DeFi Markets Update 2026-03-11

EURCV Adoption, Stablecoin inflows pressure Treasury yields, AUSD Farming

Welcome to another DeFi Markets Update—your no-nonsense briefing on the cryptobanking plumbing and market pulse.

EURCV Adoption Accelerates with Deblock and Safe Integrations

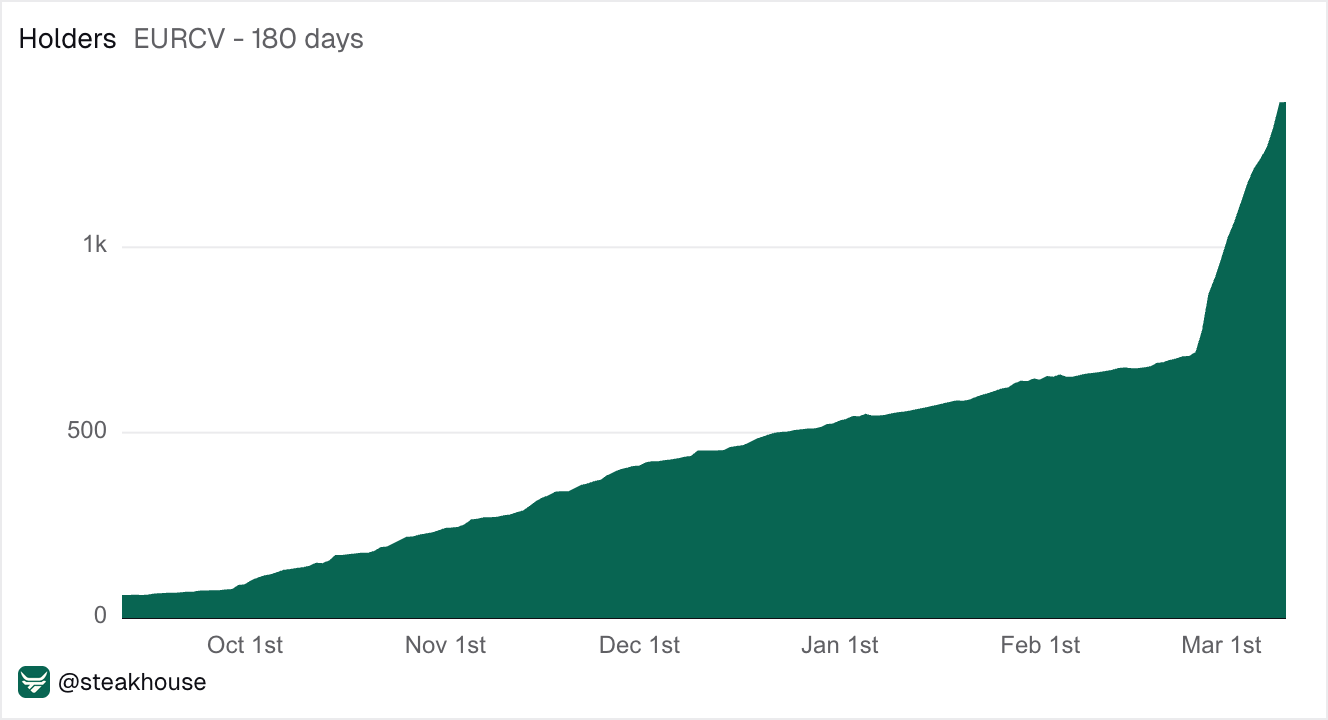

The tokenised euro ecosystem recently crossed $1B in circulating supply, according to Token Terminal data tracking EUR-denominated stablecoins, marking a notable step for euro-based stablecoins and suggesting that regulated EUR liquidity is beginning to gain traction on-chain.

Recent integrations by Deblock and Safe are expanding EURCV distribution across both fintech and wallet interfaces. Deblock lets users hold EURCV in-app and deploy it into yield strategies without using DeFi protocols directly, while Safe gives users access to a Steakhouse curated EURCV vault from the wallet interface.

Since the Safe and Deblock integrations launched on 25 and 26 February, the number of EURCV holders has roughly doubled within two weeks, suggesting that new distribution channels are beginning to bring regulated euro stablecoins to a broader user base.

Steakhouse curates the majority of EURCV vaults on Morpho, with the EURCV Prime Instant vault that you can explore on the Steakhouse App, currently offering 4.1% APY in an A-rated strategy.

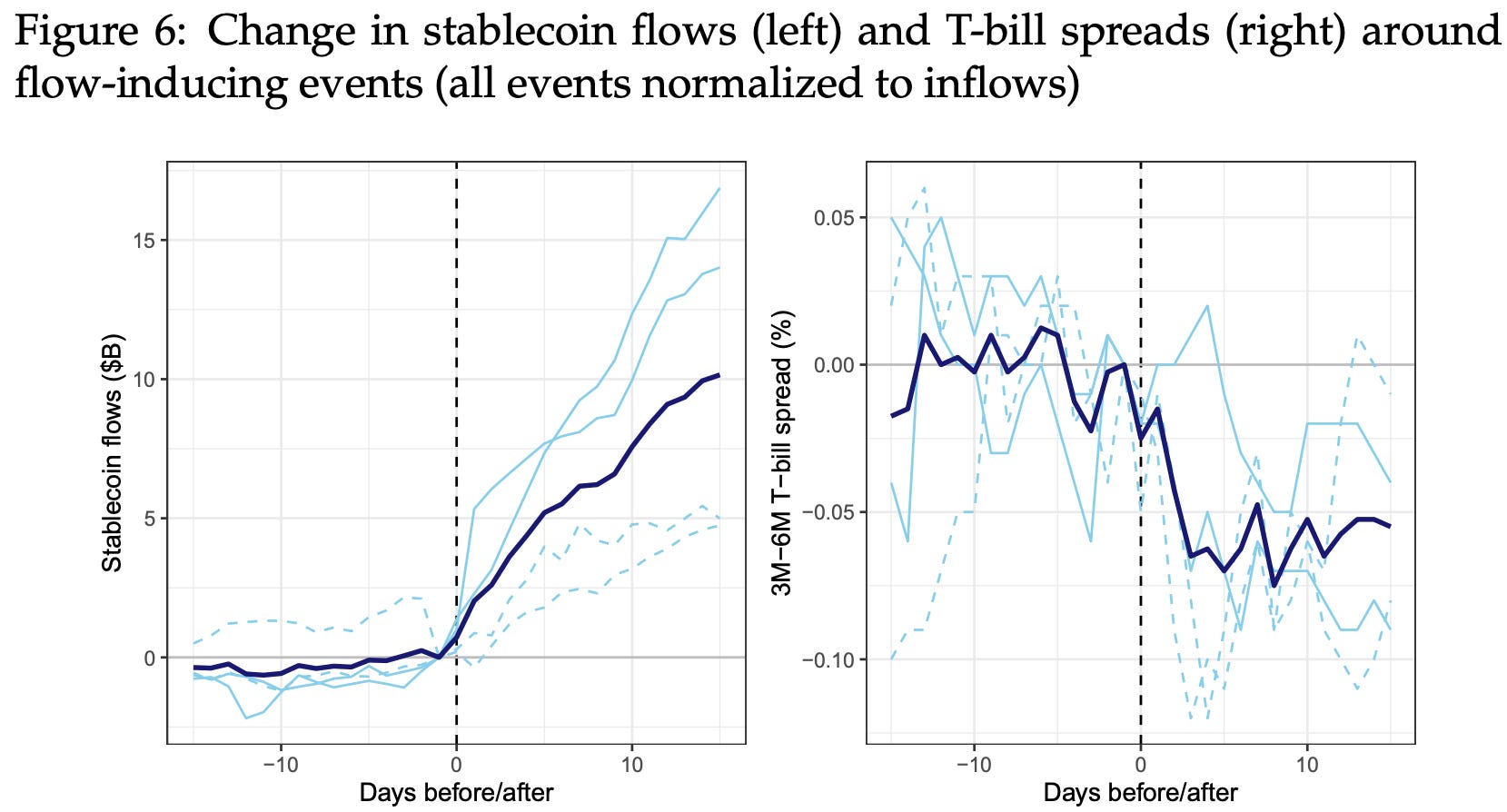

Do stablecoin inflows create measurable demand pressure in the Treasury Market?

In the Bank for International Settlements (BIS) Working Paper No. 1270, “Stablecoins and safe asset prices”, the authors analyse the relationship between dollar-backed stablecoin flows and short-term US Treasury yields using daily data from January 2021 to March 2025, defining flows as the 5-day change in the aggregate market capitalisation of the six largest USD stablecoins.

As previously discussed in a Markets Update, stablecoin reserves are largely invested in short-term government securities and repo markets, meaning new stablecoin issuance creates direct demand for US Treasury bills as issuers invest incoming dollars into safe reserve assets.

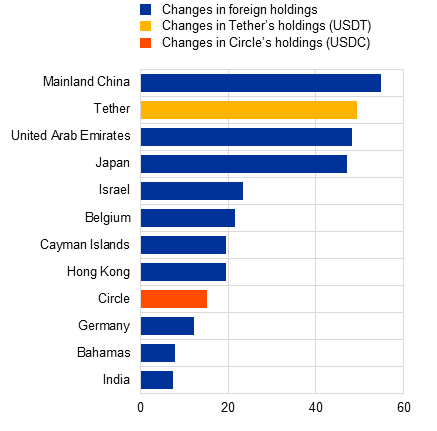

By March 2025, stablecoin issuers collectively managed over $200 billion in assets, exceeding the short-term Treasury holdings of many foreign investors. Between January 2024 and September 2025 alone purchased roughly $64 billion of Treasury bills, placing them alongside major foreign holders of short-term US government debt.

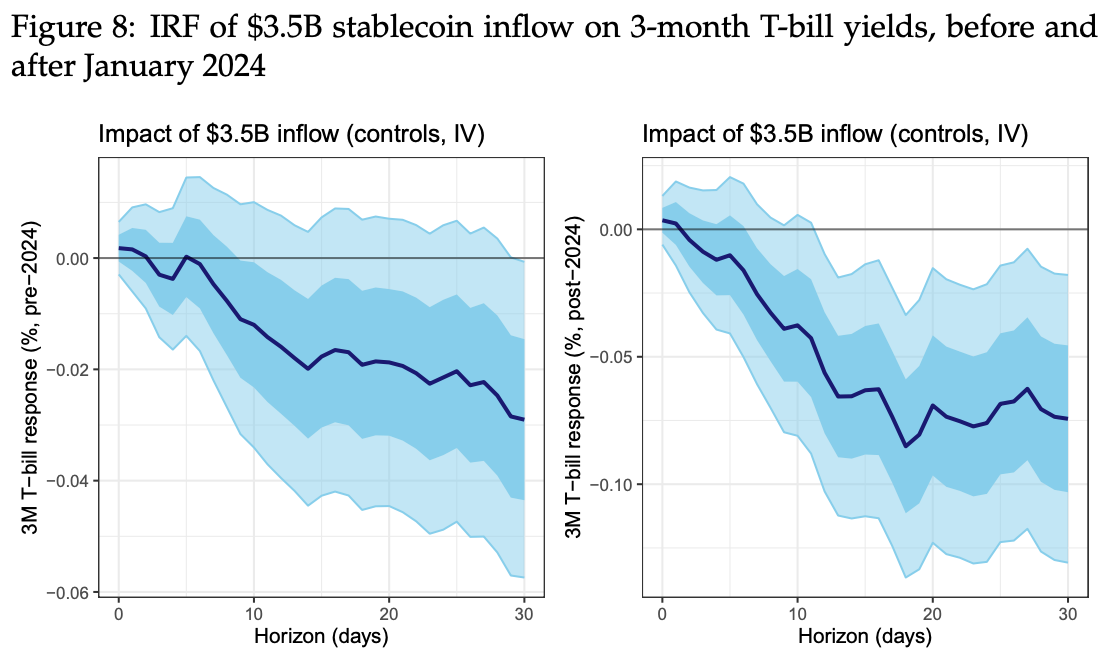

The paper finds that stablecoin inflows have a measurable effect on short-term Treasury yields: a two-standard-deviation inflow shock (roughly equivalent to several billion dollars of new stablecoin issuance) lowers the 3-month Treasury bill yield by about 2.5–3.5 basis points, with the effect appearing within around 10 days.

They used a statistical model to estimate how sudden increases in stablecoin supply affect the 3-month Treasury bill yield. The results suggest that large inflows of new stablecoin issuance are associated with small declines in short-term Treasury yields. However, it’s important to note that stablecoin supply often expands during crypto bull markets, which themselves tend to coincide with periods of stronger global liquidity. In that case, stablecoin growth may partly reflect broader liquidity cycles rather than being the main driver of additional Treasury demand.

The price impact is state-dependent: when Treasury bill supply is abundant, the effect becomes statistically insignificant, but during periods of bill scarcity (measured using increases in the Federal Reserve’s Overnight Reverse Repo Facility (ON RRP) or debt-ceiling episodes) the estimated yield impact rises to roughly 5–8 basis points, indicating stronger sensitivity when safe assets are scarce.

Some scepticism remains around the magnitude of the effect as the US Treasury bill market is roughly $6–7 trillion, compared with stablecoin reserves of about $200 billion, meaning stablecoin inflows represent only a small share of the overall market. As a result, we can argue the estimated few-basis-point yield impact may reflect model sensitivity rather than measurable price pressure.

To conclude, the evidence provided by BIS suggests stablecoin inflows exert some demand pressure on short-term Treasury markets, particularly during periods of safe-asset scarcity, although we have to note that part of the relationship may also reflect reverse causality, where higher Treasury yields incentivise further stablecoin issuance.

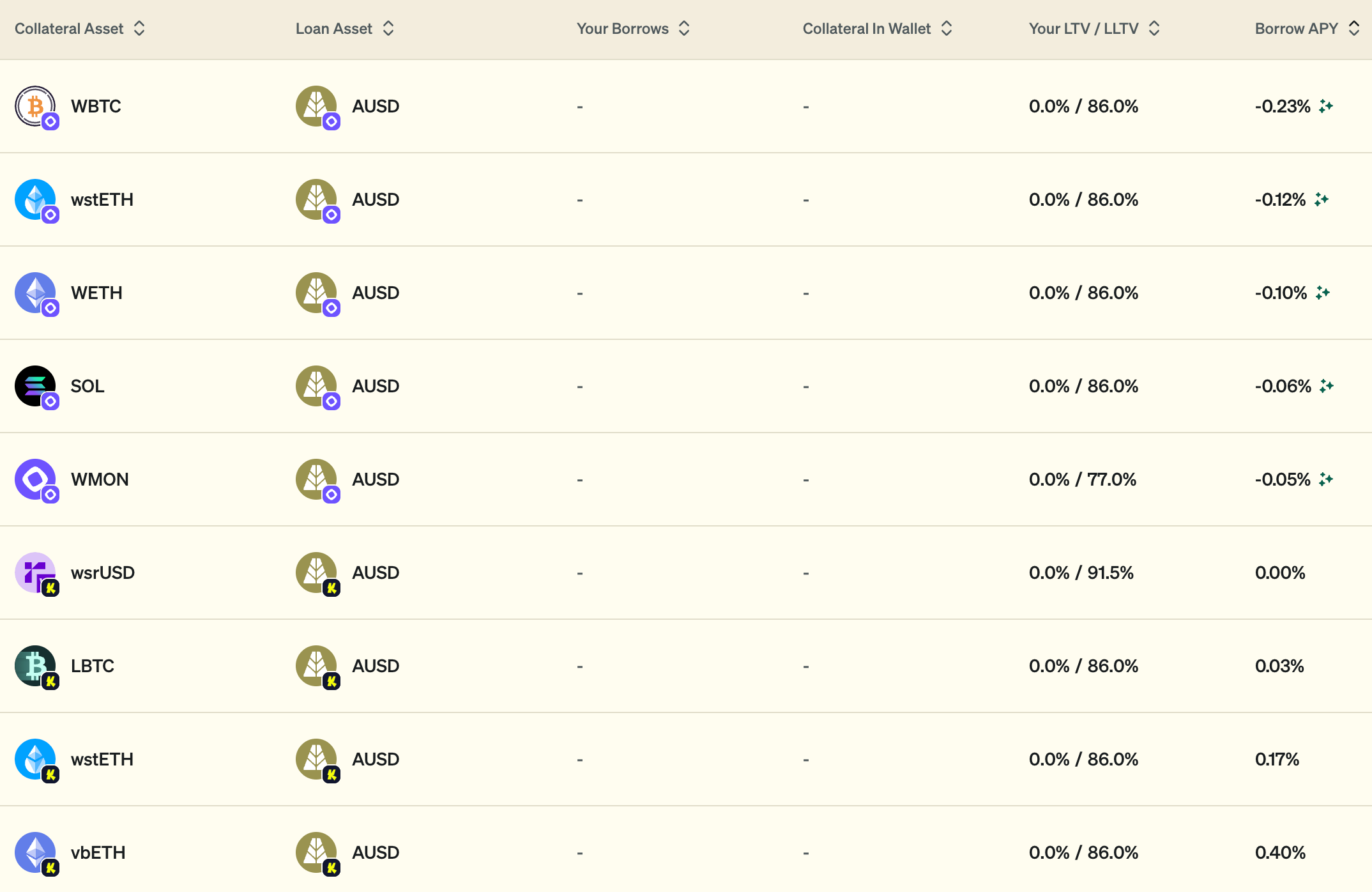

AUSD Farming on the Steakhouse App

The Steakhouse app has now been live for about a week, and it’s already bringing many great opportunities with it.

As highlighted in the last Markets Update, AUSD vaults continue to keep rewards high, with yields currently reaching up to 25% APY on the High Yield Term vault.

On the borrow side, AUSD rates remain near 0%, with particularly cheap borrowing currently available on Monad and Katana.

For example, on Monad, the WBTC/ AUSD market currently offers negative borrow rate, effectively paying users to borrow AUSD.