DeFi Markets Update 2026-04-22

KelpDAO Exploit, Prime vaults continue to Grow, Stablecoin Spillovers to FX Markets

Welcome to another DeFi Markets Update—your no-nonsense briefing on the cryptobanking plumbing and market pulse.

KelpDAO Exploit

On April 18, 2026, attackers drained about 116,500 rsETH (~$292M) from KelpDAO’s LayerZero-powered cross-chain bridge by poisoning the RPC nodes LayerZero’s verifier relied on and DDoS’ing into the backups, tricking the bridge into releasing tokens against a forged cross-chain message.

The attackers, preliminarily linked to the Lazarus Group, deposited 89,567 rsETH on Aave and borrowed 82,650 WETH and 821 wstETH against it. As this collateral is now impaired, those positions could translated into protocol shortfall, with the final bad-debt outcome depending on how Kelp allocates the bridge loss across rsETH holders.

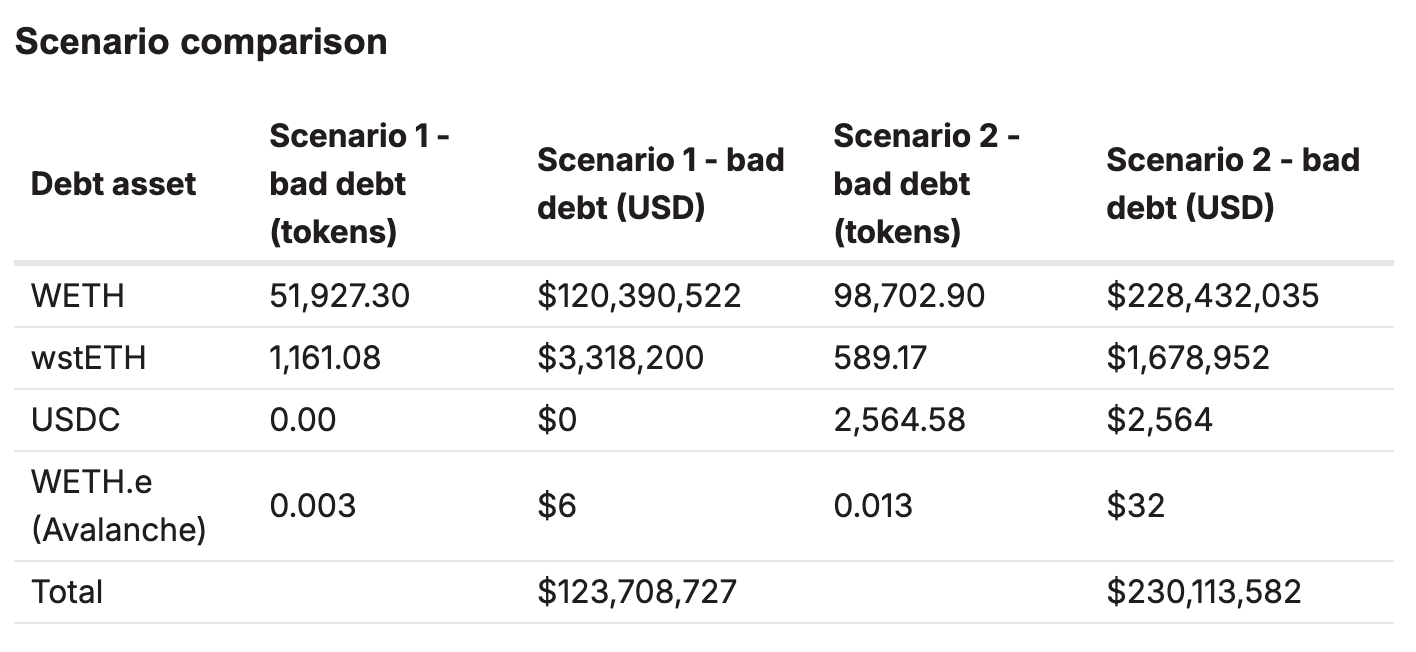

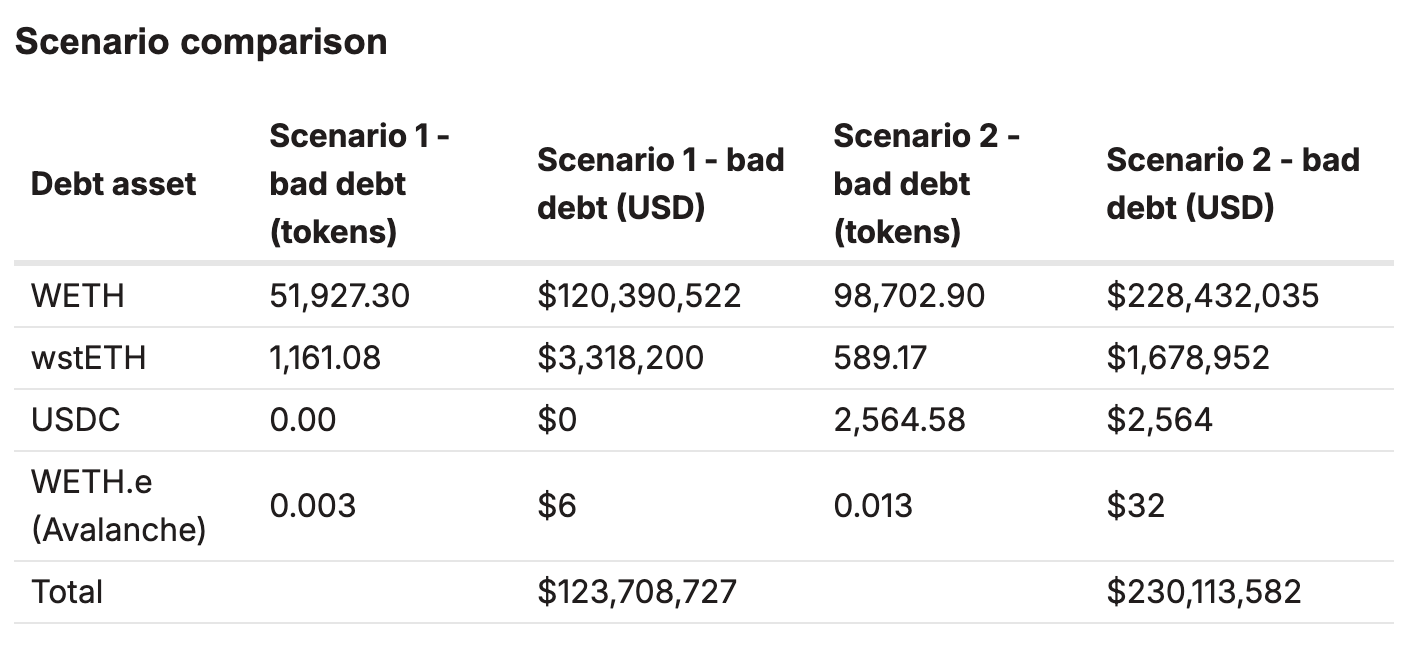

In Aave’s incident report, the protocol models two bounding cases: one where the 112,204 unbacked rsETH is socialised across the full supply, implying $123.7M of bad debt, and another where the impairment is isolated to bridged rsETH only, which produces materially larger losses on L2 markets. Under the first case, Aave also notes that Ethereum Core’s Umbrella WETH module could absorb part of the hit.

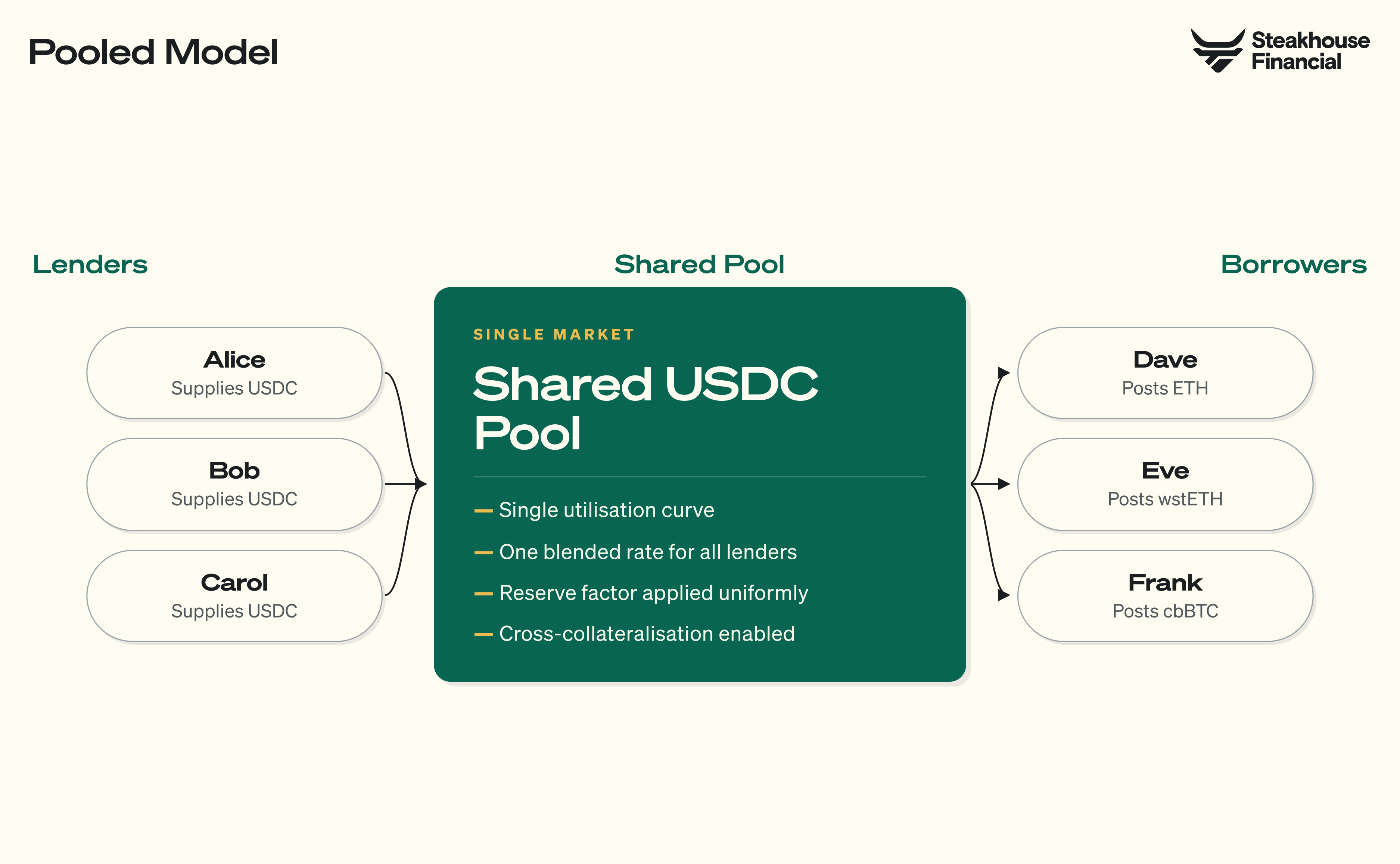

Aave’s exposure stemmed from its pooled architecture as lenders supply into a single shared liquidity pool, against which any whitelisted collateral, ETH, wstETH, cbBTC, or in this case rsETH, can borrow against that same pool under one blended rate and shared risk parameters.

Moreover, the contagion spread because Kelp’s inflated supply left rsETH partially unbacked across more than 20 supported chains, including Base, Arbitrum, Linea, Blast, and Mantle. Around 18% of the circulating supply became effectively unbacked, which triggered depositor withdrawals as users rushed to avoid being affected. That wave of exits pushed DeFi TVL down by $13bn in 48 hours, making it the largest DeFi exploit of 2026. As one of the leading money markets, Aave sits at the centre of that exposure, leaving many protocols affected even as Aave itself remains largely illiquid for now.

On Morpho, the isolated-market design meant the damage was capped; only $1M of ETH was borrowed against rsETH as collateral across two isolated markets, and just 2 of ~500 Morpho Vaults (with >$10k in deposits) had any exposure to those markets.

At Steakhouse, we had less than $0.01 of exposure to KelpDAO, which we exited. We communicated all changes made to our vaults via our socials and remained unaffected by the hack. This marks the second major DeFi incident in a row this year in which our curation has shielded users from losses, following the Resolv USR incident. To this day, we still have zero non-dust bad debt since we started curation.

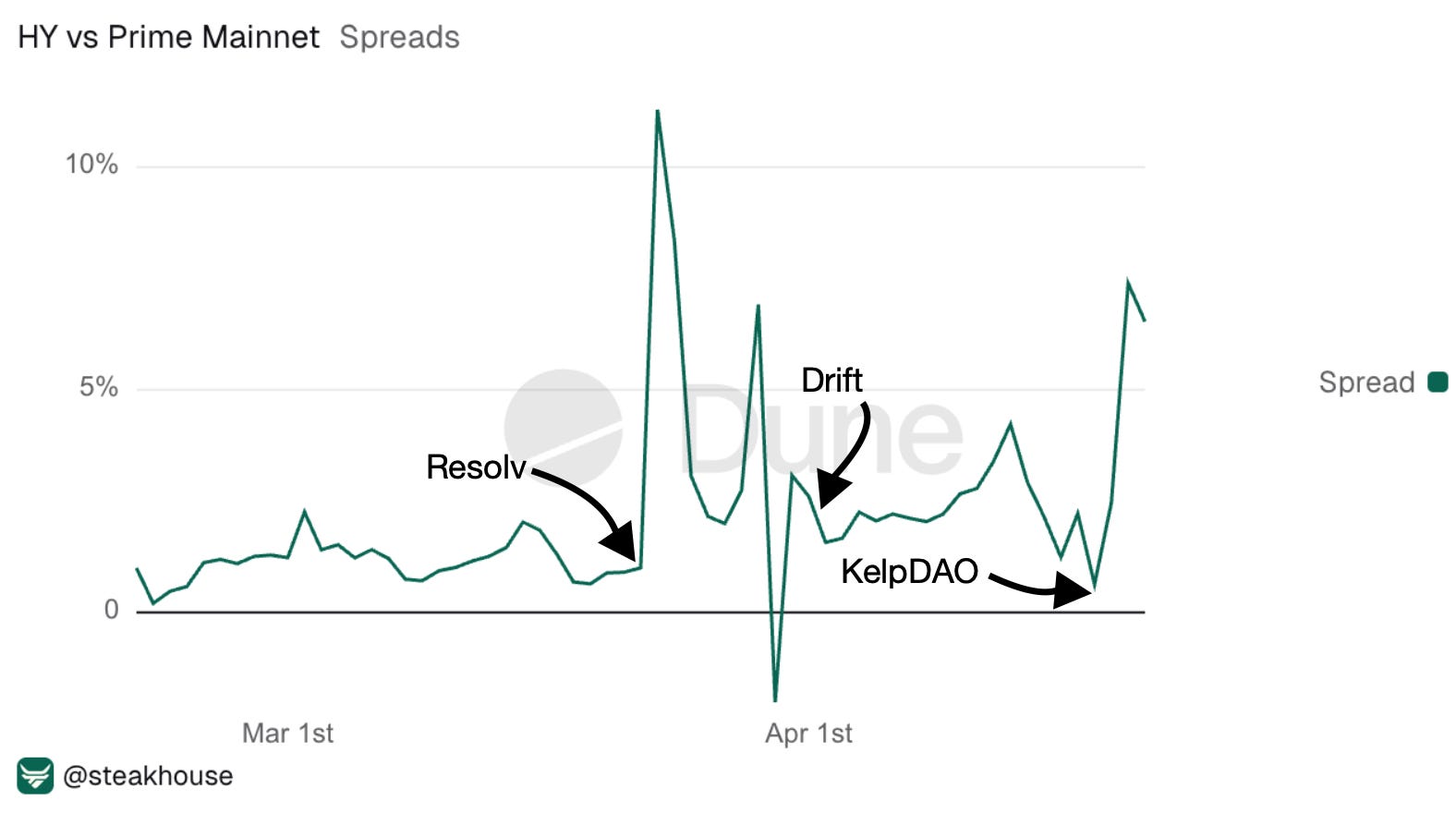

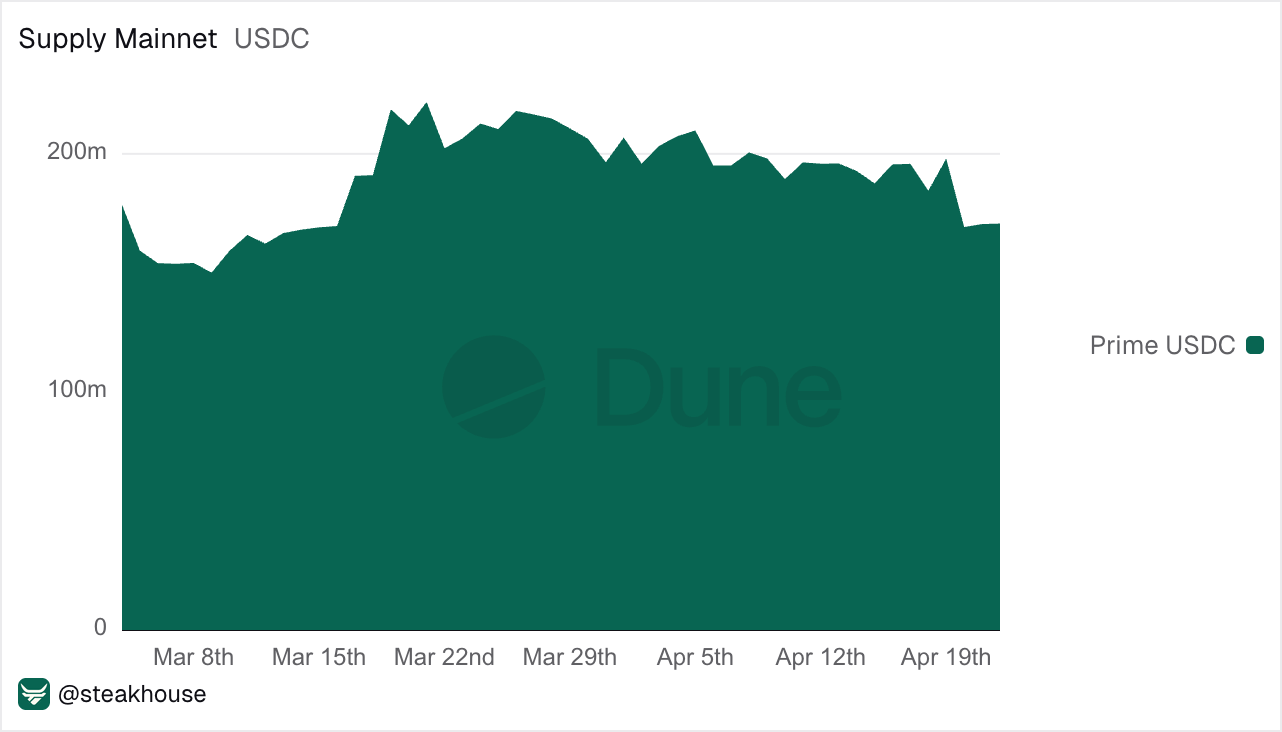

Steakhouse Prime vaults Grow after a month of Exploits

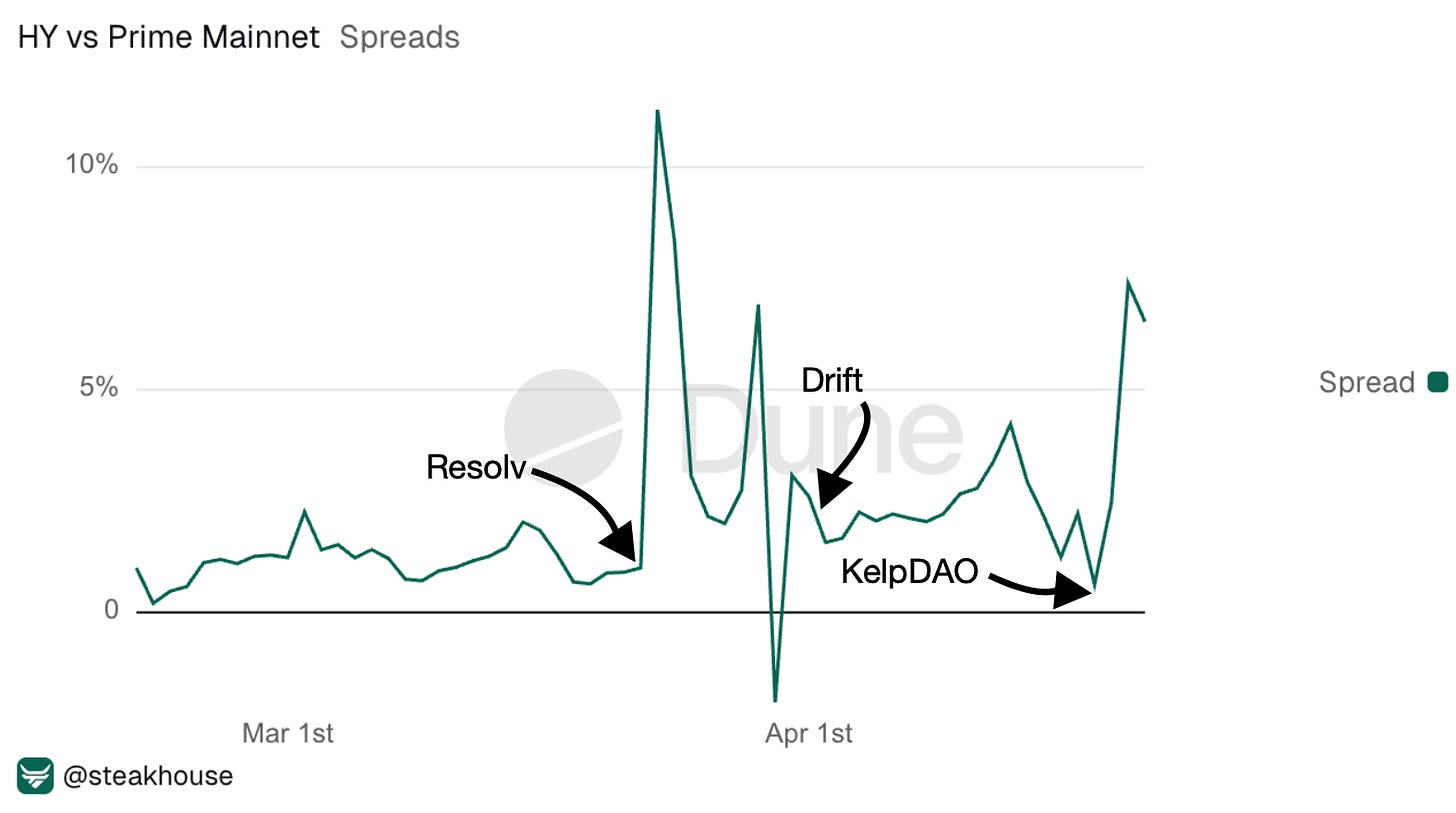

DeFi has gone through a rough month, with multiple exploits and hacks pushing markets to price risk higher. As allocators became more cautious and moved into safer positions, the spread between Prime Instant and High Yield Instant USDC vaults widened over the past month on Mainnet.

Based on daily averages, the spread is now around 7% APY. For users still in V1, this is a strong reason to migrate into our V2 vaults and access that spread through the updated architecture.

Reallocation out of riskier strategies and into Prime vaults increased supply by $60M in a single week at the end of March on Mainnet.

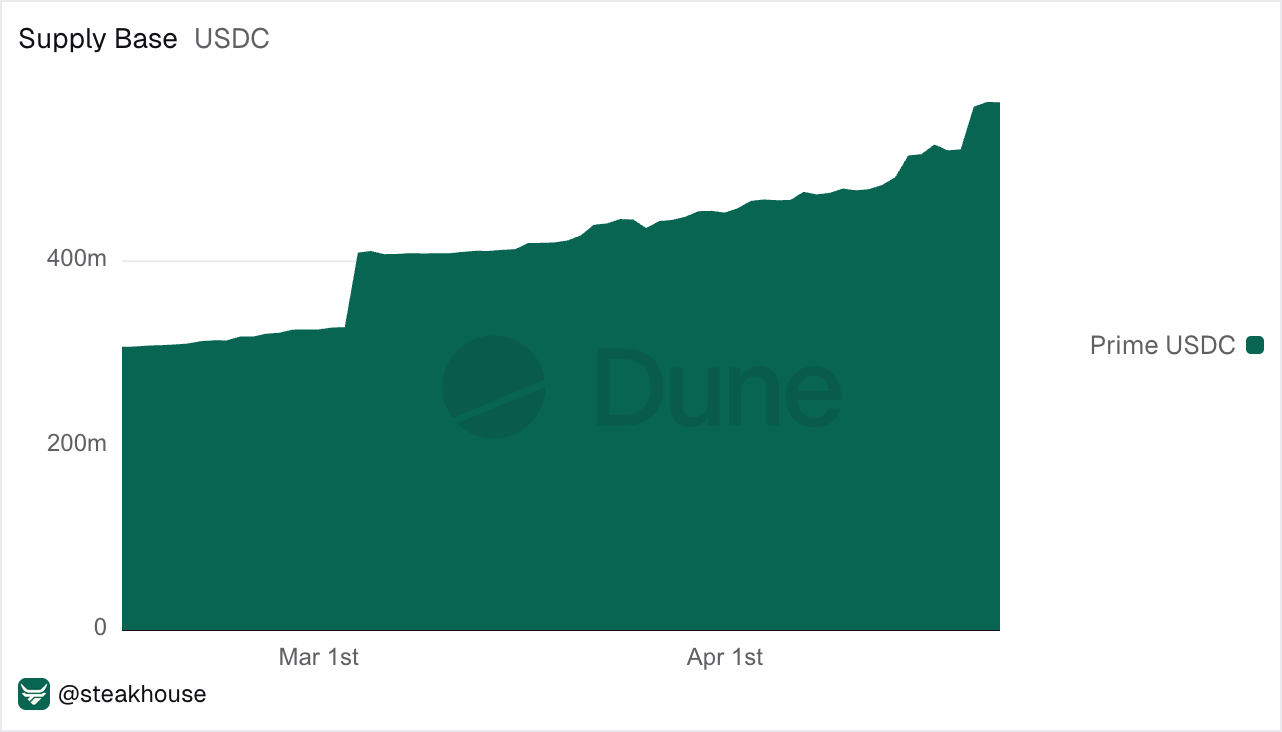

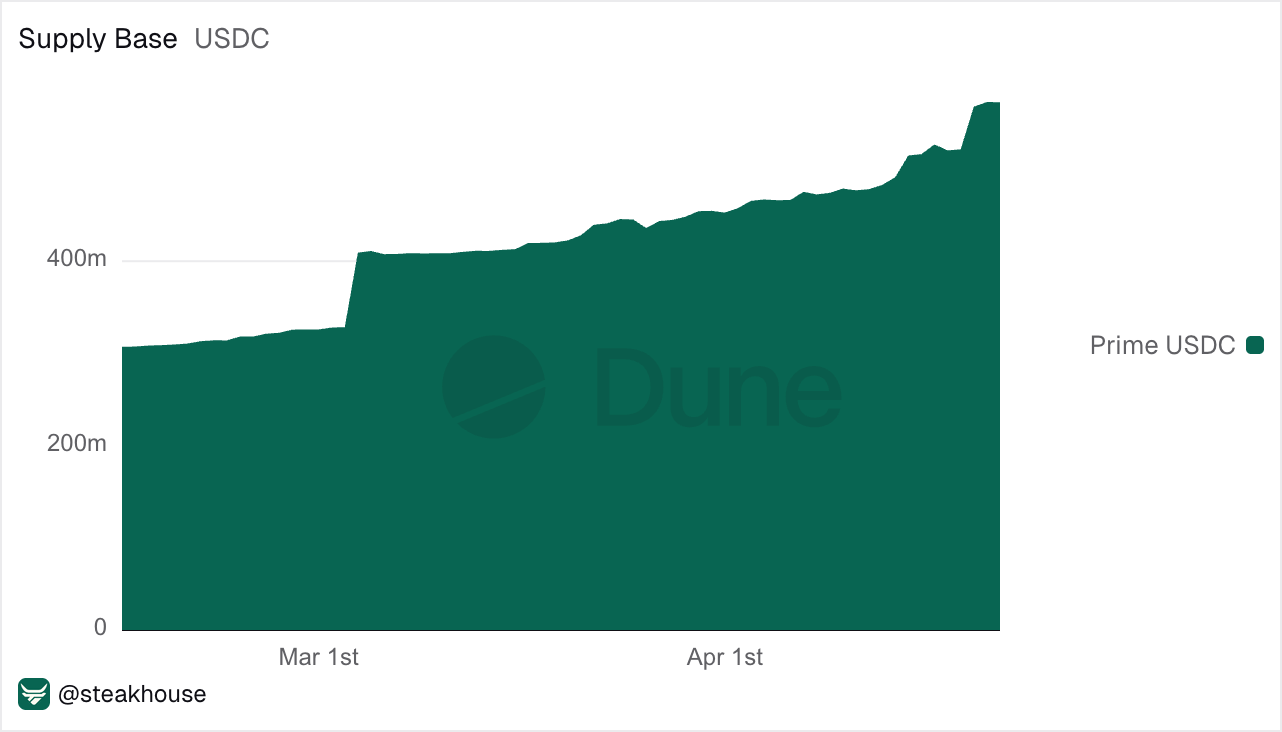

On Base, the pattern is similar. Prime continued to absorb new inflows as depositors repositioned, while Coinbase Borrow and broader Morpho activity on Base added further USDC demand. Together, those flows almost doubled the supply of our Steakhouse Prime Instant (link to V2 version) as it grew from $300M to $570M in just two months.

Stablecoin Spillovers to FX Markets

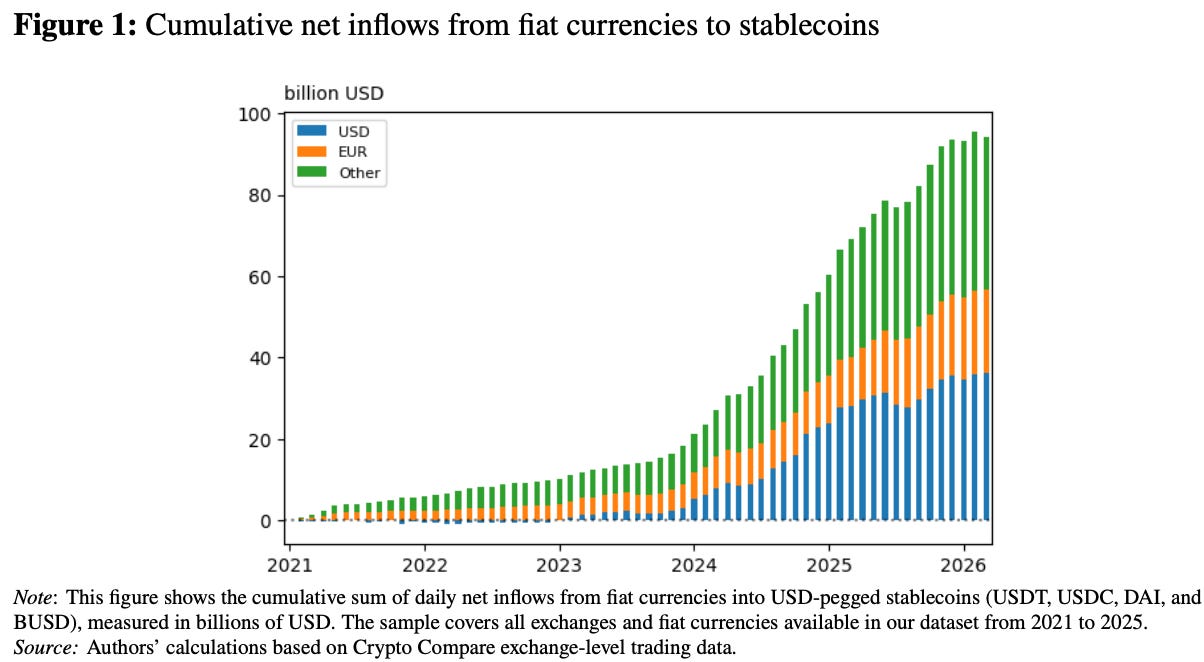

We examine the March 2026 BIS/IMF paper, Stablecoin Flows and Spillovers to FX Markets, which studies whether stablecoin activity leaks into spot FX and dollar funding markets. Stablecoins are overwhelmingly dollar-denominated, but the bulk of cumulative fiat inflows into them come from non-USD currencies, which means most stablecoin purchases embed an FX conversion and makes stablecoin venues a parallel FX market.

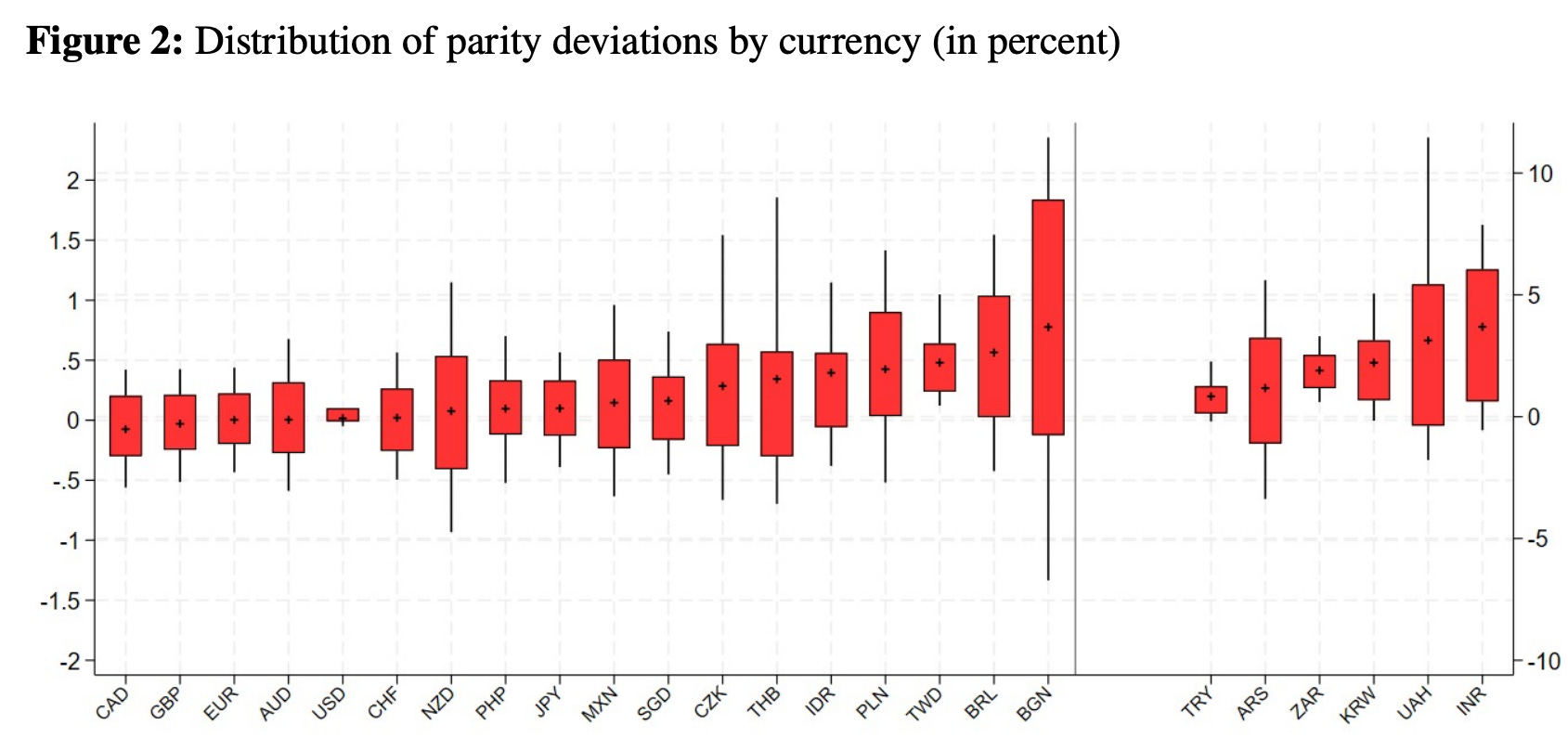

Someone holding local currency like the Argentinean peso (ARS) can acquire a stablecoin directly on a centralised exchange, or indirectly by first converting to USD in the spot market and then buying the stablecoin. In a frictionless market these two routes should cost the same, and any gap between them is what the authors call a parity deviation. Parity deviations are near zero for liquid developed-market currencies, like USD, but widen substantially in economies with macro instability or capital controls.

The model centres on an intermediary that facilitates dollar swaps in both the stablecoin market and the FX swap market, can be thought of as a market maker or dealer active across both markets. For example, when local demand for USDT rises, that intermediary sells the token, takes on the local-currency exposure, and uses up some of its capacity to absorb risk. As that capacity tightens, supplying dollars through swaps becomes more expensive too.

This is the paper’s main mechanism: stablecoin demand does not stay contained within crypto; it passes through the intermediaries that also help clear dollar demand elsewhere. That means pressure originating in stablecoin markets can feed into broader FX pricing, raising dollar premia and affecting exchange rates. The size of that spillover depends less on the token itself and more on the strength of the intermediary sitting between the two markets.

This market cost problem could potentially be solved once the GENIUS Act comes into effect, as bank subsidiaries and OCC-qualified nonbanks enter the stablecoin space and bring their FX desks with them, which means the intermediary slot the paper describes could increasingly be filled by entities like a JPMorgan subsidiary running matched stablecoin and swap books with more capital behind them.

Alongside bank subsidiaries, the December 2025 OCC conditional approvals of Circle, Ripple, Paxos, BitGo, and Fidelity Digital Assets for national trust charters point to a growing pool of regulated issuers. Whether the spillovers the paper measures remain meaningfully measurable in a post-GENIUS world is ultimately an empirical question for the next iteration of this research.

Furthermore, in February 2026, SEC staff added Q5 to its crypto-asset FAQ. Q5 lets broker-dealers treat qualifying payment stablecoins as liquid assets and apply only a 2% haircut when calculating net capital. That means a broker-dealer can hold qualifying payment stablecoins with only a small capital penalty. Hence, if regulated firms can hold stablecoins more efficiently, they can put more capital behind the intermediary role the paper describes, which could help the market absorb larger flows with less friction over time.

The paper shows that stablecoin flows affect FX through intermediary capacity, and the new SEC capital treatment, together with the GENIUS Act, could push forward a clearer federal framework for payment stablecoins. This suggests that stablecoin intermediation could become more institutional and easier to scale. The next phase of the market may therefore look less like a niche crypto venue and more like mainstream dollar plumbing built around stablecoins.