DeFi Markets Update 2026-02-18

Mainnet Opportunities, EURCV, Stablecoins Overview

Welcome to another DeFi Markets Update—your no-nonsense briefing on the cryptobanking plumbing and market pulse.

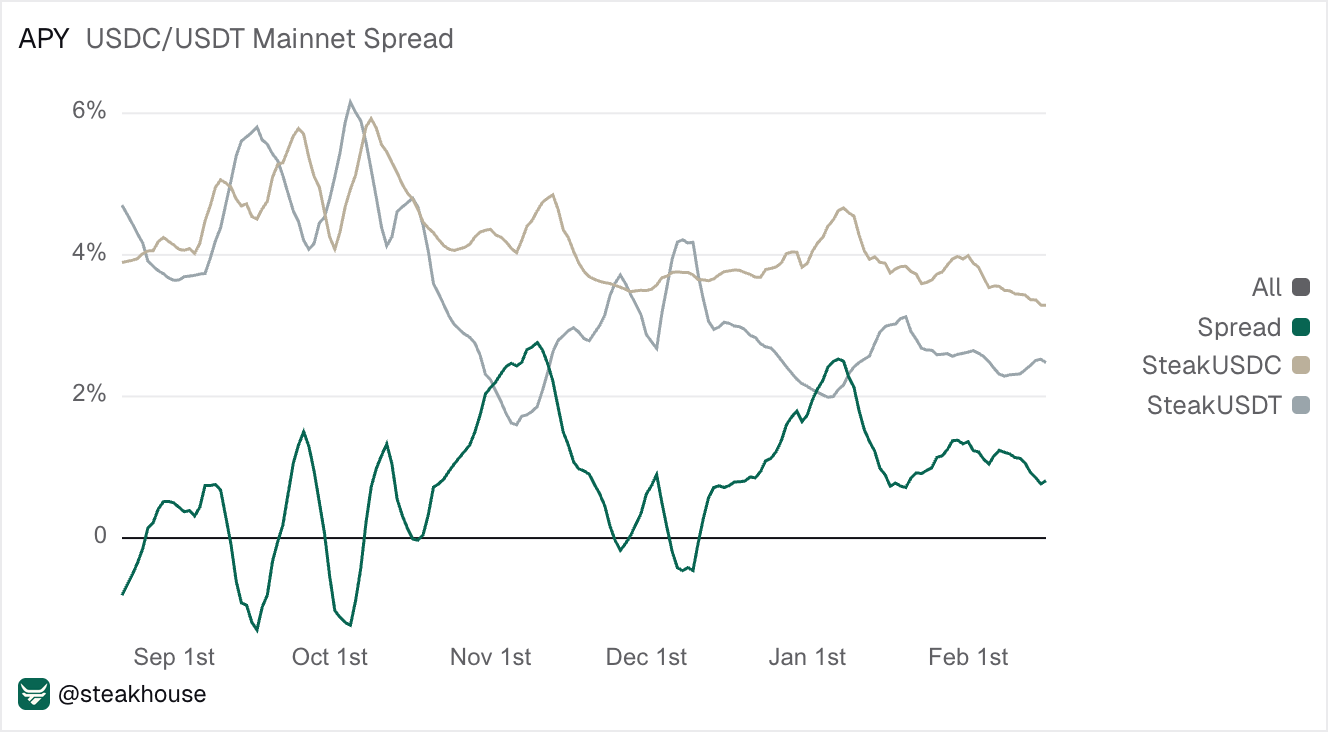

Mainnet Lending Opportunities

Morpho Incentives on V2 vaults have created an attractive opportunity for our Steakhouse High Yield Instant V2 Vault, that is currently yielding 5% APY on Mainnet.

This V2 vault deploys exclusively into the Smokehouse USDC, which currently has $67m TVL and $21m available liquidity, combining the V1’s proven track record with V2’s updated vault framework.

Additionally, there’s still a positive spread to capture between the Steakhouse V2 Prime Instant USDC and USDT vaults on Mainnet.

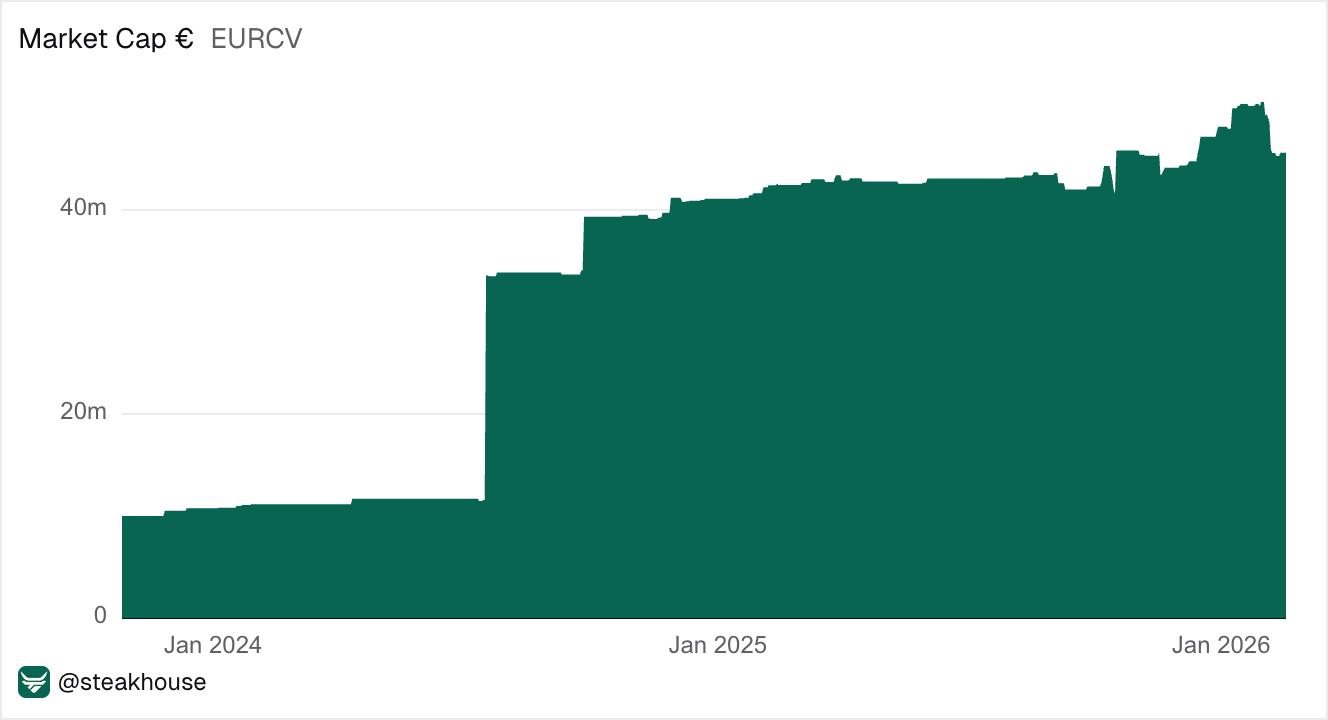

EURCV Market Overview

EURCV has been growing steadily since launch and now sits at around €45m in circulating supply.

EURCV is a euro-denominated token issued directly on Ethereum Mainnet by a global banking group via Société Générale – FORGE.

The token follows a bank-native issuance model, with on-chain representation issued on a public blockchain and structured around segregated reserves and par redemption, in line with established financial frameworks (MiCA).

Despite the relatively low-risk profile, EURCV is currently earning around 6.4% APY when lent on Morpho as a new incentive campaign start.

Meanwhile, borrowing costs in EURCV lending markets are around 1% when borrowing against cbBTC and wstETH.

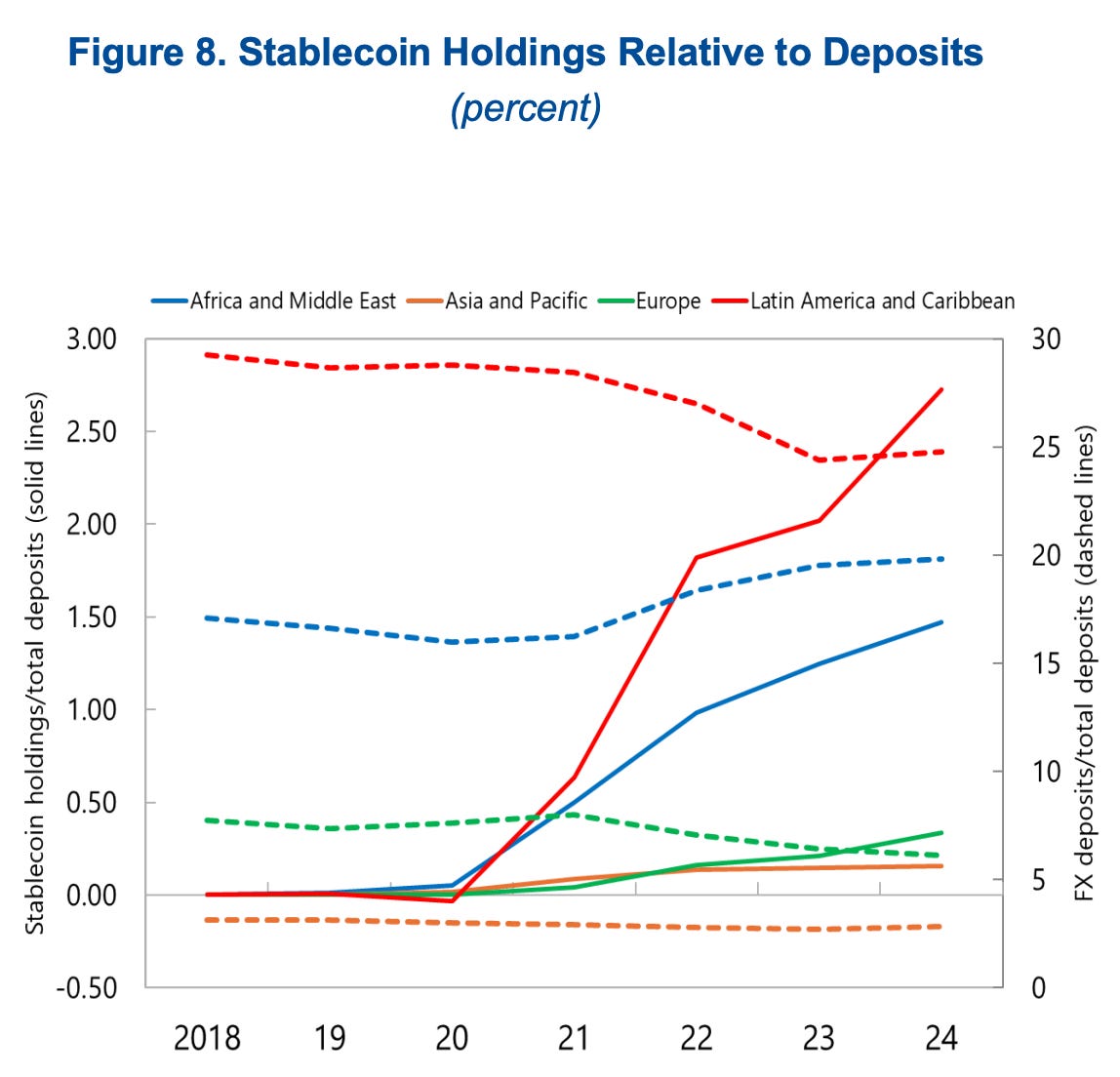

Stablecoin Growth, Concentration, and US Treasury Exposure

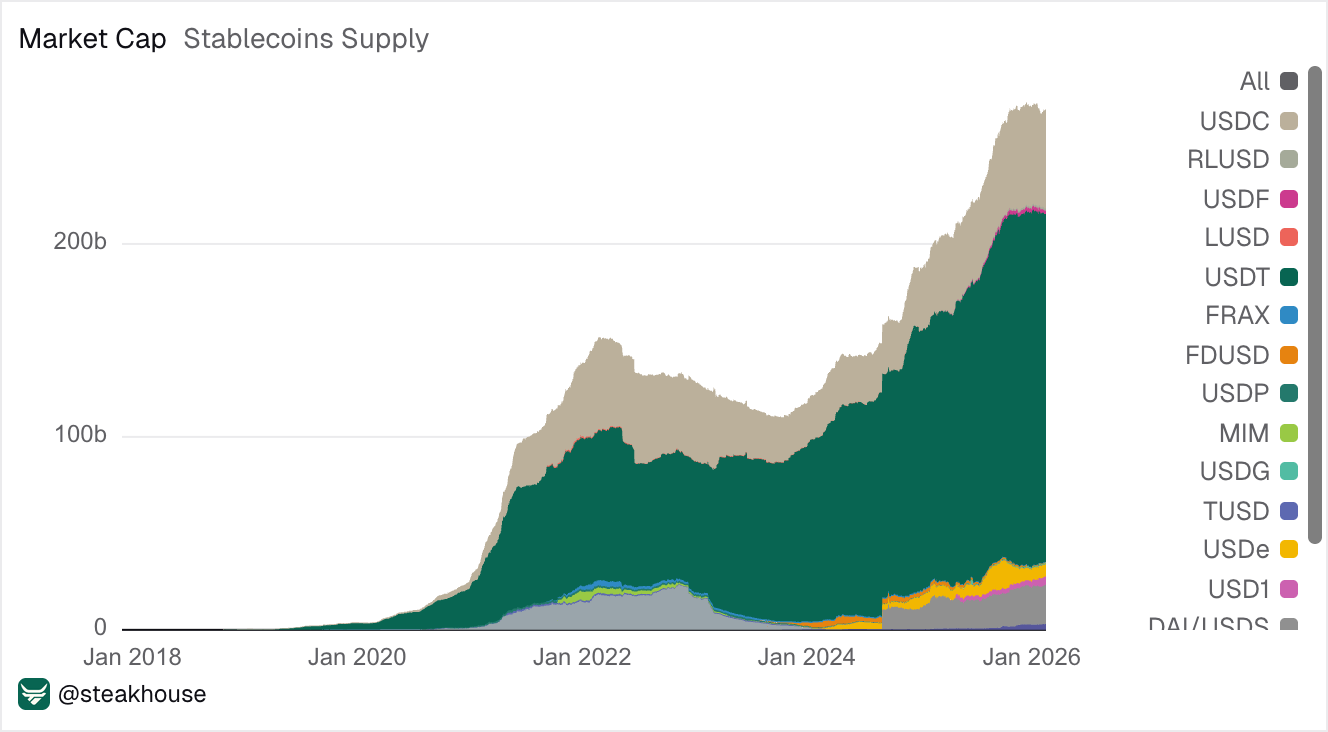

Based on recent (Dec 2025) analysis titled “Understanding Stablecoin”, the IMF discuss the evolving role of stablecoins in global financial markets as stablecoin market capitalisation increased from $150bn in 2024 to around $300bn by the end of 2025, equating to around 7% of total crypto market cap.

The market is highly concentrated, as USDT and USDC represent about 90% of total stablecoin value, meaning changes in their reserve management affect overall stablecoin risk and behaviour.

USDT and USDC reserve composition has matured over the past five years and is now mostly backed by US Treasury bonds and reverse repo.

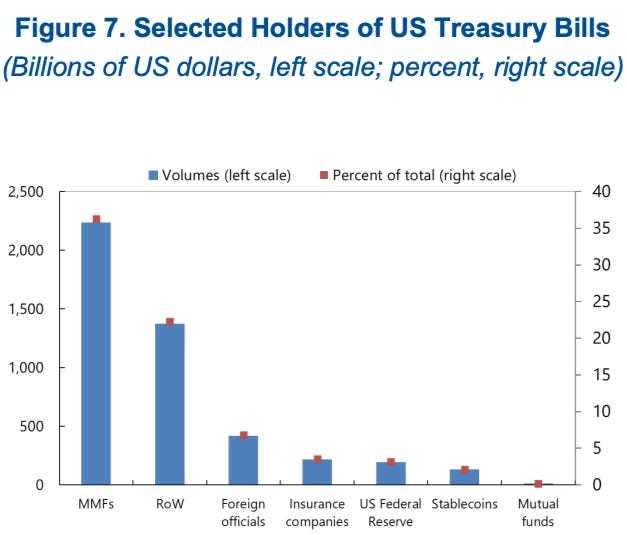

Stablecoin issuers have accumulated a large amount of US Treasury Bills, reaching a scale comparable to the US Federal Reserve, which holds around $4.3 trillion in Treasury securities.

Stablecoins are increasingly used in countries with weaker local currencies. For example, in Latin America, stablecoin holdings relative to bank deposits increased from near zero to roughly 2.5–3% within 4 years.

Is figure 8 EM and that's why North America is not there?