DeFi Markets Update 2026-03-26

Resolv, Yield Spreads, Cork’s Time-to-Cash Framework

Welcome to another DeFi Markets Update—your no-nonsense briefing on the cryptobanking plumbing and market pulse.

Resolv: RLP & USR DeFi Markets Exploited

On March 22, USR, a DeFi product designed to hold a $1.00 peg, was unfortunately exploited, creating $23.6m in losses. A compromised private key controlling a privileged signing account allowed the attacker to deposit about $200K into Resolv’s minting contract and receive around $80m of unbacked USR in return. The attacker then swapped the unbacked USR into ETH across DEXs, temporarily bringing the pool price down to $0.05 per USR and extracting the assets before Resolv paused protocol functions.

Contagion spread to lending markets on Morpho as they kept valuing wstUSR collateral at a hardcoded $1.13, assuming full peg, while the market price was well below this point. This created an arbitrage as people bought wstUSR at distressed prices and borrowed healthy USDC against it at full face value, which drained the vault’s liquidity.

According to Morpho, “there are ~15 vaults with non-negligible exposure (>$10k)” to Resolv that were impacted. None of which were Steakhouse vaults.

In Resolv’s dual-tranche architecture, wstUSR and USR are the more conservative (senior) tranche, while RLP serves as the riskier (junior) tranche. Steakhouse never accepted RLP as collateral; its concentrated junior tranche risk fell outside our framework for depositors.

Our systems flagged a 1.61% USR deviation at 02:21 UTC and were fully exited across all vaults by 03:02 UTC. With zero exposure, there were zero potential losses to depositors. Our published assessment identified the failure modes that materialised and the underlying collateral was not compromised, consistent with that view. Our full treasury is in our own products and our commitment to withdraw last predates this incident.

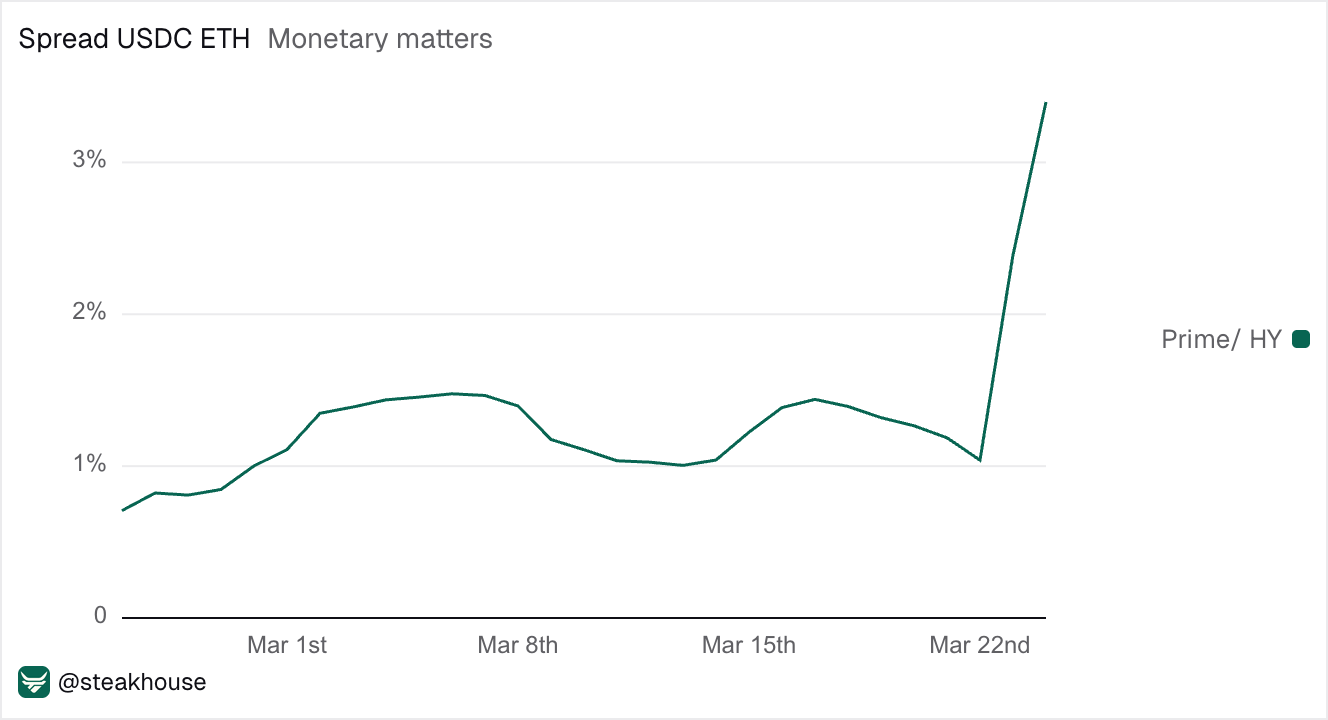

Spread Between Prime and High Yield USDC

Following the recent Resolv exploit, depositors have been more cautious around positions in riskier strategies, which reduced supply and mechanically increased yields. Throughout the situation, Steakhouse High Yield USDC Instant remained liquid for withdrawals.

Steakhouse High Yield USDC (and its v2 feeder vault) saw volatile TVL during the events, going from $61m to $37m. After derisking, deposits flowed back into our HY fund.

The overall TVL of this market is currently 64m, higher than pre-incident TVL, and the vaults are earning above 7% APY.

Currently, there’s a 3%+ spread between our High Yield and Prime USDC vaults on Ethereum Mainnet. USDC Prime Instant on Ethereum is tracking in the 3-4% range. This is suggestive of a persistent tick-up in cost of capital for onchain repo opportunities.

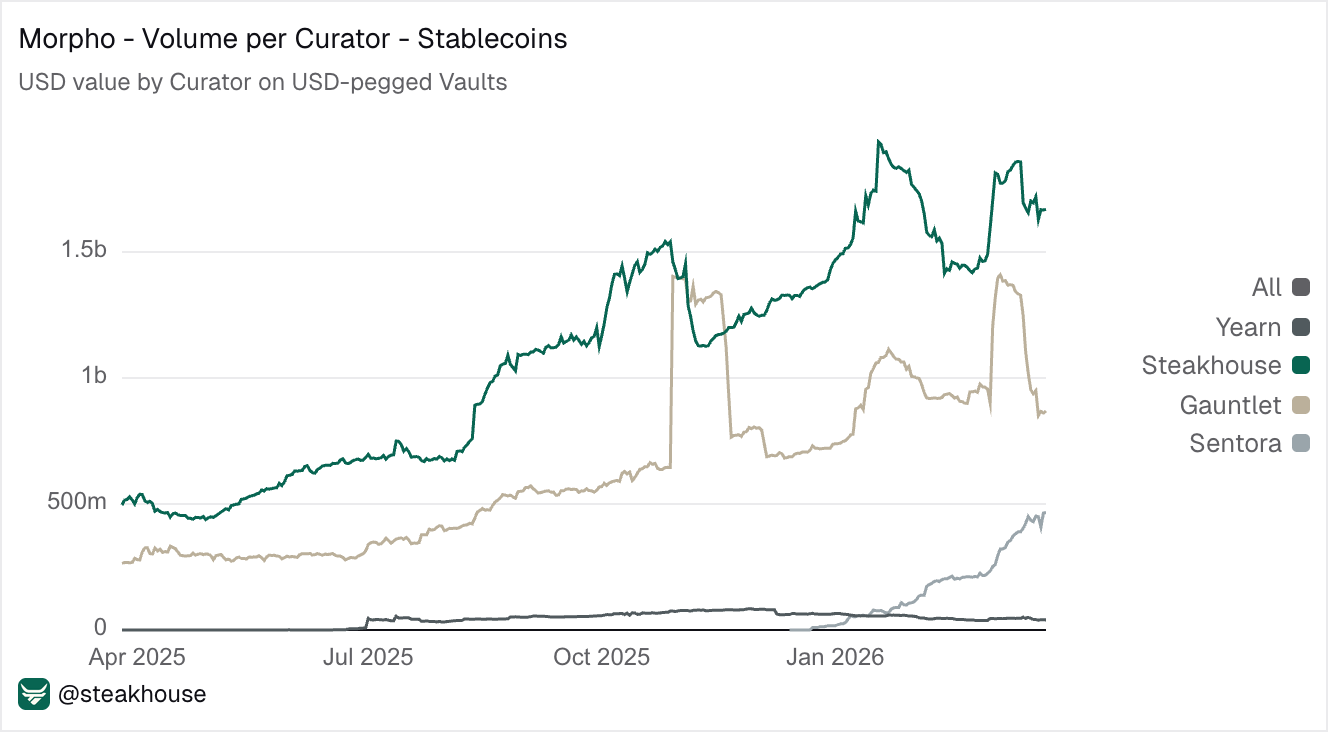

Steakhouse continues to hold the largest share of stablecoin deposits on Morpho.

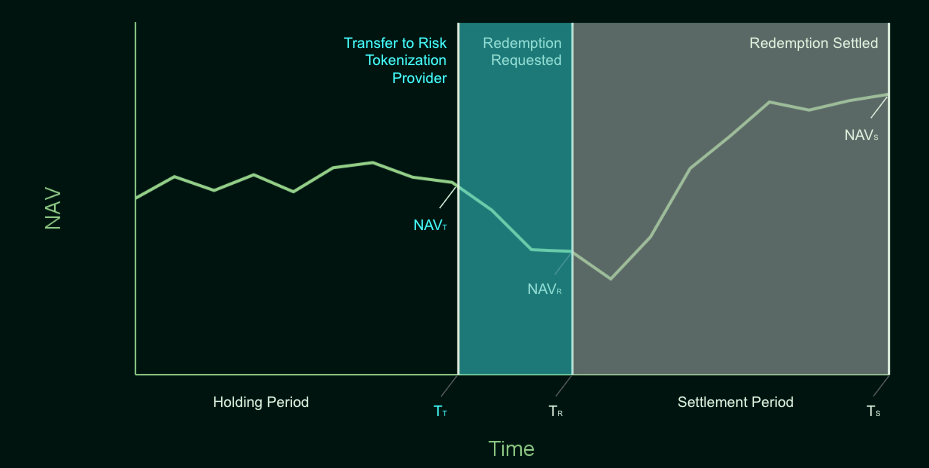

Cork’s Time-to-Cash Framework

In ‘Assessing Liquidity Risk in DeFi’, Cork’s team focused on a question that matters more and more as DeFi matures: How quickly does capital convert back into cash? Early DeFi was built on highly liquid collateral and near-instant settlement, so liquidity remained a background concern for most product design. That changed as the market expanded into RWAs, fixed-rate lending, cross-chain settlement, and structured vaults, where the path from redemption request to final cash can take a lot longer.

The main concept is the time-to-cash, which gives a practical way to think about liquidity risk onchain. The article defines time-to-cash as the period between asking for liquidity and actually receiving funds, and that period can include notice windows, settlement processes, withdrawal queues, and other operational delays. Once you look at an asset through this lens, the risk becomes more concrete because the question moves from “is this asset liquid” to “how long does exit actually take, and under what conditions”, including whether cash is received immediately at NAV or only after a settlement period.

Longer time-to-cash usually comes with a higher required yield, which is the illiquidity premium. Stablecoin positions with immediate redemption, a monthly-window fund, or a quarterly-redemption private credit product can all look income-generating, but the exit profile behind each one is very different. That makes liquidity part of the return stack, alongside credit risk and market risk, and it gives a clearer basis for comparing headline yields across asset types.

For example, an RWA may only let investors redeem monthly or quarterly, while a staking-linked asset may require time for validators to exit. A vault may need time to unwind positions before cash is available, and a cross-chain asset may depend on bridge and settlement timing. These are different sources of friction, but they all affect how long it takes to get your money out.

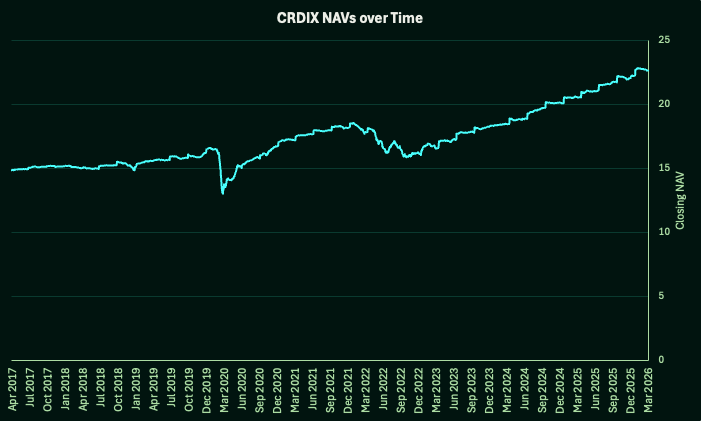

In products like CRDIX, a smooth reported NAV can still sit alongside a longer path from redemption request to cash. Once time-to-cash becomes longer or less predictable, it starts to shape which assets fit inside a product, how liabilities should be structured, and where extra yield is coming from.

The article notes that liabilities in DeFi often behave like instant deposits or on-demand redemptions, which creates a need for assets with matching liquidity. When the portfolio holds assets that settle more slowly, the system relies on liquidity sleeves, secondary markets, or staggered exits to keep withdrawals smooth. During heavier redemption periods, those mechanics become visible through capped exits, secondary discounts, slower settlements, and higher sensitivity to market depth.

As DeFi moves further into assets with slower settlement, liquidity deserves its own pricing framework alongside credit and market risk. The article goes deeper on the mechanics, examples, and implications across asset types, and is worth reading in full.