basin may extend across tokenized credit assets including investment-grade bonds and private credit. Grove is starting with Treasury and MMF products first because they are liquid, operationally mature, and institutionally adopted.

Furthermore, a new rewards program is launching this week. Users who supply USDS or USDC through Grove Savings on Ethereum to mint sUSDS will begin accruing Grove Points when the program goes live on 21 May at 9am ET.

Points accrue proportionally to a wallet’s share of total sUSDS minted through Grove Savings and are tracked through Grove’s referral code infrastructure inside the Sky ecosystem.

Diverging Capital Flows Across Lending Markets

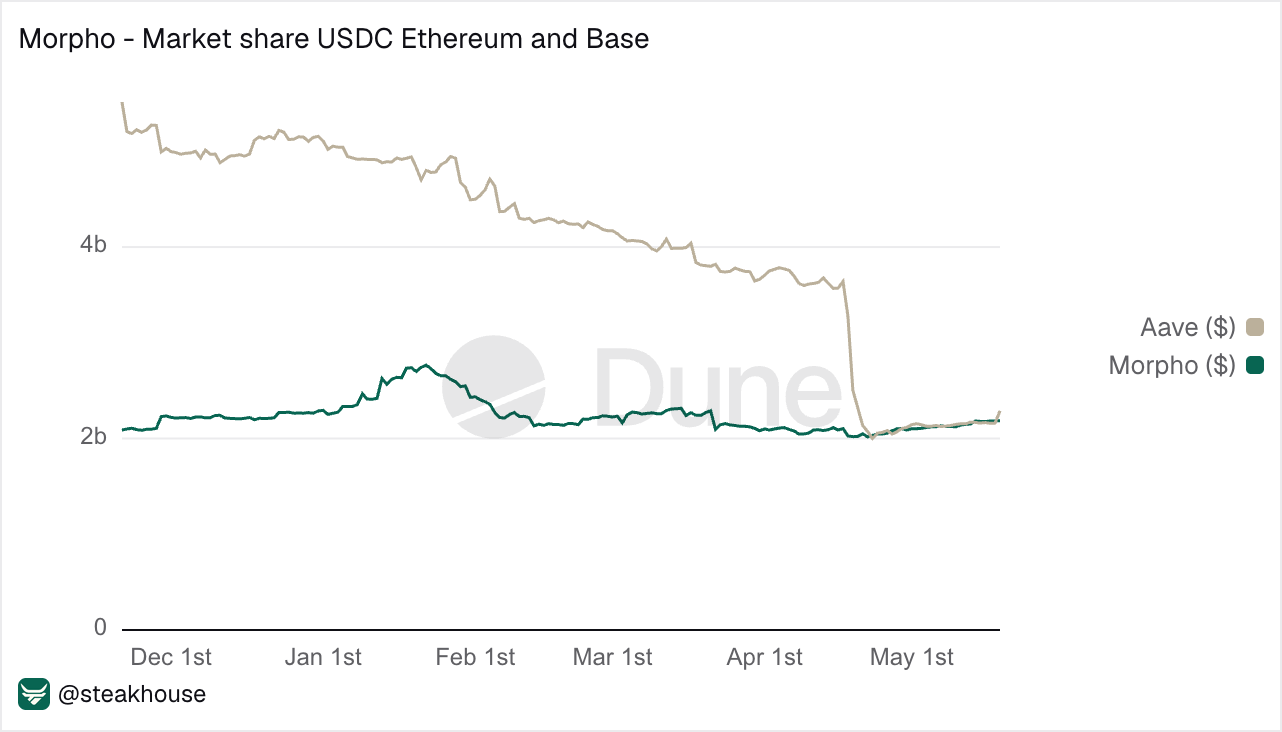

Lending venue preference appears to have shifted after the 18th of April KelpDAO/ LayerZero exploit, with users moving away from pooled lending exposure and into more isolated market structures. For comparison, aggregate USDC market size across Mainnet and Base is now similar between Morpho and Aave.

Overall, in total size Morpho has continued growing this quarter and over the past 90 days, Morpho TVL is up 29%.

In contrast, Aave TVL is down by around 45% over the same period, with roughly $18bn leaving since 18th of April.

Isolated market design allocates capital across separate vaults and markets rather than one shared pool. Each market has its own collateral exposure and risk profile, making risk easier to contain. [read more here]

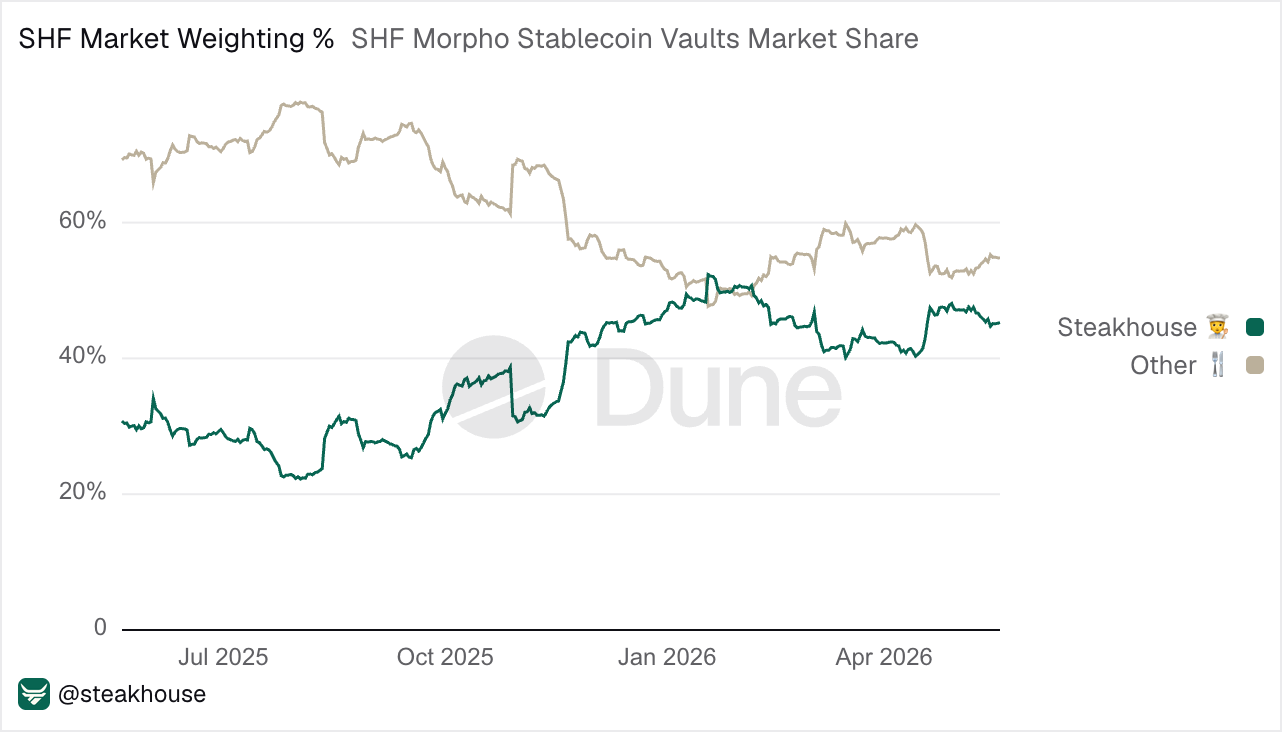

Risk on Morpho still depends on the curator. Curators choose collateral, manage allocations, and define each vault’s risk-return profile. Steakhouse, the leading curator, currently curates more than 45% of Morpho stablecoin vault market share, giving users a broad set of vaults across different risk profiles and return targets.

AUSD Opportunities Across Chains

Agora’s dollar stablecoin vaults curated by Steakhouse have continued earning above 8% APY for several months, supported by sustained borrow demand and ongoing incentive programs across multiple markets.

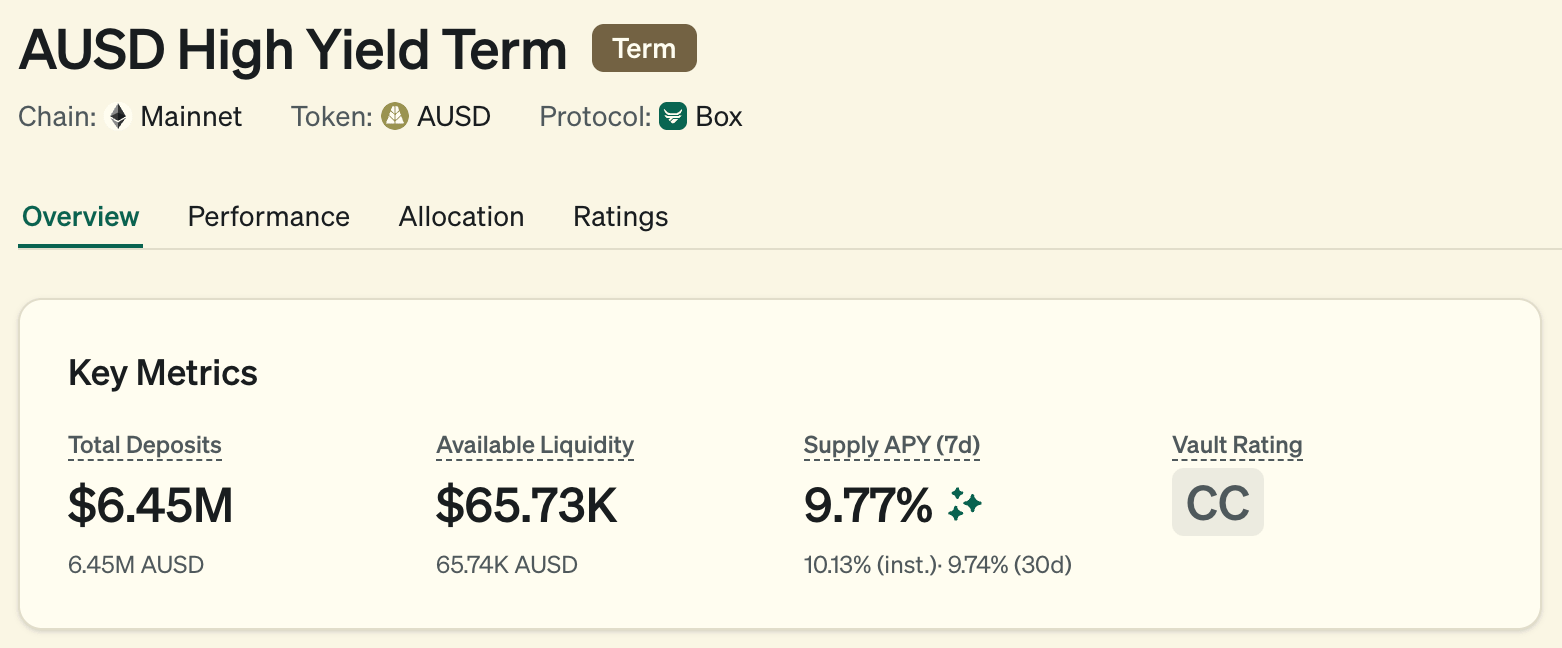

On Ethereum, the AUSD High Yield Term Vault on the Steakhouse App combines organic lending strategies earning around 4–5% with an additional ~5% in AUSD incentives, bringing total vault APY close to 10%.

Term strategies are built using Steakhouse Box adapters and hold direct positions to underlying assets. [read more here]

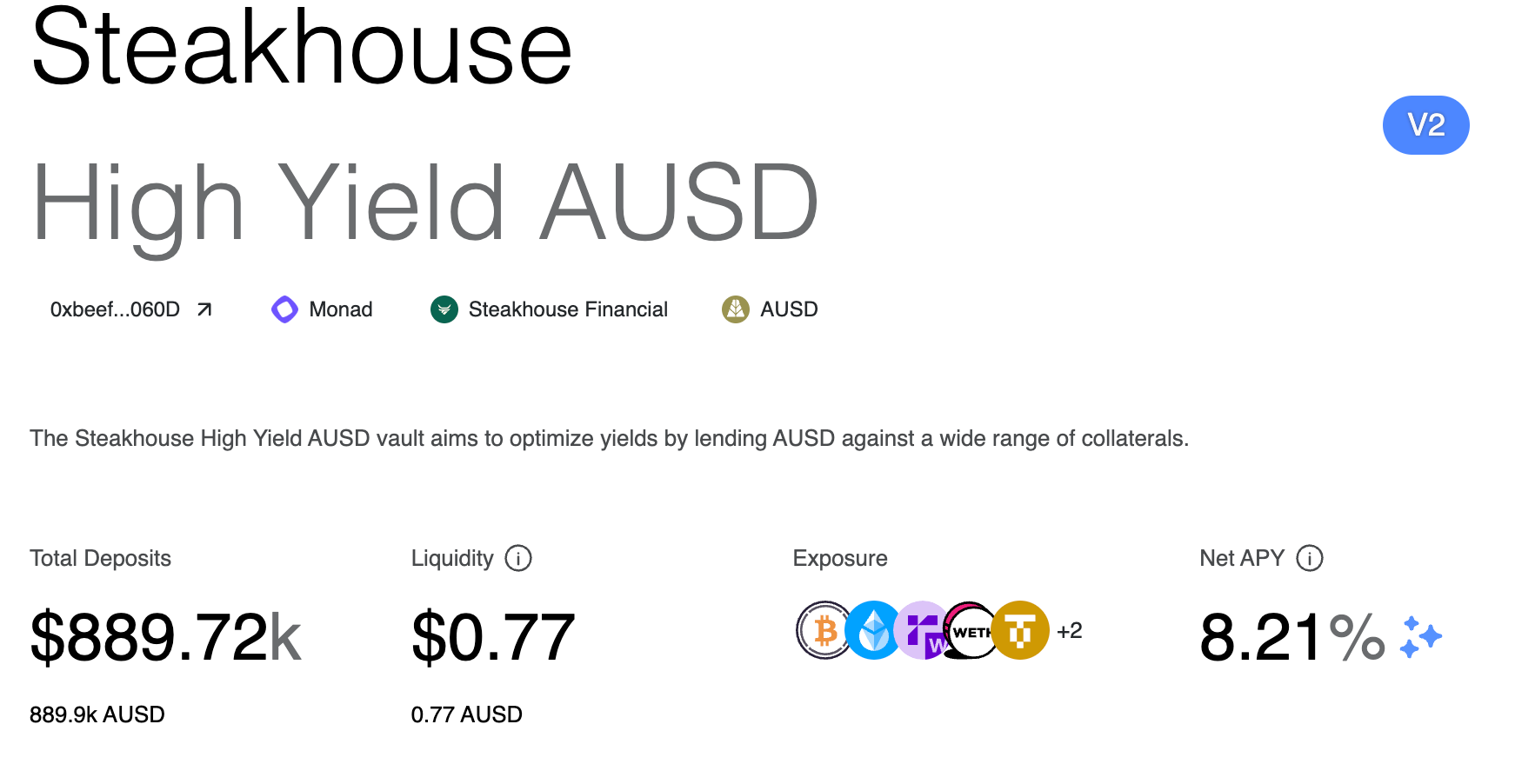

On Morpho Monad, the High Yield AUSD vault has averaged roughly 7% organic APY over the past three months. Current MON incentives add another ~2%, pushing net vault yield toward 8-9%.