DeFi Markets Update 2026-03-05

The Steakhouse App, Stablecoins: plumbing of the financial cycle, Negative Borrow rates on Katana

Welcome to another DeFi Markets Update—your no-nonsense briefing on the cryptobanking plumbing and market pulse.

The Steakhouse App Is Live

We launched our new App, bringing all Steakhouse curated vaults into a single interface where users can allocate capital across Morpho strategies with full visibility into collateral composition, LLTV thresholds, liquidity, and historical APY before deploying capital.

Alongside existing Prime and High Yield vaults, we introduce two new strategy types built using Steakhouse Box adapters: Term strategies, which hold direct positions to the underlying (e.g. Pendle PT), and Turbo strategies, which apply leverage or carry structures to increase exposure. More on Vault Infrastructure coming soon.

Strategies are separated into Prime, High Yield, Term, and Turbo so conservative and higher-risk collateral are not mixed in the same pools, allowing users to choose exposure based on their risk tolerance.

Meaty opportunities are currently available on the app like 13.5% APY on AUSD Turbo vault, or 9% APY on the AUSD High Yield Term vault (both CC ratings) on Mainnet.

Stablecoins: the plumbing of the crypto financial cycle

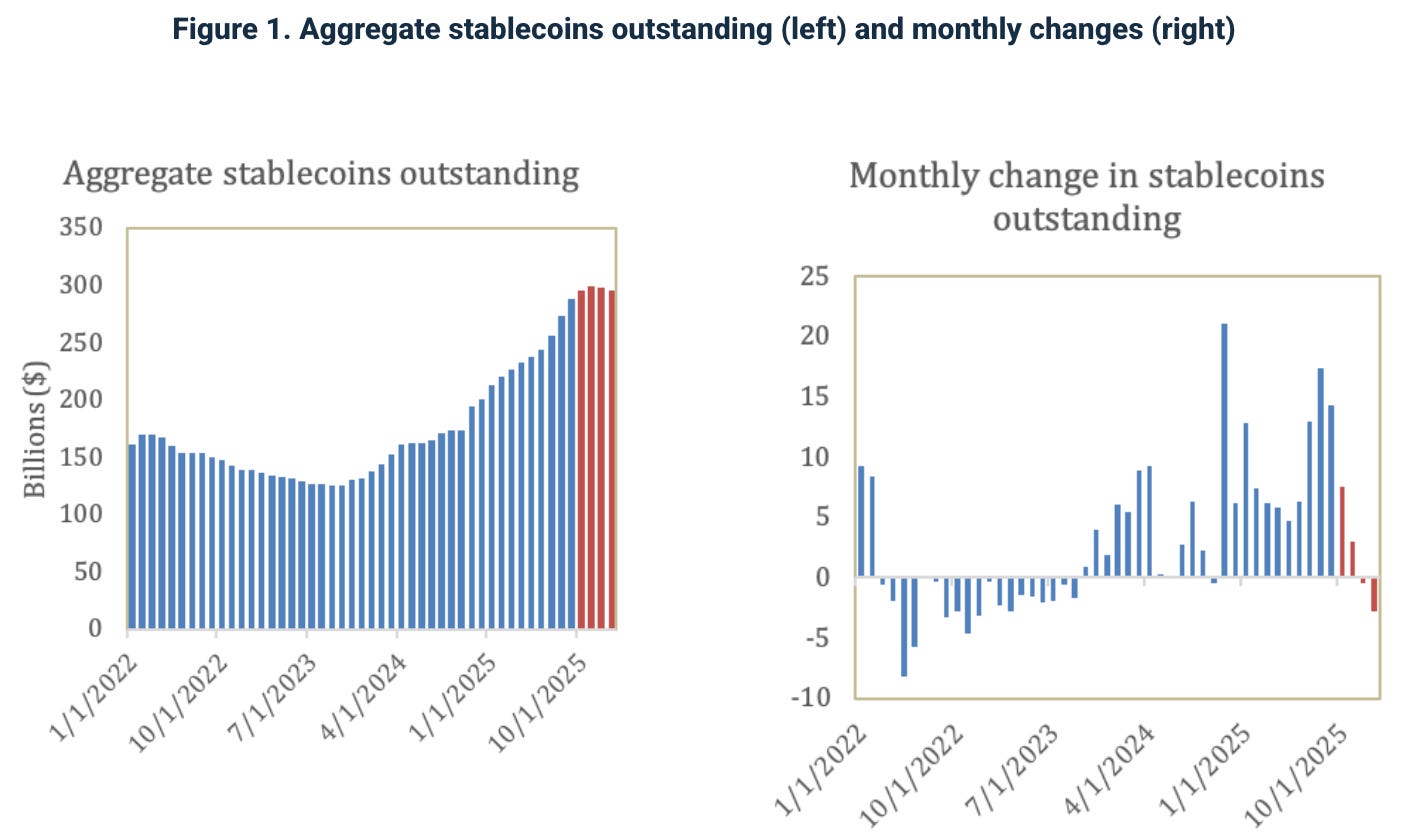

We examine a recent report from the Andersen Institute for Finance & Economics on stablecoin behaviour during the latest crypto winter. After the 10/10 mass market liquidation event and the Stream Finance blow-up, we entered a so-called cold crypto winter with heavy liquidations and declining activity. DeFi lending contracted, with total value locked falling from $90B in October to $52B.

Stablecoins were expected to act as a safe haven during the crash, with users moving out of risky assets into stable dollars. Instead, supply mostly plateaued and slightly declined in recent months, suggesting demand is still closely tied to crypto activity rather than acting as a refuge from it.

The growth of stablecoins outstanding stalled after October, breaking the strong expansion seen through 2024 and early 2025. Authors of the article note that stablecoin supply “contracted” by $125M with two consecutive monthly declines in December and January, something not seen since 2023.

At Steakhouse we would frame this dynamic as plateauing rather than contraction, as the reported decline represents only about 0.05%, alongside a reallocation of some USDC supply into PYUSD and RLUSD driven by incentives. We already discussed this phenomenon in one of our Markets Update.

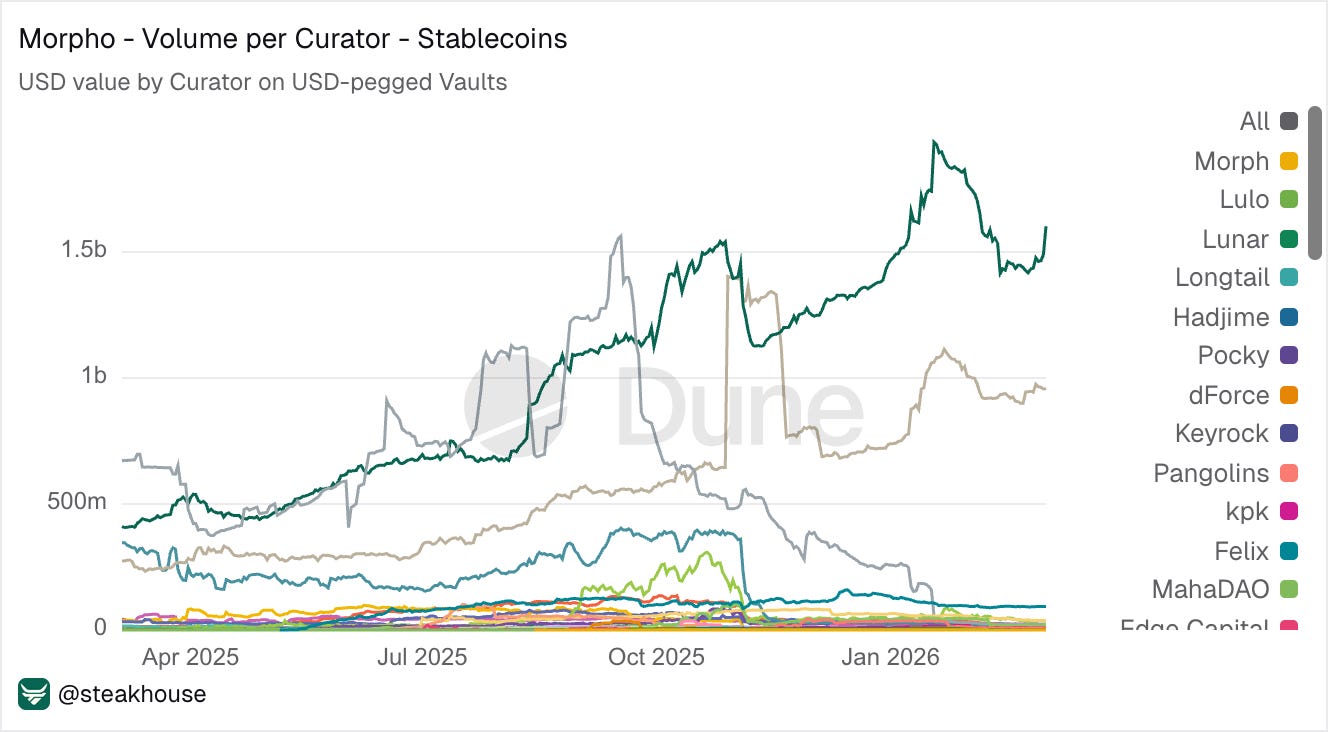

Steakhouse stablecoin vaults on Morpho continued to grow during this period. Capital staying on chain kept flowing into more conservative lending strategies as users sought stable yield and trusted risk management during market stress.

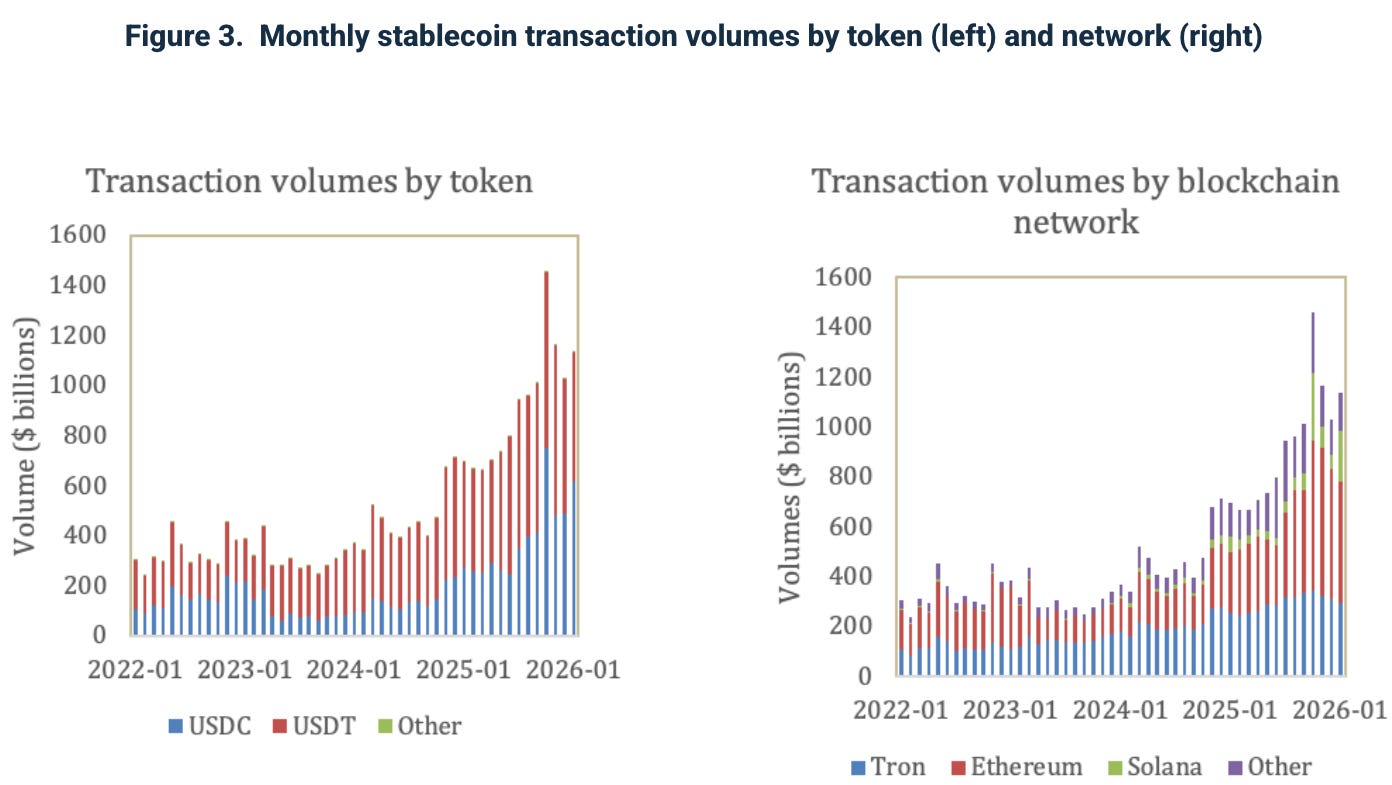

Moreover, transaction activity increased in tandemn with on-chain stablecoin volumes surged in October, reaching around $1.46T according to Visa analytics. The increase was driven mainly by USDC transfers, as traders moved collateral, closed positions, and settled trades during the market stress.

The “crypto winter” confirmed that stablecoins are the plumbing of the crypto financial system, with their product-market fit reflected through transaction activity and volumes growing regardless of market regime.

Katana Liquidity Surge Drives Negative Borrow Rates

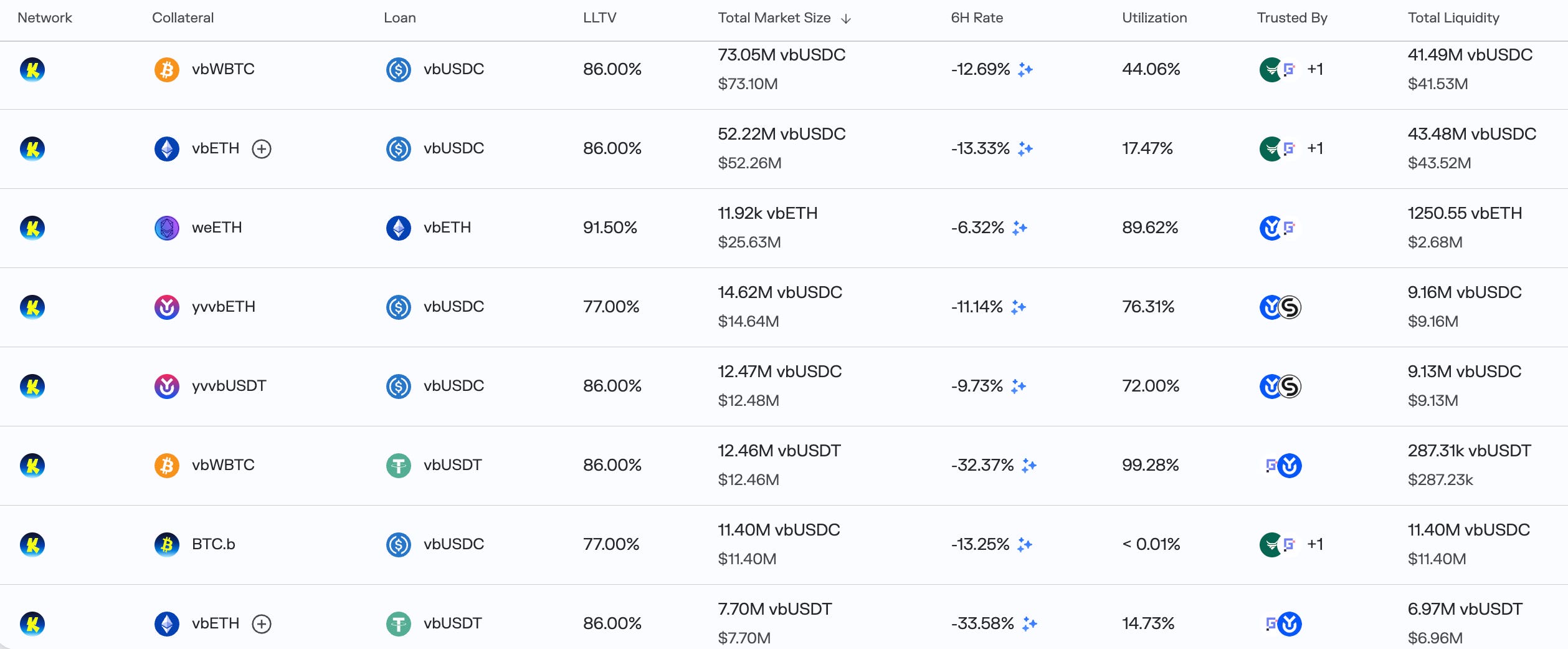

Katana saw a major inflow of stablecoins into Morpho, with roughly $120M+ in TVL added in a single day, much of it flowing into Steakhouse vaults.

As liquidity increased, borrow capacity expanded and rates turned deeply negative across several markets. Borrowing vbUSDC against vbETH or vbWBTC collateral is currently around -13%, effectively paying users to borrow due to excess stablecoin liquidity. There are many more marekts with such incentivized negative rates.

So are these negative borrowing rates paid by lenders?