DeFi Markets Update 2026-04-28

Opportunities on Base, Pooled vs Isolated Lending Markets, Stablecoin Volumes

Welcome to another DeFi Markets Update—your no-nonsense briefing on the cryptobanking plumbing and market pulse.

Base Opportunities: Borrowing, Yields, and Referrals

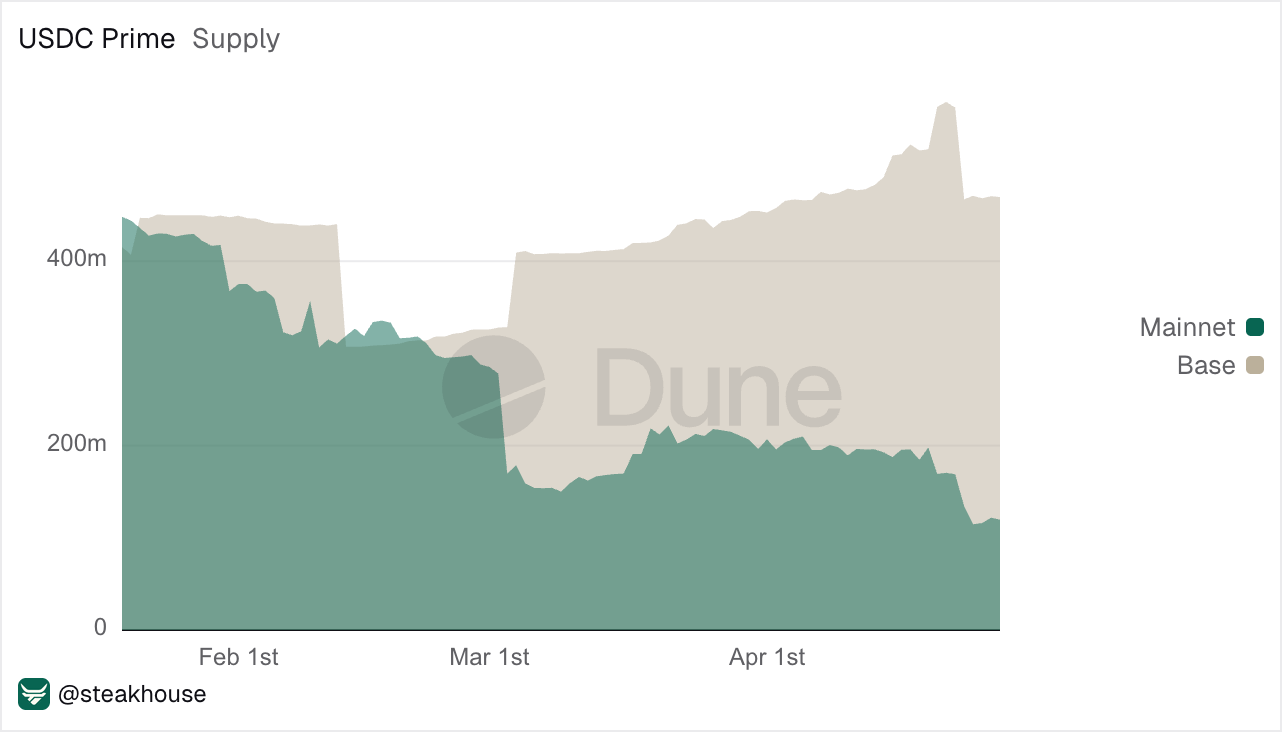

Base is becoming the Morpho hub for USDC lending, as Coinbase Borrow lets users borrow USDC against BTC, ETH or cbETH collateral, with loans executed through Morpho on Base and accessed directly through Coinbase. The supply of Steakhouse USDC on Base has overtaken the one on Mainnet in recent months.

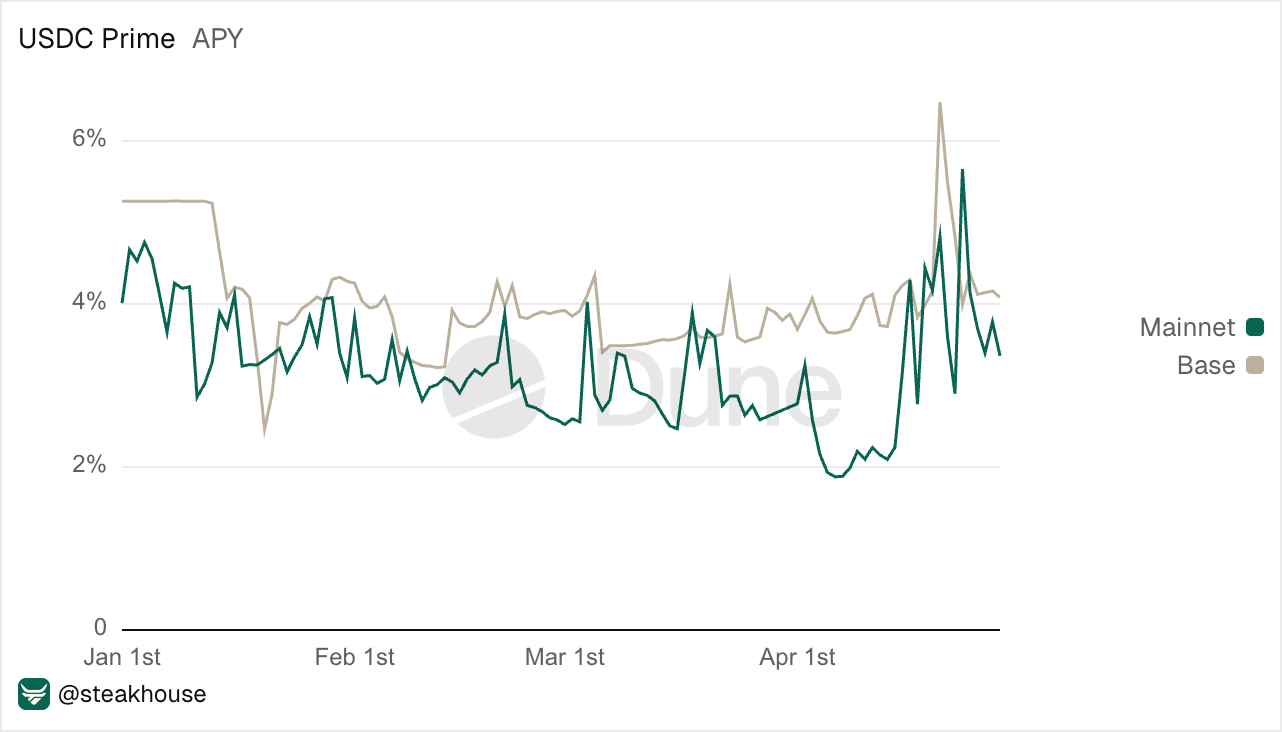

With deeper borrow demand on Base, Steakhouse Prime Instant sits in a more active USDC lending market, which can support steadier utilisation and more resilient allocation. The Base vault offers a conservative profile, with APY consistently around 4% through 2026, compared to a lower circa 3% APY on Mainnet.

Beyond our Prime vault, Steakhouse App also gives users access to other vault strategies on Base including, our USDC HY Instant yielding 6%+ APY.

Lastly, Coinbase is also introducing more user incentives through referral rewards on Base App. Users can earn 25% of net referral swap fees when they refer friends, while referred users receive 10% off swap fees.

Pooled vs Isolated Lending Markets After KelpDAO

Following the KelpDAO exploit, the DeFi ecosystem coordinated one of its largest recovery efforts to date under DeFi United, with reported contributions now exceeding $300m to help restore rsETH backing and stabilise affected markets. However, one question remains: if even Aave, the blue chip of DeFi lending, can face $200m+ of potential bad debt from a poisoned collateral event, what protocols can actually be considered low risk?

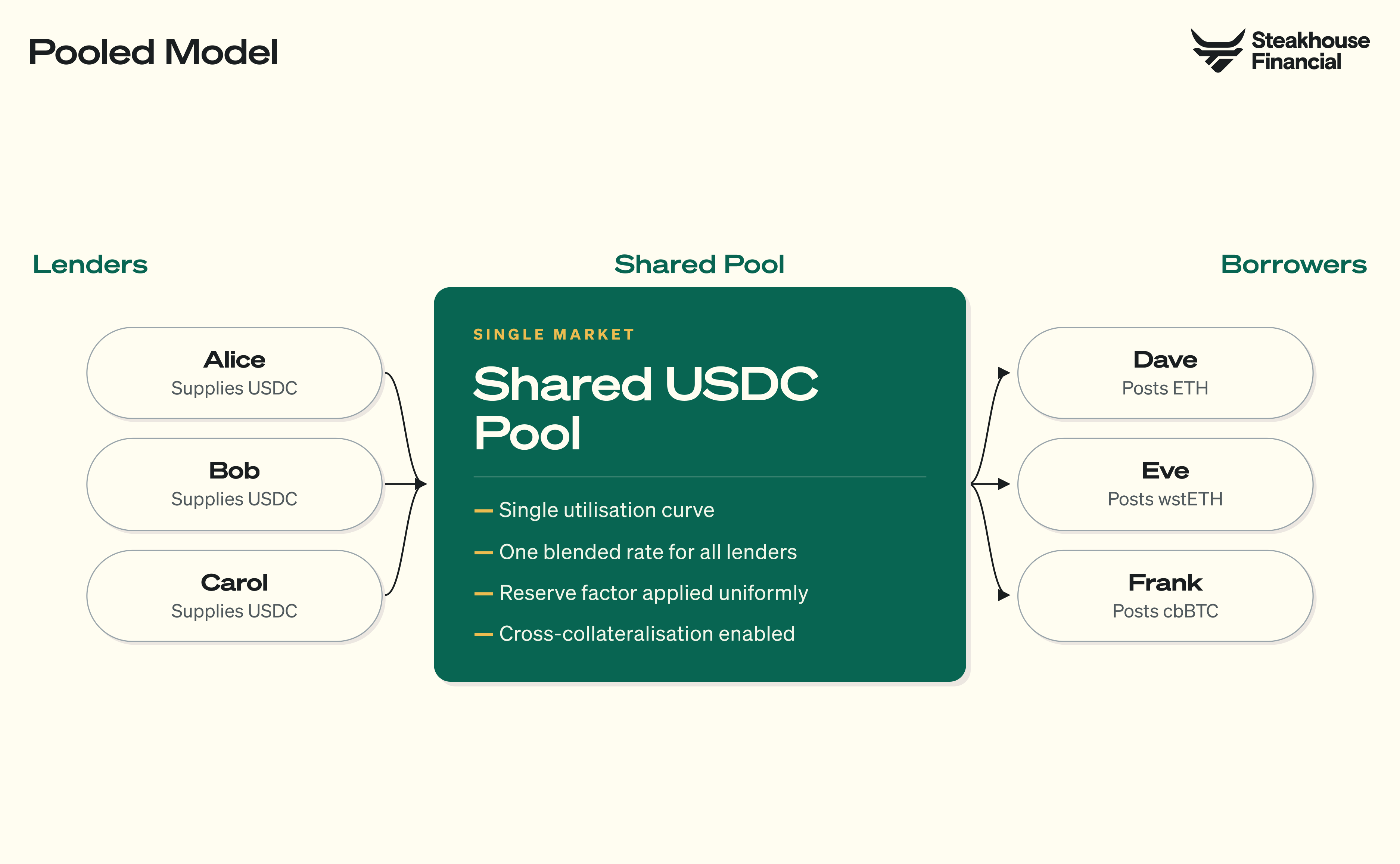

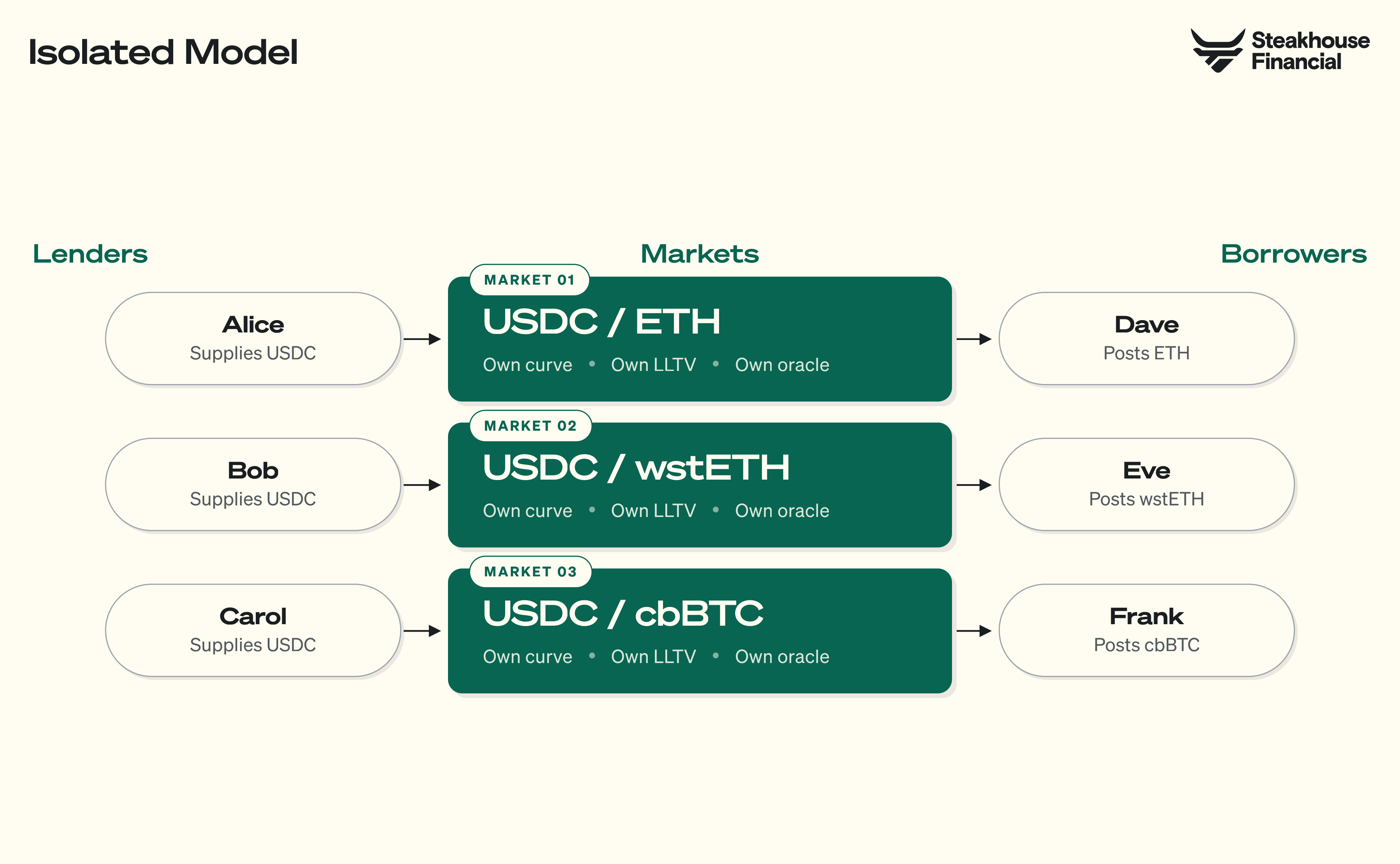

Aave’s pooled design routes deposits into shared liquidity pools, where lenders are exposed to a common set of assets. In the KelpDAO / LayerZero incident, compromised rsETH entered the system as collateral, meaning the risk was able to sit against the broader pool once the asset was used due to rehypothecation. [read more about the Exploit in our previous Markets Update]

This is why lending market design matters when thinking about platform-level contagion risk. Some designs prioritise deep shared liquidity, while others prioritise isolating risk so one asset or market has less ability to affect the rest of the system.

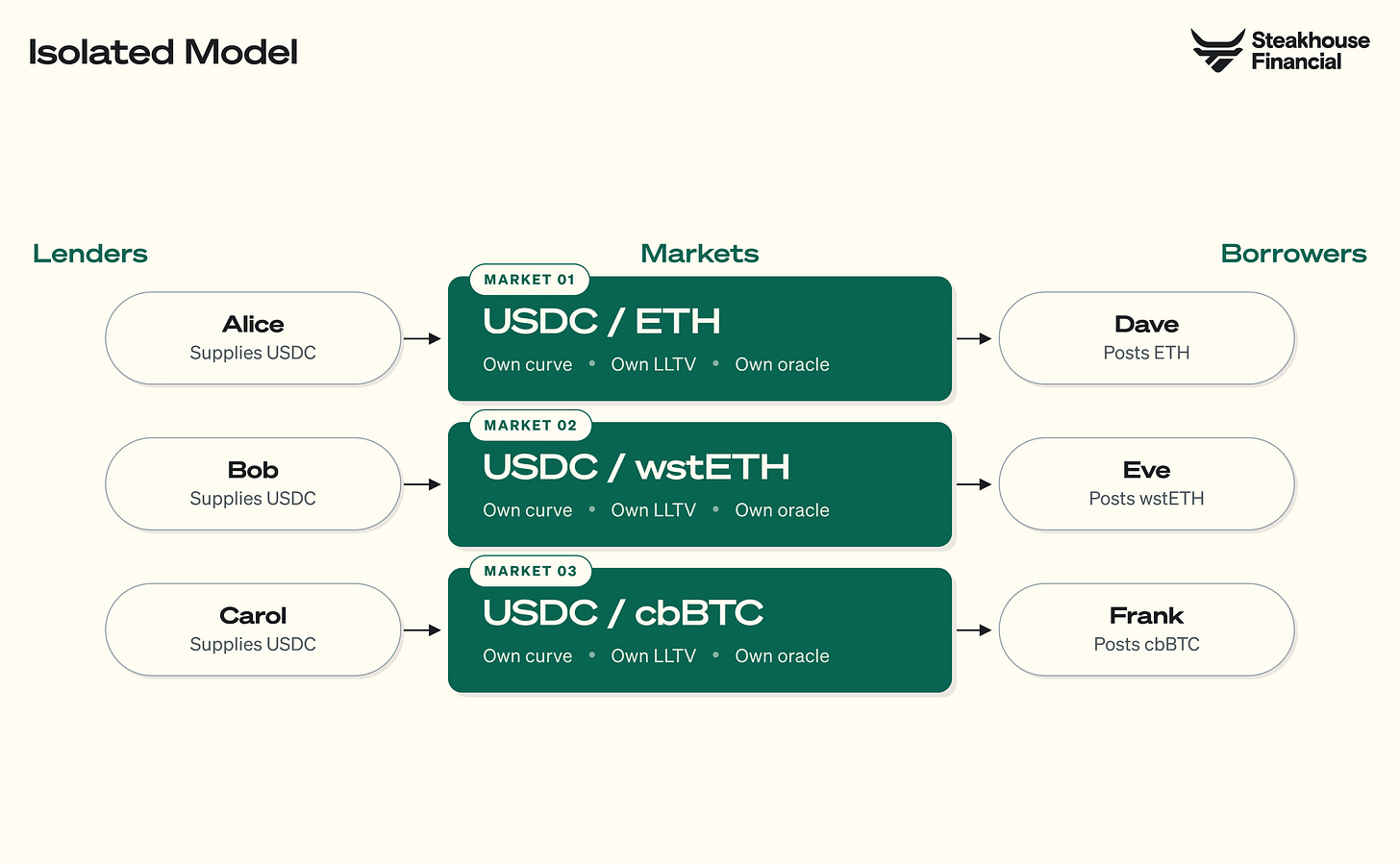

Morpho uses an isolated market design, where capital is allocated across separate vaults and markets instead of one shared pool. This gives each market its own collateral exposure and risk profile. Moreover, collateral can’t be rehypothecated, limiting contagion for borrowers.

In this structure, risk is contained at the market level. For example, if an asset like rsETH is compromised, only the vaults or markets exposed to that asset are affected, while unrelated markets continue to operate independently with no contamination. Borrowers are unaffected.

It is also important to note that “low risk” on Morpho depends on the curator. Curators define the collateral set, manage allocations, and shape the overall risk profile of each vault, so choosing the curator also matters. Even within a given curator, there can be multiple vaults with different risk profiles and levels of risk appetite.

Is Everyone Inflating Stablecoin Volumes?

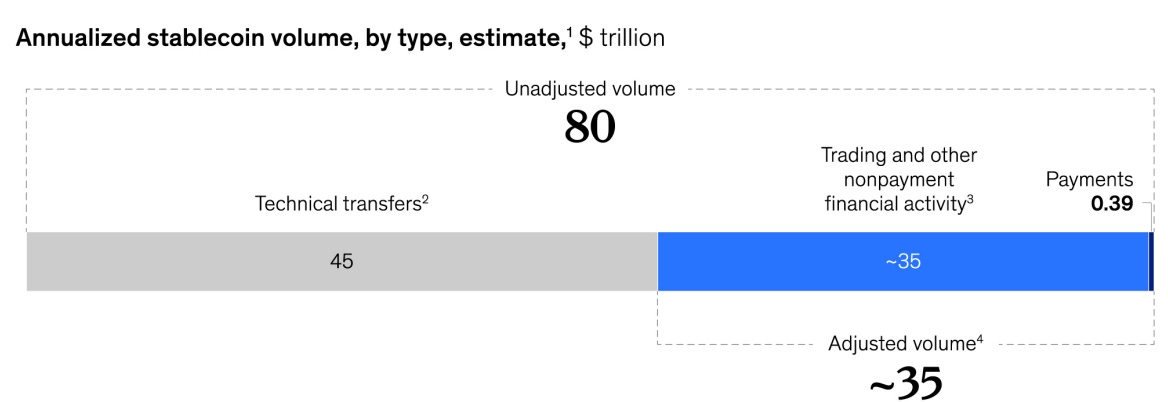

Stablecoin volumes have become one of the easiest numbers to overstate and one of the hardest numbers to interpret properly. A headline can say $35tn in annual volume, like in the another can say that payments are only $390bn, and both can be true depending on whether we are talking about supply, transfer volume, adjusted activity or actual payment usage.

For example, the headline figure of $35tn annual stablecoin transaction volume, reflects the total value transferred onchain. It includes trading flows, exchange and custodian wallet movements, arbitrage, liquidity management, internal treasury transfers, and automated smart-contract activity, where the same capital can move multiple times. Therefore the figure can be often misleading as most of this activity does not represent true end-user payments

To understand the problem, we need to distinguish the key vocabulary often used around DeFi.

Circulating supply refers to how many stablecoins exist, currently over $320bn.

Transfer volume is the total value moved onchain, including trading, internal wallet movements and smart-contract activity.

Adjusted activity attempts to remove obvious noise like bots, wash-like activity and internal transfers to get closer to meaningful usage.

Payment volume captures stablecoins used to transfer value for an economic purpose, including business payments, remittances, payroll, card spend and settlement.

Real payments refers to the portion of payment volume that can be clearly identified and attributed through transaction tagging, address labels, payment infrastructure, or category-level assumptions.

So the ~$35tn figure is essentially everything combined, and it does not represent real payment usage, which is what we often want to look at. To get a clearer picture of actual usage, we need to strip it down. A recent analysis by McKinsey & Company does exactly this.

McKinsey starts with raw onchain data and filters out exchange and custody movements, trading, arbitrage, and automated smart-contract activity. For categories like B2B and remittances, they apply tagging and assumptions to estimate likely payment flows. The result is $390bn annualised stablecoin payment volume based on December 2025 activity, representing a conservative estimate of identifiable real-world payments.

Therefore, the headline volume is reduced by more than 99% to estimate identifiable payment usage. This is an extremely large reduction; so does this mean stablecoins, and hence, DeFi are both underperforming? Not really. Even under McKinsey’s strict definition, identifiable stablecoin payment volume has more than doubled since 2024, per their report. At the same time, stablecoin supply has grown from roughly $130bn in 2024 to over $320bn today, showing continued inflows and adoption across the ecosystem.

The takeaway is that stablecoins operate across multiple use cases: trading, collateral, liquidity management, settlement, payments and more. A single number rarely captures the full picture, and headlines can be attention-grabbing. Often, the wording blends very different concepts into one number, shaping how the data is interpreted, so don’t get fooled and stay sharp.