Resolv Protocol

Economic and Operational Overview

Update 2026-03-22: Unfortunately, one of the risks we highlighted in the below report materialized, leading to an exploit that allowed an attacker to mint new USR tokens. The collateral backing, thankfully, was not compromised and remains whole. Please refer to communications from Resolv Labs for more updates.

Steakhouse Financial has been engaged, on a fixed-fee basis, as a risk manager by Resolv. The mandate focuses on formalizing a unified risk framework (liquidity, market, concentration, duration risk), providing a governance review of collateral onboarding, venue exposure and building structured transparency and attestation dashboards. The below report provides our overview of the first few weeks examining Resolv in-depth.

Published in March 2026. Download the Full PDF

Resolv Protocol is a DeFi platform issuing USR, a stablecoin backed by a diversified basket of crypto money markets, and RLP, a risk‐bearing yield token. Together these form a dual-tranche structure: USR provides stable USD exposure with no directional crypto risk, while RLP acts as an insurance/equity layer that absorbs volatility and counterparty risks in exchange for higher returns.

Unlike other similar protocols, Resolv bifurcates its collateral pool into senior (USR) and junior (RLP) claims, delivering stable yield to conservative holders and leveraged returns to risk-tolerant liquidity providers. The following report presents a comprehensive economic and operational analysis of Resolv’s unique mechanics. We examine how collateral flows through the system, how delta-neutral exposure and payoffs are managed, the liquidity and correlation dynamics of its integrated venues, and the operational processes and failure modes that underpin Resolv’s stability.

1. Economic Analysis

The information herein is sourced primarily from the Resolv public docs and supplementary materials. For a complete description of the structure, including its risks, please refer to the governing documents directly.

1.1. Structure

Resolv is a stablecoin protocol with a two-token structure consisting of USR (a $1-pegged stablecoin) and RLP (the risk-bearing “insurance” token). This design separates conservative vs. risk-tolerant capital into different tokens. USR serves as a senior stable tranche (targeting 1 USD value), while RLP is a junior tranche that absorbs risk and earns higher yields. Economically, this structure lets USR holders enjoy stability and modest yield, whereas RLP holders take on extra risk (like market and counterparty risk) in exchange for a greater share of the profits.

USR (Resolv USD): A fully collateralized stablecoin pegged to $1. Its primary backing are on-chain assets grouped into a few distinct clusters, such as delta-neutral positions in ETH and BTC, DeFi lending, and RWAs. USR itself does not accrue yield unless staked (as stUSR), designed to make it a low-risk, stable asset. USR can be minted and redeemed 1:1 for USD value of collateral (e.g. $1 of collateral ↦ 1 USR).

wstUSR (Wrapped Staked USR): USR is a stablecoin that by itself does not accrue yield. However, holders can stake USR to earn native yield. When USR is staked, it is converted into a yield-bearing token. Staking USR first issues stUSR (staked USR), which is a rebasable token whose balance grows as rewards accrue. For ease of use in DeFi, stUSR is typically wrapped into wstUSR which represents staked USR in a non-rebasing format. Each wstUSR grows in value relative to USR over time as it accumulates staking rewards

RLP (Resolv Liquidity Pool token): A risk-sharing token that represents the excess collateral beyond the $1-per-USR backing. RLP acts as an insurance layer for USR – it covers any losses or shortfalls to protect USR’s peg. RLP’s price is not fixed but floats based on the net asset value of its backing (denominated in USD). Holders of RLP earn higher yield rewards (including a dedicated risk premium) for shouldering this risk. If losses occur, RLP’s value is written down first, preserving USR’s full collateralization

1.2. Delta Exposure for Minting and Redeeming

Resolv’s collateral pool is sourced from user deposits and allocated across multiple instruments and custody locations to implement its delta-neutral strategy. The key steps of the minting process are:

Stablecoin Deposit: A user deposits $x of liquid collateral (currently USDC or USDT) to mint either $x of USR or an equivalent value of RLP. Minting is done at a 1:1 USD value basis.

Swap to Allocation: The protocol uses the deposited funds to deploy into multiple USD-Neutral clusters including Delta-neutral ETH & BTC, Delta-neutral Altcoins, USD DeFi assets, RWA

On a cluster level, funds are deployed into a relevant money market strategy, for which the cluster is mandated. For example, in the delta-neutral cluster, the assets are exchanged into ETH. In parallel, Resolv opens a short using perpetual futures, sized to fully offset the assets acquired. For every 1 ETH added to the collateral pool, the protocol shorts approximately 1 ETH worth on a partner exchange or DeFi perps venue (e.g. Hyperliquid, Bybit, etc.). This hedge neutralizes price movements – if ETH’s market price rises or falls, the gain/loss on the long ETH is offset by an opposite loss/gain on the short contract. The net effect is that the portfolio value stays pegged to USD, enabling 1 USR to remain redeemable for ~$1 of collateral at all times without needing large collateral buffers for volatility.Minting Tokens: In conjunction to the above allocations, the user receives their tokens as either USR equal to the deposit amount (if they chose to mint USR), or RLP tokens equal in value to their deposit (if minting RLP). RLP minting mirrors USR minting operationally, but with a different economic outcome. The RLP collateral becomes “excess” collateral in the system (above what’s needed for USR backing). This increases the buffer protecting USR. Initially, 1 RLP token typically represents $1 of assets; over time its price will fluctuate as profits or losses accrue to the RLP tranche.

The redemption process follows closely but in the opposite direction:

Redeeming USR/RLP burns the tokens in exchange for a proportional share of the underlying collateral. For USR, this creates an unwind request that is submitted and fulfilled by the team. For RLP, the amount of stablecoins you get back equals # of RLP redeemed) * (current RLP price), minus any fees. For example, redeeming 10,000 RLP when price is $1.10 would return about $11,000 worth of assets. The protocol adjusts collateral requirements dynamically based on RLP’s price, so that redemptions and minting are always fair relative to the pool’s latest valuation.

Critically, RLP redemptions may be subject to certain guardrails to maintain the system’s capital adequacy. Because RLP acts as the buffer protecting USR, the protocol monitors the ratio of RLP pool value to USR outstanding, akin to a capital adequacy ratio. Withdrawal limits or delays can kick in if too much RLP tries to exit at once, ensuring that after RLP redemptions, the remaining collateral still fully backs all USR in circulation. This design prevents a scenario where RLP holders could withdraw and leave USR under-collateralized.

1.3. Yield Generation

Once users have minted USR or RLP and the protocol has allocated the collateral, Resolv’s system enters a steady-state of delta-neutral yield generation. The economics hinge on the fact that the collateral assets (e.g. ETH) produce yield, and the short hedge can also produce or cost funding, all while the net value remains stable in USD.

Key components of Resolv’s collateral yield strategy include:

Staking Yield: The majority of ETH collateral is held as yielding ETH (e.g. in liquid staking derivatives like Lido or in native staking or direct lending on Aave). This earns regular staking rewards (currently on the order of ~2-3% APY for ETH). Those rewards increase the total ETH in the collateral pool over time, effectively boosting the backing for both USR and RLP. Since USR is fixed to $1, these extra earnings are split to accrue to staked USR and RLP holders as “excess” collateral once credited (hence raising wstUSR and RLP’s price). Staking yields provide a base level of profit to the system, derived from securing the Ethereum network.

Funding Fees from Shorts: By holding a short perpetual position against the long spot, the protocol may earn or pay funding rate payments. Historically, typically longs pay shorts, resulting in the short side (where Resolv is) receiving periodic funding fees. Historically, funding on ETH/BTC perps ranges around ~10% of annual yield when positive. However, if market sentiment flips, shorts might pay funding to longs (a cost to Resolv). The protocol’s design aims to manage this by possibly adjusting hedge venues or relying more on staking yields during such times.

Other Yield Streams: Resolv also deploys portions of the collateral in DeFi money markets or RWAs to enhance returns, as long as they remain USD-neutral. For example, a portion of assets could be lent on Aave/Morpho or put into tokenized real-world assets (like treasury bill tokens) to earn interest. Allocations are made while making sure to preserve high liquidity and safety. In essence, Resolv’s treasury management seeks diversified yield (staking, lending, funding fees) to maximize return without jeopardizing the peg or taking directional bets.

1.4. Yield Payoff

Resolv splits the earnings (or losses) of the collateral pool between USR, and RLP holders and the treasury in a structured way to align incentives:

USR Stakers (Conservative Tier)

USR itself is a stable utility token and does not automatically accrue yield. However, users can opt to convert into stUSR and wstUSR to receive yield distributions. Staked USR and RLP together are entitled to a portion of the protocol’s profits (the “Base Reward”) each epoch (24 hours). After a 10% protocol fee is deducted, 76.5% of each epoch’s profit is shared pro-rata between stUSR and RLP holders as the Base Reward. This parameter was updated in early 2026 from the original 70% base / 30% risk premium split (with no protocol fee) via a phased six-week transition. USR holders must stake to get this reward; if they don’t, they simply hold a stable token with no interest.

In times of loss, USR holders are protected – no losses are taken from USR, and unstaked USR never dips below $1 in value because redemptions are always honored at $1 so long as RLP capital is available. This makes USR a low-risk asset suitable for those who prioritize stability but with the option of moderate yield (by staking).

RLP Holders (Risk Tier)

RLP holders receive the lion’s share of rewards due to the higher risk they bear. In addition to their pro-rata portion of the 76.5% Base Reward, RLP exclusively earns 13.5% of profits as the Risk Premium each epoch (with the remaining 10% going to the protocol treasury as a fee). This boosts RLP’s effective APY significantly.

For example, if RLP comprises 30% of total staked assets and USR 70%, RLP would receive 30% of the 76.5% Base Reward (i.e. 22.95% of profits) plus 100% of the 13.5% Risk Premium – totaling ~36.5% of all profits in that scenario (while only representing 30% of capital). USR stakers would receive the remaining ~53.6%, with 10% going to the protocol treasury.

Note that RLP also fully absorbs any losses: if an epoch ends with a negative return (e.g. due to adverse funding rates or other costs), 100% of that loss is deducted from the RLP pool’s value (reducing RLP price) and USR holders receive nothing negative. RLP is essentially the first-loss capital that insures USR such that USR remains fully backed. In return, RLP is rewarded with outsized profit share during good times. This risk-reward profile attracts users who are comfortable with volatility and seeking high yield.

Economic Example

Suppose the system has $200M USR (staked) and $100M RLP. In a day, the collateral pool could earn $82.2k from staking and funding (~10% net interest). From this $82.2k yield, $8.2k (10%) goes to the protocol treasury as a fee. Of the remaining $74.0k, $62.9k (76.5% of total) is the Base Reward split pro-rata between staked USR and RLP, and $11.1k (13.5% of total) goes entirely to RLP as the Risk Premium.

From the above table, you can see how on this example epoch day, the net $300m of TVL earning 10% collectively ended up split into staked USR yielding 7.7% and RLP holders earning 11.7%.

1.5. Points Incentives and Airdrop Rewards

Resolv historically employed a seasonal Points Program to reward user participation, effectively converting user activity into future token yield. Each season allocates a portion of the total $RESOLV token supply as an airdrop, distributed in proportion to points earned by users.

Season 1 rewarded early adopters with 10% of the total token supply (100 million tokens) distributed via airdrop. Season 2 followed with an allocation of 5% of the supply (50 million tokens) for its airdrop pool. Subsequent seasons have continued this trend on a diminishing scale; for example, Season 3 distributed 3% of supply – reinforcing long-term engagement while avoiding excessive immediate dilution.

These token rewards acted as a powerful incentive tool as users earned not only interest from USR/RLP positions but also “bonus” yield in the form of points that convert to governance tokens. In essence, the prospect of sizable airdrop rewards boosts the effective APY for participants and has been a key driver of user involvement.

Points are earned by performing various actions that support USR and RLP’s ecosystem – such as holding or staking USR, providing USR liquidity, or holding RLP in the protection pool. Different actions earn different amounts of points, and the Resolv team can choose to adjust these point distributions as they like to reward ecosystem favorable behaviors. For example, if they want there to be deeper secondhand USR liquidity, they can choose to allocate more points to USR/USDC liquidity pools to encourage more LPs.

To maximize points (and thus their share of airdropped tokens), many users employ leverage and looping strategies. For example, a user can deposit USR as collateral on a lending platform (e.g. Morpho or Euler) and borrow USDC against it, then swap the borrowed USDC for more USR to deposit again. By repeating this loop, the user dramatically increases their USR position (while staying largely delta-neutral since both assets are USD-pegged), which in turn multiplies the points they earn.

Some top point-maximizing strategies involved leveraged USR/RLP positions on protocols like Fluid, Morpho, and Euler, achieving up to a ~10× points multiplier through aggressive looping. Users also pursued yields on Pendle by acquiring wstUSR/RLP YT (yield tokens), which simultaneously generated base yield and points rewards. These tactics became common as participants sought to “farm” as many points as possible before each season’s snapshot. While such leverage amplifies rewards, it does introduce risks (liquidation or interest costs), so only savvy users with higher risk management engage at higher multiples.

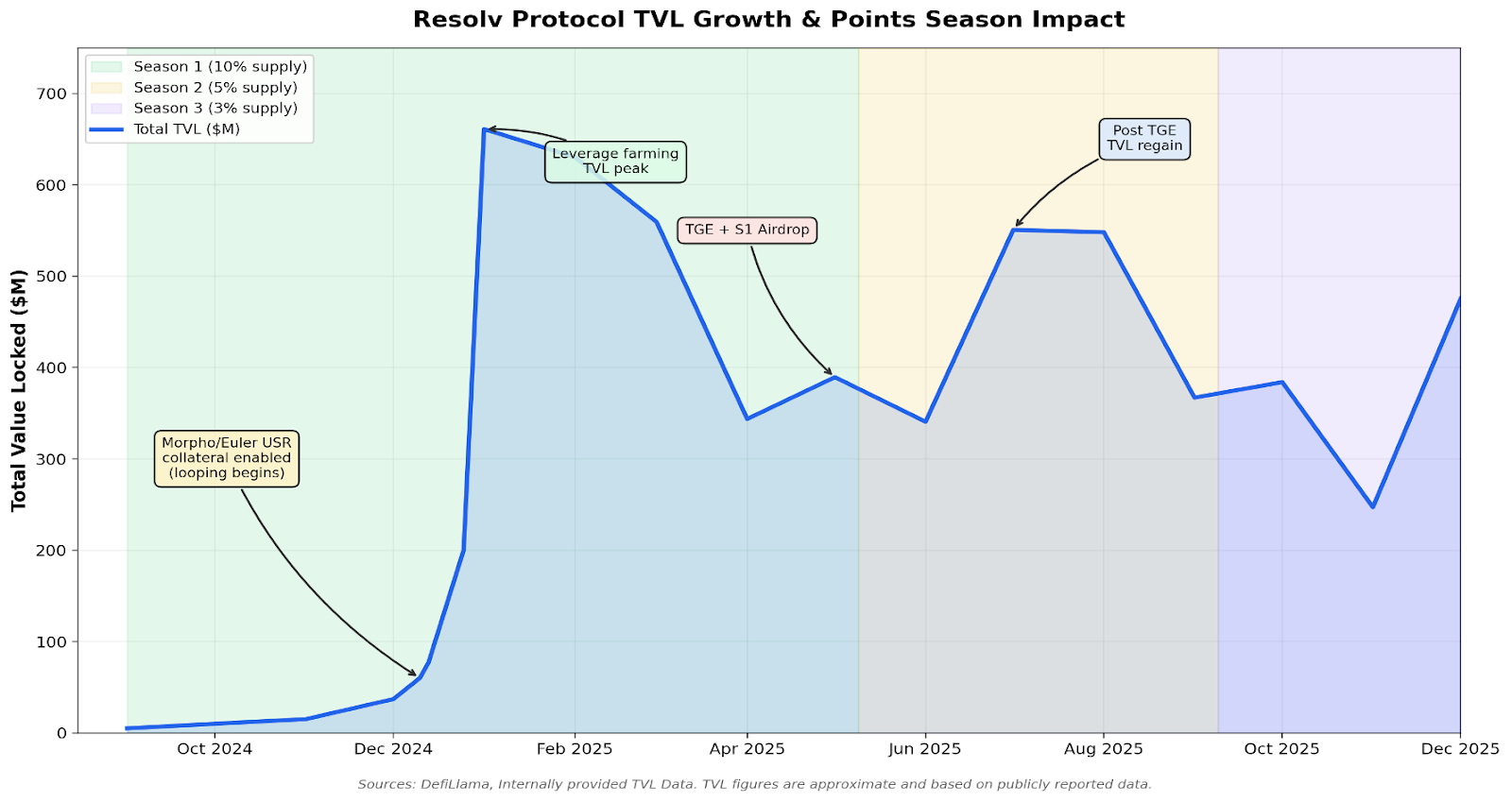

The impact of these point incentives on protocol growth and user behavior has been substantial. By offering significant token rewards, Resolv rapidly attracted liquidity and users – effectively jumpstarting network effects.

The chart above illustrates the direct causal link between points incentive seasons and TVL growth. Season 1 (10% of RESOLV supply) catalyzed explosive growth from under $50M to over $650M in under three months, driven primarily by the enabling of USR as collateral on Morpho and Euler which unlocked leverage looping strategies. Following the TGE and Season 1 airdrop distribution, TVL contracted by approximately 40–45% as yield farmers exited positions. Season 2 (5% supply) and Season 3 (3% supply) incentives helped plateau TVL. This pattern is consistent with incentive-driven growth curves seen in other basis trading protocols like Ethena, and represents a key risk factor: a significant share of TVL may not be “sticky” capital and may exit upon incentive exhaustion. With the points program now concluded, this thesis is actively being tested as the protocol transitions to liquid incentives.

1.6. Liquidity Pathways

A critical aspect of any protocol is how liquidity flows in and out – both under normal conditions and stress. Resolv’s liquidity pathways can be summarized as follows:

Primary Market (Mint/Redeem):

Users can always interact with the protocol contracts to mint new USR/RLP (by depositing collateral) or redeem USR/RLP (withdrawing collateral). This provides base layer liquidity. USR is soft-pegged by this mechanism: if market price deviates, arbitrageurs can create or destroy USR via the 1:1 collateral window to profit, thus pushing the price back to $1. USR redemptions are typically honored within 24 hours via the standard process. Additionally, Resolv offers instant USR redemptions subject to a daily cap and a small fee, funded by idle USDC in the Treasury or temporary Aave borrowing.

The delay in some cases usually relates to converting staked assets or unwinding futures if needed. The on-chain liquidity buffer is intended to fulfill most redemptions quickly without having to wait, for example, for a Lido unstaking period.

Additionally, Resolv can maintain liquidity by borrowing against staked assets – e.g. using stETH as collateral to borrow ETH from DeFi lending markets – ensuring that even if a large portion of assets are staked (with days-long withdrawal times), the protocol can access immediate liquidity to redeem users if needed. This is an important operational pathway: essentially transforming illiquid yield assets into liquid funds when needed via DeFi money markets.

Secondary Market Liquidity

USR, as an ERC-20 token, trades on secondary markets (DEX pools, CEX listings) for convenience. The presence of the primary arbitrage mechanism (mint/redeem) typically keeps secondary market spreads tight around the peg – any drift invites arbitrage. RLP also trades on secondary markets, allowing investors to enter/exit without directly calling the slow redemption function.

However, secondary liquidity for RLP will depend on demand; since RLP’s price can fluctuate and has fewer holders (risk seekers), its market might be less liquid than USR’s. Resolv’s approach to fostering RLP liquidity has included incentivizing liquidity pools in the past and additional points incentives for such.

Liquidity for Hedging Operations

Another facet is internal liquidity for rebalancing. When the protocol needs to adjust futures positions or margin, it requires available capital. Resolv’s design ensures a portion of assets is always liquid (unstaked or in stable form) as a buffer. If crypto prices spike and more margin is needed on exchanges, Resolv can pull from this buffer or quickly swap some assets to stablecoin to post margin.

Conversely, if prices crash and positions are in profit, Resolv will withdraw excess margin back to the buffer. This flow of liquidity between on-chain reserves and exchange collateral is managed via the custodial accounts (Fireblocks/Ceffu) which allow near-instant transfers to/from exchanges. Essentially, Fireblocks and Ceffu act as bridges that can swiftly move collateral in response to exchange margin needs, avoiding the delays of traditional banking. This operational liquidity pathway is critical in volatile conditions to prevent forced liquidations.

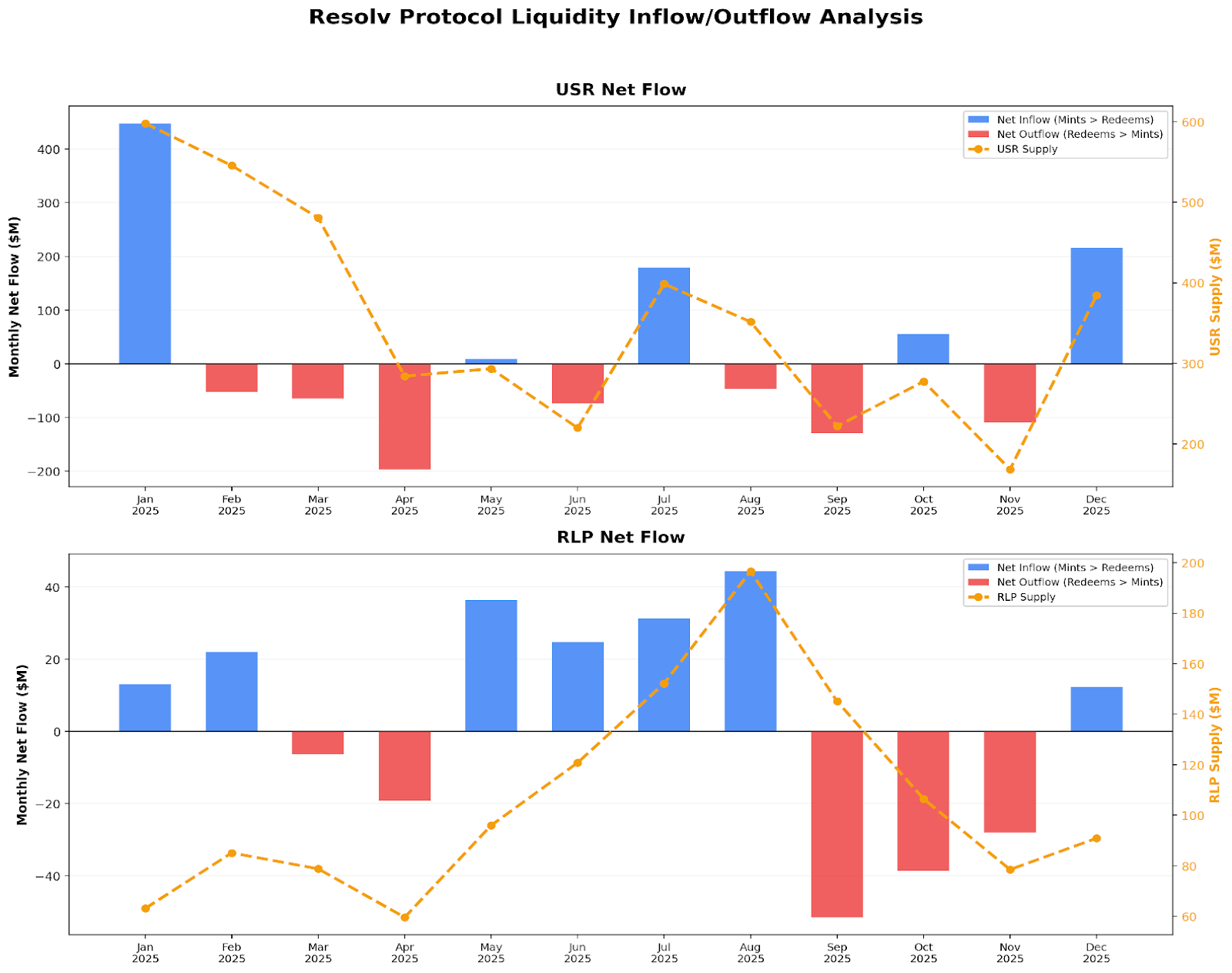

Below is an analysis of USR and RLP Inflow/Outflow across 2025 using the TVL chart from above. This highlights explosive USR & RLP growth to start the year as leverage was introduced before plateauing off as 2025 continued.

1.7. Correlation and Co-Movement Across Integrated Venues

Resolv sources its delta-neutral yields from multiple venues (staking and several futures exchanges). Understanding the correlation and co-movement of yields and risks across these venues is key to evaluating Resolv’s stability.

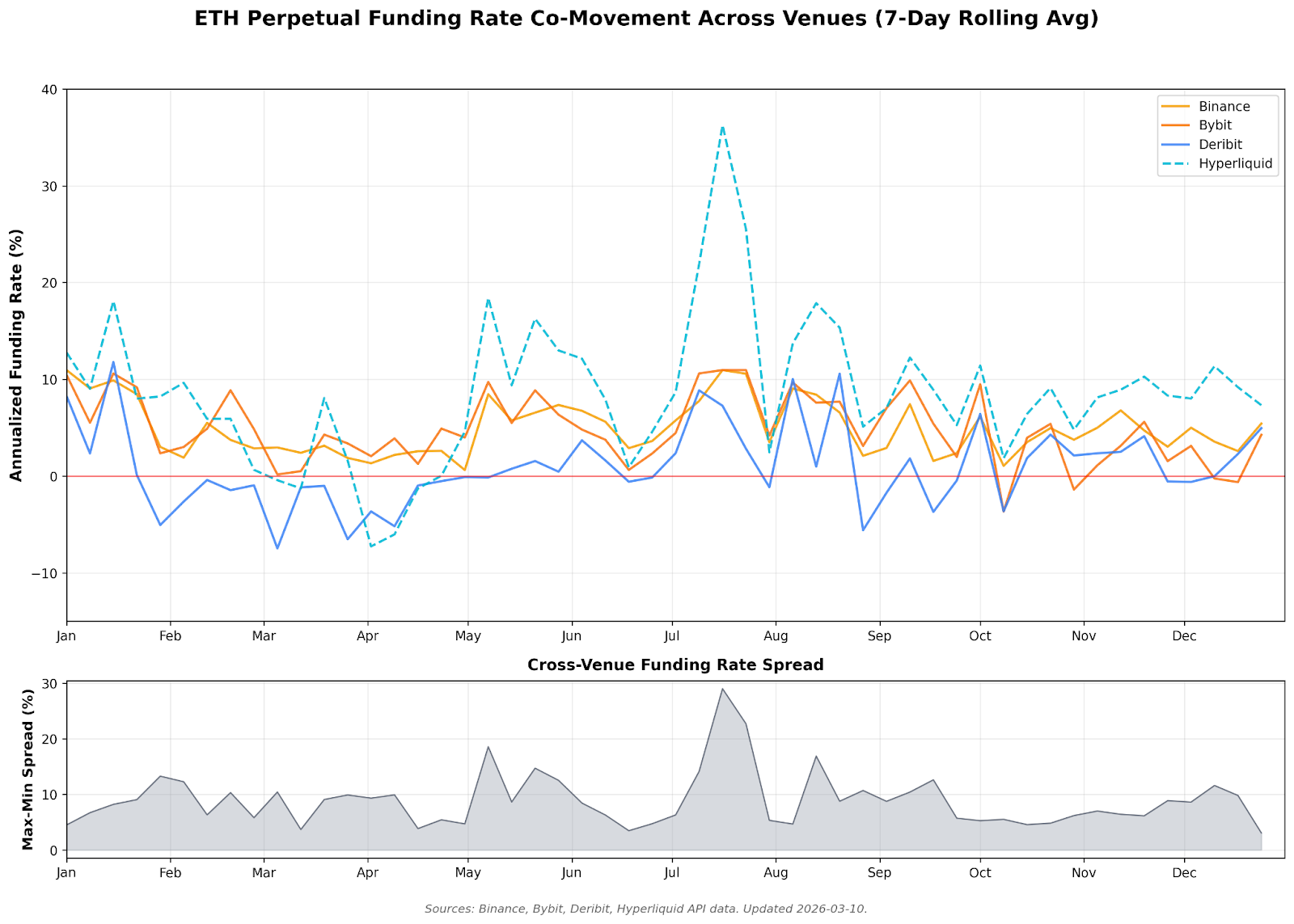

Funding Rate Co-Movement

Funding rates for BTC and ETH perpetuals are broadly driven by market sentiment. Thus, there is a high correlation in the direction of funding moves across venues as in a market-wide downturn, most exchanges’ funding will compress or turn negative together. While exchanges follow the same broad trends, there are material differences in average funding and volatility by venue.

By allocating futures across various exchanges like Binance, Bybit, Deribit, and Hyperliquid, Resolv can achieve a blend close to actual efficient operations. This diversification means Resolv is not overly exposed to an idiosyncratic funding event on any single exchange. If one venue’s rates go negative due to a localized issue, the others might still be positive, smoothing the overall yield. Correlation of funding income is high but not perfect, so diversification reduces variance of the composite yield.

Exchange Credit Event Correlation

The risk of exchange failure is another area of possible co-movement as a broad market crash could stress multiple exchanges simultaneously (as seen in events during the Bybit hack during February 2025). Resolv mitigates by using independent custodians and aiming for low exposure, explained more in the operational analysis.

Staking Yield vs Funding Correlation

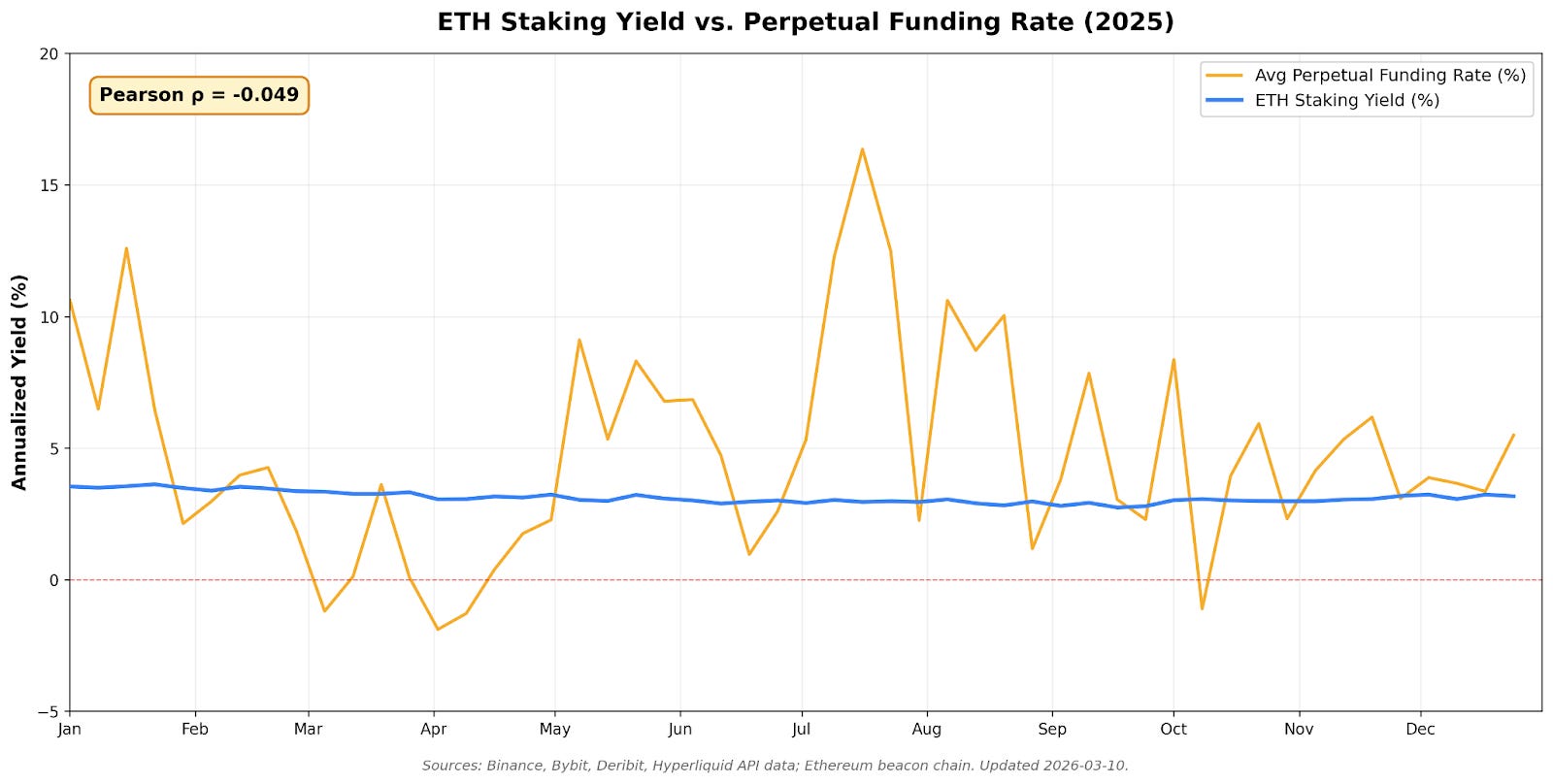

Two of Resolv’s main yield sources – ETH staking rewards and perp funding fees – are uncorrelated to a large extent. Staking yield is relatively stable (set by network parameters and overall ETH economics) and tends to slowly vary (recent range ~3–3.5% APY). Funding fees, conversely, are highly sensitive to market conditions and can swing from strongly positive to zero or negative.

The above analysis confirms statistically insignificant correlation (ρ ≈ -0.049) between ETH staking yield and perpetual funding rates, validating the diversification thesis underlying Resolv’s dual yield strategy. This lack of correlation is beneficial: during some periods when trading yields are low (bear markets with flat or backwardated futures), staking yields continue to accrue, providing a baseline return. In bull markets with rich futures premiums, funding yields spike, adding to staking returns. In stress scenarios, funding could be slightly negative, but staking would likely still produce positive yield, offsetting some losses.

Price Correlation of Collateral Assets

The collateral includes ETH, BTC, and other stable assets. BTC and ETH prices are closely correlated, often moving in tandem. It’s important to note that with respect to stETH vs ETH liquidity, in extreme conditions, stETH (Lido Staked Ether) can trade at a slight discount to ETH. If Resolv needed to quickly liquidate stETH for ETH, a large depeg could impair liquidity or value. This is a risk if, say, many are exiting stETH at once, Resolv’s mitigation is to keep some portion of ETH not staked and to allow time for redemptions (24h window) which could include swapping stETH gradually.

1.8. Worst-Case and wind-down Scenarios

Under normal conditions, both USR and RLP can be redeemed freely. In a severe stress scenario, additional measures kick in. As already noted, if the collateralization drops too low, RLP redemption halts. USR redemption would presumably remain open unless the situation is so dire that even USR might be impaired (which the protocol is architected to avoid – it would require both RLP to be fully wiped out and further losses beyond that, an unlikely scenario given the conservative hedging and downside risk management).

More likely, in a situation like an exchange default or a sudden large loss, USR redemptions might temporarily queue so that the team can assess and reallocate remaining collateral to honor $1 redemptions fairly. The primary withdrawal “surface” to monitor is RLP run risk as a large exodus of RLP could reduce the cushion. Resolv handles this by dynamically adjusting yields (to entice RLP to stay or join) and by outright blocking redemption if it would compromise USR backing. This is analogous to gating redemptions for a fund’s junior shares during crisis to protect senior claims.

The most common risks include counterparty risk where the assets Resolv holds (Defi lending, RWAs, stablescons, exchanges, etc.) encounter a hack or insolvency, as well as interest rate risks (funding rates, defi lending, RWAs). Below are some scenarios and their projected responses to the most common risks.

Exchange Insolvency (Counterparty Failure)

Perhaps the most drastic scenario for Resolv is a major exchange (or multiple) becoming insolvent or inaccessible (e.g. sudden shutdown or hack like FTX). In this event, any margin collateral and unrealized P/L on that venue could be lost. Resolv mitigates this risk by safekeeping trading margin for centralized exchanges with third-party custody solutions, such as Fireblocks and Ceffu. However, there is a remaining risk for funds held directly with exchange infrastructure (e.g. margin deposited to smart contracts of Hyperliquid, or unrealized PnL owed by the exchanges to Resolv).

Similarly, a meaningful share of Resolv’s collateral pool is deployed into decentralized lending markets (currently, Aave, Fluid, and Morpho are allowlisted). While these protocols are among the most battle-tested in DeFi, they carry distinct counterparty risks: smart contract exploits, oracle manipulation, or governance attacks on the lending protocol itself could result in partial or total loss of deposited assets.

RLP Absorbs Loss

The immediate economic loss – say exchange X held 5% of total collateral as margin and unrealized profit – would be deducted from the collateral pool’s value. This hits RLP exclusively: RLP price would drop to reflect the missing assets, potentially by a significant percentage if losses are large. USR remains fully redeemable from remaining on-chain assets; the system essentially “eats” into RLP’s insurance layer.

Maintaining Peg

USR redemption might be temporarily paused or limited if multiple exchanges failed at once and there’s concern about asset recovery, but assuming enough on-chain collateral remains to cover USR (which is the intent – Resolv keeps on-chain backing ≥ 100% of USR), USR should hold at $1.

If RLP is mostly or completely wiped out by the loss, the system enters a state of zero protection layer. The FAQ notes that even if the protection layer goes to 0, “no loss of value of the stablecoin” occurs – USR is still redeemable for $1 equivalent. However, going forward, USR would temporarily become an un-overcollateralized stablecoin until more RLP liquidity comes in. In that state, any further losses (e.g. another exchange failure) would directly threaten USR, so likely the protocol would freeze new USR minting and aggressively incentivize RLP recapitalization.

Operational Response

Resolv would attempt to close any remaining positions on that exchange via emergency (if possible) or recreate hedges on other venues to maintain delta neutrality. Fireblocks/Ceffu might help in claiming any recoverable funds from the failed exchange’s estate. This scenario effectively tests the soundness of the design: as long as total exchange exposure was limited and RLP had at least that much value, USR holders should come out whole.

Prolonged Negative Funding / Yield Drought

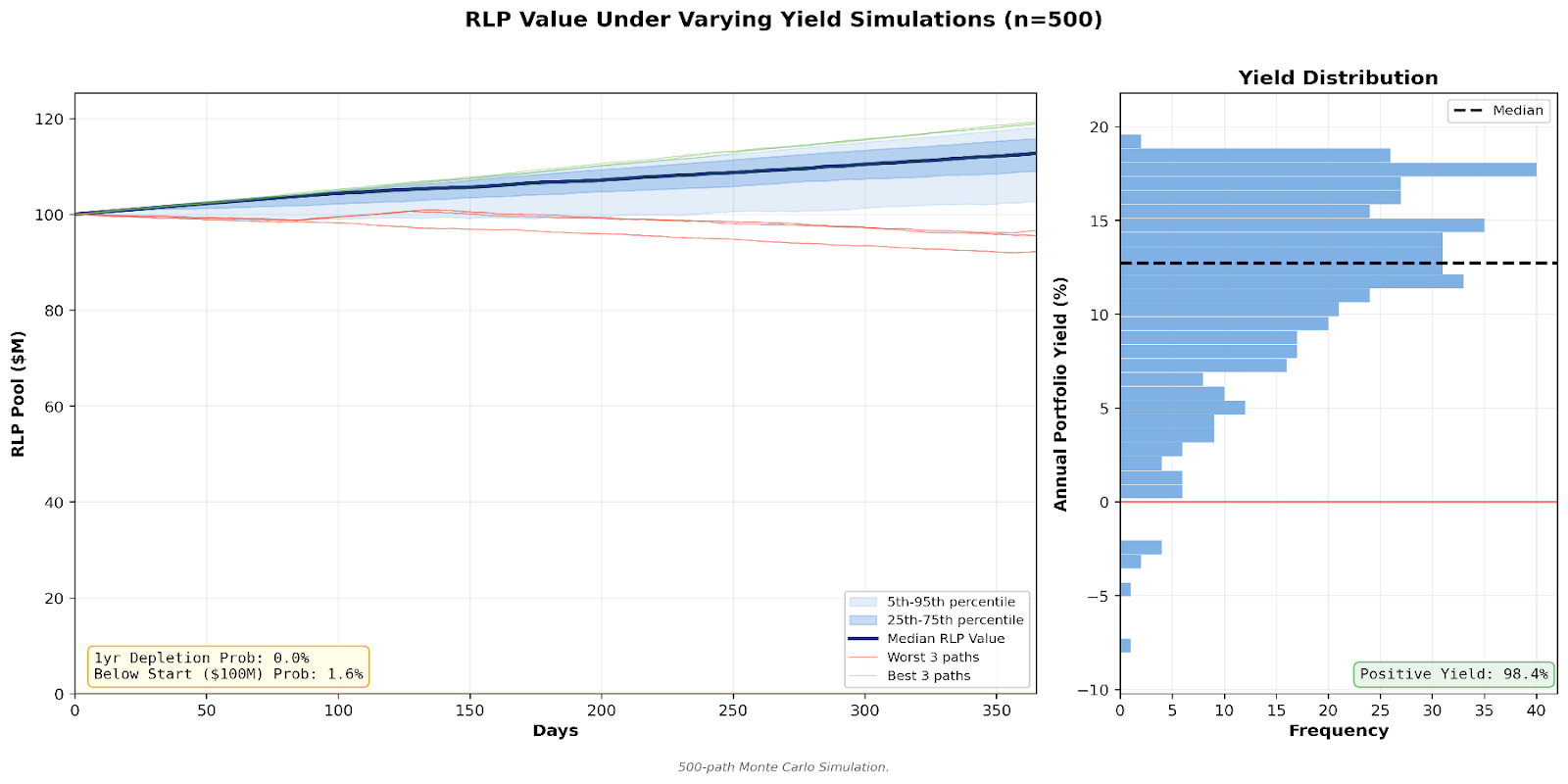

In a scenario where crypto markets enter a long stagnation or backwardation, futures will trade below spot (negative funding), and staking yields drop (perhaps due to protocol changes or slashing events). In such a case, Resolv’s strategy could turn net negative-yielding – paying funding while earning minimal staking return. If this persisted, the collateral pool would slowly bleed value. For other yield-generating assets of Resolv, such as positions in DeFi lending venues and fixed income RWAs, the situation can be similar in a low rate environment.

RLP is designed to cover any yield shortfall. Each epoch that realizes a loss would reduce RLP’s price. USR stakers would get zero yield in those epochs (but their principal remains $1). Over a long period, RLP could lose value – effectively subsidizing the stablecoin’s rate. The question is whether RLP could deplete entirely if the negative carry persists.

Above, a hypothetical Monte Carlo simulation was conducted using data extrapolated from the 2025 funding and staking data previously presented, with each of the 500 paths (standard n simulation) being a hypothetical yield scenario after one year. Overall, in a situation where a majority of the net yields were positive, even if there are days of negative yield, the chances of the entire pool of RLP being wiped are virtually 0.

Additionally, note that if RLP approaches depletion, new investors might actually step in because a thinner protection layer means the next uptick in yields will disproportionately reward them. The protocol’s self-correcting incentive is that the thinner the RLP layer gets, the higher its prospective yield, which should attract replenishment capital.

Due to diversification of possible allocations enabled for the collateral pool, in such scenarios Resolv would also aim to reposition its assets into a combination of other money market instruments in DeFi and real-world assets.

Governance might also respond by adjusting fees or allocations to support RLP. This lever has already been exercised, with the yield distribution parameters updated in early 2026. In the absolute worst case where RLP goes to zero and funding is still negative, USR could become undercollateralized. That is essentially a failure of the stablecoin (it would no longer be fully backed). However, long before reaching that, Resolv would likely halt USR minting and potentially wind down operations (allowing USR holders to redeem what remains, and effectively dissolving the project).

Mass Redemption or Bank Run

Consider a scenario where, due to external fear or market panic, a large portion of USR holders and RLP holders all rush to exit (maybe triggered by rumors or a black swan event). This is a liquidity stress test. For USR, because it’s fully backed, in theory everyone could redeem $1 for $1 of collateral until all collateral is gone. The only issue would be if some collateral is not instantly liquid (e.g. staked ETH needing days to withdraw).

Resolv’s mitigations include a 24-hour redemption window allowing staggering and using liquidity buffers to meet most requests. If needed, Resolv’s operators can tap DeFi loans (as mentioned, borrowing ETH against stETH) to meet redemptions quickly. In an extreme, they might even perform an emergency partial unbond of stETH (taking the withdrawal delay but communicating to users the timeline).

Because USR is over-collateralized, even a full redemption of all USR should be possible: users would end up withdrawing essentially the entire pool of assets, leaving only RLP. The design forbids RLP from redeeming in such a situation – RLP can’t be redeemed until USR is above 110% collateralized. RLP holders in a bank run scenario are effectively last in line and could remain stuck.

They might trade RLP on secondary markets at fire-sale prices, but the contract won’t let them redeem at primary if it would negatively impact USR holders. This is by design, as RLP is the safety buffer for USR holders. A mass redemption would play out with USR holders getting priority claims on all liquid assets and RLP being left with whatever remains.

If USR holders fully clean out the pool (less likely, because presumably some RLP value was present), RLP holders end up with nothing. This is the intended outcome: the stablecoin holders are protected even in a run, at the expense of RLP capital. The rules are clear: RLP’s gate closes at CR <110%, so RLP withdrawals freeze and only USR can continue to redeem. This ensures no “race” between tranches.

Smart Contract Exploit or Oracle Failure

Although not an “economic” scenario per-se, it’s a worst-case scenario to consider nonetheless. If Resolv’s smart contracts were exploited (e.g. a bug allowing an attacker to withdraw funds) or if the price oracle’s feeding values were manipulated (causing misvaluation of USR or collateral), the protocol could suffer a sudden loss of assets or erroneous redemptions.

To mitigate these risks, Resolv relies on reputable oracles and employs safeguards through sanity checks and multi-source pricing. As with all protocols, an exploit could still circumvent the economic design entirely. These mitigations are primarily preventative, utilizing multiple security audits and using time-tested components for token minting and redemption logic.

Resolv is designed to handle a range of crises via automated mechanisms (pausing certain redemptions, rebalancing collateral, using RLP as a buffer, etc.) and via a diversified approach (multiple exchanges, sources of yield). However, these scenarios also stress that the ultimate backstop is RLP capital – if losses exceed RLP, the stablecoin could impair USR holders. The protocol’s parameters (like maintaining low exchange exposure and >110% collateral ratio) are designed to make that outcome unlikely, though it is not impossible.

2. Operational Analysis

The information herein is sourced primarily from internal due diligence with the team, official documentation, and supplementary public materials. For a complete description of the operational structure, including its risks, please refer to the governing documents directly.

2.1. Contractual Structures

Resolv’s operational structure spans on-chain smart contracts and off-chain agreements with custodians and exchanges. Unlike traditional fund structures that rely on legal frameworks and appointed service providers, Resolv is implemented as a protocol with contractual logic embedded in code and other elements managed via governance and partnerships.

Smart Contract System

At the core, Resolv has smart contracts for minting and redemption of USR and RLP, maintaining the collateral pools, and distributing yield. These contracts enforce rules like the 1:1 collateralization on mint, the 110% collateral ratio requirement for RLP withdrawals, and the daily profit distribution mechanism. The mint/redeem contract will only allow RLP redemption if post-redemption collateralization stays at or above 110%. Additionally, the contracts restrict withdrawals of collateral by anyone except via the designated user redemption functions, ensuring that even administrators cannot arbitrarily pull funds aside from programmed margin transfers to custodians which are rule-based.

The protocol enforces that withdrawals from on-chain treasury are limited to amounts necessary to meet margin requirements, preventing misuse of funds. These rule-based safeguards are essentially programmatic contracts taking the role of what in a traditional fund might be legal covenants or oversight by a trustee. They hard-code certain risk limits such as no unlimited draining of assets to exchanges, no redemption that breaks collateralization, contributing to Resolv’s trust-minimized design philosophy.

Multi-Chain Deployment

Resolv has deployed across nine blockchain networks including Ethereum (primary), Base, BNB Chain, Berachain, HyperEVM, Soneium, TAC, Arbitrum, and Plasma. The core Ethereum contract addresses are publicly verifiable:

Contract

Ethereum Address

USR Token: 0x66a1e37c9b0eaddca17d3662d6c05f4decf3e110

RLP Token: 0x4956b52aE2fF65D74CA2d61207523288e4528f96

stUSR Token: 0x6c8984bc7DBBeDAf4F6b2FD766f16eBB7d10AAb4

wstUSR Token: 0x1202F5C7b4B9E47a1A484E8B270be34dbbC75055

RESOLV Token: 0x259338656198eC7A76c729514D3CB45Dfbf768A1

USR Requests Manager: 0xAC85eF29192487E0a109b7f9E40C267a9ea95f2e

Custodial and Off-Chain Agreements

Despite being DeFi-native, Resolv interfaces with CeFi via custodians (Fireblocks, Ceffu) that hold and manage exchange accounts. There are contractual arrangements between Resolv Digital Assets Ltd. and these custodians. Fireblocks allows Resolv to delegate collateral to Deribit and Bybit without the collateral sitting directly at the exchange. Ceffu holds an omnibus account that interfaces with Binance futures. These relationships are operationally critical and involve legal agreements ensuring the assets in custody are not commingled with direct deposits to exchanges’ (and thus, not forming exchanges’ liability base in case of their insolvency).

The custodial structure means that if something goes awry (exchange default), Resolv has a legal claim via the custodian for those assets, potentially providing better recovery odds than direct exchange custody. In essence, Resolv’s off-chain contractual structure mirrors that of an institutional trading operation using third-party custodians to manage exchange positions under specific custody terms.

2.2. Custodial Assumptions and Asset Security

Custody of assets in Resolv is bifurcated between on-chain custody (smart contracts on Ethereum) and institutional off-chain custody for exchange collateral. Each comes with distinct assumptions and risk considerations.

On-Chain Custody (Smart Contracts)

A portion of the assets (ETH, stETH, BTC as wrapped assets, stablecoins) are held in Resolv’s smart contract wallets on Ethereum. The assumptions here are that the smart contract is secure (no one can withdraw assets except via legitimate mint/redeem processes) and that the keys controlling upgrades or emergency functions are well-managed. A multisig controls certain administrative privileges. The security audits and focus on 100% on-chain collateralization indicate a priority on making this component trustless.

Users must trust the code as they would a vault. If the code has no flaws and no backdoors, their on-chain collateral is safe from misappropriation. However, one assumption is that the price oracles feeding the contract are reliable, since they determine redemption rates and when to halt RLP redemptions. If an oracle reported collateral as more valuable than reality, it could allow excess USR to be redeemed. Resolv uses robust oracles and likely conservative pricing approaches.

Off-Chain Custody

via Fireblocks: Fireblocks Off Exchange uses Multi-Party Computation (MPC) wallets where assets are held in single-purpose blockchain wallets dedicated to Resolv. These wallets enable traders to allocate and mirror assets directly to exchanges without actual transfer, meaning assets can be audited in real-time while protecting principal from hacks, bankruptcy, and fraud. Fireblocks primarily services Deribit connectivity for Resolv.

via Ceffu: Ceffu MirrorX operates through Binance partnership, providing real-time collateral pool mirroring between Ceffu custody and Binance. The system features multi-signature approval processes, HSM integration, automatic T+1 settlements, and API-driven execution. Ceffu also enables WBETH liquid staking with slashing protection coverage. Ceffu’s legal separation means that if Binance had trouble, clients using Ceffu could potentially reclaim assets outside the exchange’s bankruptcy estate.

Off-Exchange Settlement (OES) Architecture

The technical OES architecture uses a 2-out-of-3 signer model (Custodian, Client, Trusted Third Party) for multi-party wallets. When Resolv deposits assets, the custodian locks funds while the exchange mirrors those funds as tradeable margin. Assets never actually leave custody during trading. PnL settles periodically through a separate settlement wallet. This fundamentally changes how counterparty risk is managed compared to direct exchange deposit.

Custodial Risk Management Summary: Resolv’s strategy to mitigate custodial risk is segregation and limitation: keep most value on-chain (no custody risk besides Ethereum itself and chosen DeFi protocols); for off-chain needs, use reputable custody solutions to avoid direct exchange custody; diversify across venues to avoid concentration; and programmatically prevent misuse of funds via contract rules. These measures align with best practices and show a thoughtful approach, assuming trust in some intermediaries but reducing the need to trust any single one excessively.

Specific custody wallet addresses are not publicly disclosed, though the protocol has real-time auditability with third-party verification available through Apostro’s proof-of-reserves dashboard. The absence of published custody addresses presents a transparency limitation for independent verification.

2.3. Rebalancing Mechanisms

Resolv must continuously rebalance its portfolio to maintain the peg, manage leverage, and optimize yield. The collateral pool is dynamically managed between its sub-components (ETH, BTC, stable assets) to meet protocol needs.

Margin Management Parameters

The protocol maintains a target margin ratio of 30% with a minimum threshold of 20%. This buffer absorbs potential losses from slippage, market swings, or rebalancing delays. Position adjustment triggers include: every user mint or burn triggers futures position adjustment to maintain delta neutrality; price movements require margin top-ups (when price rises) or gain realization (when price falls); and margin ratio breaching minimum threshold triggers automatic rebalancing.

Inventory Allocation on Deposits

When new collateral comes in (mint), the protocol allocates a target fraction to staking versus margin. This split is not fixed; it depends on factors like current funding rates, collateral composition, and the target exposure metric (~8%) for exchanges. If significant USR is minted via ETH deposit, Resolv increases the short futures accordingly and stakes the rest. If USR is minted via USDC deposit, Resolv may convert some to ETH/BTC to maintain the desired inventory or deploy stablecoin into lending markets.

Price Movement Response

When collateral value shifts due to price moves, delta-neutral positioning means net USD value stays constant, but the margin dynamics change. If ETH price doubles, the short futures will have unrealized loss equal to the spot gain, requiring margin top-up. Resolv rebalances by withdrawing margin and possibly converting some ETH to stablecoins or vice versa to keep ratios consistent. This ensures the exposure metric (assets at risk on exchanges) stays at target, effectively capping how much can accumulate on exchanges through partial closes of futures when needed.

Periodic Position Rollover

Although perpetuals don’t expire, Resolv periodically rolls or rotates positions to avoid excessive unrealized PnL buildup. The protocol reopens futures at new market levels to realize gains. This suggests an operational cadence (perhaps daily or weekly) where they close winning positions and open new ones, representing a form of rebalancing the hedge to keep it efficient and to withdraw profits to on-chain custody.

Automated vs Professional Management

The system operates with a mix of automated and professionally managed components:

Table: Breakdown of automated versus professionally managed operational components.

2.4. Oracle and Accounting Dependencies

Resolv’s functioning depends on accurate data feeds and accounting of assets, both on-chain and off-chain. The protocol employs four oracle providers for collateral valuation, creating defensive redundancy with Chronicle, Pyth, Chainlink, and Redstone.

Market vs Fundamental Oracles

The protocol distinguishes between market oracles (tracking real-time secondary market prices) and fundamental oracles (tracking intrinsic NAV based on actual reserves).

Fundamental values update every 24 hours based on: on-chain assets including ETH, staked ETH, BTC, and stablecoins; and off-chain positions including margin held at custodians plus unrealized P&L from futures.

Native Resolv Oracles

Native Resolv oracles (0x7f45180d6fFd0435D8dD695fd01320E6999c261c and AggregatorV3 interface at 0xf9C7c25FE58AAA494EE7ff1f6Cf0b70d7C7ce88c) provide Chainlink-compatible interfaces for integration reliability.

Price Oracle Functions

The protocol uses price oracles for valuing collateral and USR to maintain the $1 peg and determine how much collateral to give on redemption. For collateralization checks, the 110% RLP redemption rule and general monitoring of USR backing require knowing the current collateral ratio. This means summing the on-chain assets’ USD value and comparing to USR supply, using oracle prices. Extreme oracle delays could theoretically allow an RLP redemption that shouldn’t be allowed, though Chainlink updates frequently for large moves.

Funding Rate Data and PnL Accounting

A unique dependency is obtaining PnL from exchanges. The smart contract itself does not know how much funding was earned on Binance in the last epoch since that data is off-chain. An off-chain agent (like a script run by Resolv Labs or an oracle service) calculates the total change in collateral value (including realized funding, staking rewards, etc.) over the epoch and then calls the contract’s distribution function with that number. The contract may require a signed report of profit/loss, which triggers the minting of stUSR rewards and updates RLP price.

2.5. Withdrawal Surfaces

Withdrawal surfaces encompass how users withdraw or exit their positions and what risks or frictions accompany those methods. For Resolv, the primary withdrawal surfaces are the redemption process for USR and RLP, and secondarily any secondary markets or third-party integrations providing liquidity or exit.

USR Redemption Process: Users withdraw USR by redeeming it 1:1 for underlying collateral. The timeline is within 24 hours, with independent analysis by Chaos Labs in 2025 confirming the operational efficiency of USR redemptions showing a weighted average execution time of 1.8 hours, with 50% completed within 1 hour and 75% within 2 hours. Notably, redemption size shows no correlation with execution delay, where large redemptions ($1M+) process at comparable speeds to small ones. Redemption assets are in USDC or USDT only. The rate is 1:1 equivalent to the market price of USDT or USDC based on the composite oracle at that time. For example, when USDT = 0.999 USD, 1 USR is redeemable for 1 USD = 1/ 0.999 = 1.001 USDT. USR redemption is unrestricted at any time. The 24-hour window allows position unwinding, liquidity buffer management, and exchange margin settlement.

RLP Redemption Process: RLP is withdrawn by burning RLP for underlying excess collateral. The timeline is within 24 hours, with the rate being 1:1 based on current RLP price (which fluctuates). The critical restriction is that RLP redemption can only execute when USR collateralization ratio exceeds 110%. If CR drops below 110%, RLP redemptions suspend entirely. During suspension, secondary market trading (Curve, Aerodrome, Uniswap) remains available but potentially at a discount to NAV.

The 110% Circuit Breaker: This circuit breaker proved functional in late 2024 when the Collateral Asset Ratio dropped from 170% to approximately 120% during market stress. The system self-balanced: RLP yields spiked, attracting new capital without impacting USR peg stability. This demonstrates the intended functioning of the tranche structure under stress.

Secondary Market Exits: Users don’t have to go through official redemption. They could swap USR for USDC on a DEX or sell it on an exchange, and similarly sell RLP if a buyer exists. For USR, the presence of the primary arbitrage mechanism (mint/redeem at $1) typically keeps secondary market spreads tight around the peg. For RLP, if redemptions are locked (CR <110%), the only exit is secondary selling, potentially at a discount. This is reminiscent of closed-end funds trading at discount if direct redemption is unavailable.

Withdrawal via Vaults or Integrations: Resolv’s architecture includes Vaults (professionally managed strategies built on top of USR/RLP). If users enter via a Vault, their exit might be through that vault’s interface rather than directly redeeming USR. These layered integrations mean some users might not even know they indirectly hold USR. It’s important operationally because those integrators need confidence in Resolv’s liquidity. If Resolv halted redemptions, those vaults would in turn halt.

Instant Protocol Redemption: Resolv also offers instant USR redemptions with a 24-hour cap and a small fee. Both the redemption cap and fee are adjustable based on current TVL and market conditions. At the time of writing, the daily cap is $1M with a 1 bps fee. These instant redemptions are supported either by idle USDC held in the Treasury or by temporarily borrowing funds via Aave, subject to a predefined health factor (HF) parameter within the Treasury smart contract.

2.6. Governance Rights and Protocol Controls

Governance in Resolv is primarily exercised through the RESOLV governance token and the protocol’s smart contract parameters. Understanding the scope of these rights and controls is important, as it influences how the system can evolve or respond to situations.

RESOLV Token Utility: The governance token ($RESOLV) has a fixed supply of 1 billion tokens and serves as the voice of the community in protocol decisions. Holders can vote on proposals that alter key aspects of Resolv including:

Adjusting yield allocation percentages (Base vs Risk vs Fee)

Changing the collateral whitelist (adding support for new collateral types, exchanges, or yield strategies)

Setting risk parameters like the minimum collateralization (110% rule)

Fee levels (currently 10% protocol fee)

Use of the protocol treasury

Launching new products or incentivizing integrations.

The token distribution is:

40.9%: Ecosystem & Community (24-month vesting)

26.7%: Team & Contributors (1-year cliff + 30-month vesting)

22.4%: Investors (1-year cliff + 24-month vesting)

10.0%: Season 1 Airdrop

Staked RESOLV (stRESOLV): Only stRESOLV holders vote through Snapshot (resolvgovernance.eth), with a two-layer process, a Discord forum discussion followed by gasless off-chain voting. Staking features a 14-day unstake cooldown and time-weighted multiplier reaching 2x for 1-year average holding periods. Staking RESOLV grants a share of protocol fees plus voting weight, incentivizing long-term holding.

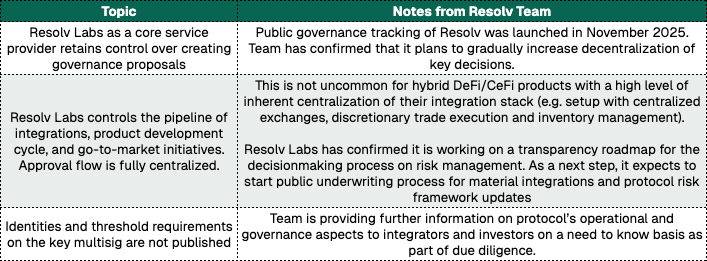

Current Governance Model: The current model is hybrid, team-led with transition roadmap toward full DAO control. Governance launched November 2025 with limited decentralization. RGP-01, the first governance proposal, approved distribution of 120,000 ETHFI earned from weETH exposure over 3 months to stRESOLV holders.

After consulting with the Resolv team on some points and raising some concerns with centralization and operational concerns, they have set forth some expectations.

Legal Structure

From a legal perspective, Resolv Digital Assets Ltd. is the main entity and structured in BVI. Resolv Foundation (Cayman) is the parent and UBO. Resolv Labs Ltd (BVI) is a key vendor of Resolv Digital Assets Ltd., carrying out software development assignments and marketing/business development services. To work with protocol directly, users should undergo AML process (KYC/KYB + wallet screening) Resolv Digital Assets Ltd. (BVI) is the sole protocol entity

2.7. Identified Failure Modes and Risk Mitigants

This section enumerates the major failure modes that have been identified in Resolv’s design, along with how the protocol mitigates them. This serves as a summary risk checklist for operational due diligence.

Counterparty Exchange Failure

An exchange used for hedging (e.g. Binance, Deribit) defaults or locks up funds.

Consequence: Loss of margin and unrealized gains on that venue; potential under-collateralization.

Mitigants: Use of off-exchange custody (assets held via Fireblocks/Ceffu, not commingled); diversification across multiple venues to limit exposure; and RLP capital to absorb losses. RLP effectively serves as an insurance pool covering the credit risk of exchanges. Additionally, active management withdraws profits frequently to minimize what’s left on exchange at any time. If a failure occurs, RLP redemption halts if needed, and USR remains redeemable from on-chain assets.

Market Risk (Hedge Imperfection)

This includes scenarios like sustained negative funding rates or extreme volatility leading to liquidation.

Consequence: Strategy could incur losses, possibly significant if positions liquidate.

Mitigants: Highly liquid venues and conservative leverage are used to reduce chances of liquidation. Because Resolv is delta-neutral and not outright leveraged (except the inherent leverage in RLP acting as equity), the only way it gets liquidated is if the team fails to post margin. They mitigate this by maintaining buffer collateral and dynamic margin management. Negative funding is explicitly addressed: RLP covers any funding losses. Historical extreme 8-hour funding rates (-0.35% Binance, -0.6% Deribit) would require 60-90 days of extreme negative rates to drain the protection layer.

Liquidity Risk (Runs and Large Withdrawals)

A flood of withdrawals, especially from RLP, could destabilize the system.

Consequence: If RLP could all exit at once during stress, USR might become undercollateralized.

Mitigants: Withdrawal gating for RLP at 110% CR ensures RLP can’t fully drain if it’s protecting USR. The system is designed to be overcollateralized normally, so moderate withdrawals are fine. For USR, a run is mitigated by having largely liquid on-chain assets and the ability to borrow against staked assets to meet redemptions promptly. Open-market arbitrage helps by other parties stepping in to buy cheap USR if any panic-sell occurs, then redeeming it.

Smart Contract Exploit

A bug in contracts could allow theft or unintended behavior.

Consequence: Loss of funds, loss of confidence, possibly collapse of the stablecoin if severe.

Mitigants: Audits (14+ engagements from five firms), bug bounty programs ($500,000 maximum on Immunefi), time-locked governance for upgrades to allow scrutiny, and circuit-breakers (pausing contracts) if something odd is detected. Many DeFi protocols have an emergency pause function controlled by a multisig; Resolv has this for the initial phase. That’s a mitigant: if an exploit starts, they can pause minting/redemptions to stop the bleeding and then patch.

Oracle Failure/Manipulation

If price feeds or other oracle inputs are wrong, it could enable bad redemptions or mispricing.

Consequence: Could drain collateral if price feed says ETH is significantly different from market reality.

Mitigants: Use of established oracles (Chainlink, Chronicle, Pyth, Redstone) which have decentralization and anti-manipulation measures. The system might also verify multiple sources. Resolv might set limits, such as not honoring redemptions beyond certain daily size or price slippage without manual intervention. RLP indirectly protects USR; if an oracle glitch caused slight loss, RLP would eat it.

Governance Attack or Failure

A malicious proposal could alter the protocol in harmful ways.

Consequence: Loss of funds or collapse of trust.

Mitigants: Time-locks and multi-stage governance, with proposals on-chain for days giving users time to exit if concerning. Admin multisig could potentially veto clearly malicious proposals. Distribution of tokens matters; if team and core supporters hold a majority, hostile takeover is unlikely. Quorum thresholds and security councils provide additional protection.

Operational Mismanagement

Non-technical issues such as team failing to respond to margin call due to human error or system downtime.

Consequence: Avoidable losses or panic.

Mitigants: Professional operations with presumably 24/7 monitoring, multiple team members on call, automated alerts. Multiple exchanges are used, so even if one margin got low, others might cover net exposure. This is more an internal risk mitigated by having a solid team and gradually handing off simple tasks to trustless agents.

Conclusion

Resolv Protocol presents a thoughtfully designed delta-neutral stablecoin with a clear economic structure. The separation of USR and RLP tranches ensures conservative holders receive stability while risk-tolerant participants earn enhanced returns in exchange for absorbing losses. The protocol benefits from diversified yield sources, and the tranche structure has already proven functional under real market stress. Operationally, Resolv demonstrates institutional rigor through third-party custody, multi-oracle redundancy, and programmatic safeguards. Resolv has operated without incident to date and has demonstrated self-correcting behavior under adverse conditions.

Download the Full Analysis

This report is available as a PDF for offline reading and sharing.