Economic analysis of stETH in ETFs

Economic analysis of the use of stETH in the context of an ETF or exchange traded product

PDF | ePub

Disclaimer

The information contained in this analysis is provided for general informational purposes only and is not intended to be, and should not be relied upon as, legal, financial, or professional advice. Steakhouse Financial assumes no liability or responsibility for any errors or omissions in the content of this assessment or for any actions taken based on the information provided herein.

This analysis is based on the information available at the time of its preparation and is subject to change without notice. The assessment is not a guarantee of future performance or results, and past performance is not necessarily indicative of future results.

You should seek professional advice from a qualified attorney or financial advisor before making any decisions or taking any actions based on the information contained in this assessment. Steakhouse Financial disclaims all liability and responsibility for any actions taken or not taken in reliance on the information contained in this analysis

Steakhouse Financial Limited is a boutique consulting company that serves as the finance workstream lead appointed by Lido DAO token holders. Please make reference to this and further disclaimers on our website

Introduction and motivation

The emerging inflow of capital into Ethereum-based ETFs opens a new chapter in expanding accessibility to digital assets for retail and institutional investors. More than eight have already come into ETFs in the US, without counting non-US exchange-traded products (ETPs) that have begun the trend some years ago.

On the whole, it is important to stress that blockchain validation is a sui-generis activity that does not map to financial market instruments. We take the view that these applications more closely resemble commodities, akin to internet cables, including stETH middleware. The participants involved in running validation software, including participants that use stETH middleware, are essential to allow the consensus algorithm to run. These participants perform functions akin to IT infrastructure or network providers, in the role of allocating public goods necessary for communications.

Inflows of Ether into blockchain validation activities democratize access to this process, but also bring the risk of concentrating Ethereum validation within single node operators and compromising its viability as neutral communications infrastructure. As more users begin to seek exposure to Ethereum staking rewards that incentivize participating in the consensus algorithm, the risk of losing Ethereum’s autonomy is in play. Without autonomy, Ethereum ceases to have value as a blockchain capable of supporting economic activity.

Steakhouse Financial has been contributing to Lido DAO since 2022, and, based on the findings of our analysis, we argue that the use of stETH has a measurable and positive impact on the decentralization of Ethereum validation. A simple analysis of validator concentration as sieved through stETH shows that the Herfindahl-Hirschman Index (HHI) of market concentration is significantly lower with Lido middleware distributing ETH to validators relative to without. To cite Coinbase’s “Order Instituting Proceedings to Determine Whether to Approve or Disapprove a Proposed Rule Change to List and Trade Shares of the Grayscale Ethereum Trust under NYSE Arca Rule 8.201E Commodity-Based Trust Shares) File No. SRNYSEArca-202370 Release No. 3499428” (link):

“The technological and operational security mechanisms inherent in Ethereum's blockchain significantly limit ETH’s susceptibility to fraud and manipulation.”

We wholeheartedly agree with this perspective, and propose that the use of stETH as neutral staking middleware furthers these security mechanisms inherent to the Ethereum blockchain consensus algorithm. Therefore, relying on infrastructure, such as stETH, as a stratum for building ETPs can help reinforce the robustness of the network for all participants.

With this analysis, we wanted to take the narrow view of an exchange-traded product issuer looking at the relative economics of selecting stETH as an underlying asset for an ETP. We investigated whether the use of stETH could provide robustness for ETP issuers from three different angles:

Is trading in stETH correlated with ETH commodity futures listed on the CME futures market?

High correlations would suggest that authorized participants (APs) in any ETPs could rely on deep commodity futures markets for hedging redemptions and subscriptions to stETH-based ETPs. Furthermore, it would suggest that bad actors would have limited room to perpetrate fraud or manipulation on the stETH market without it also being detectable in ETH or ETH futures markets

Is stETH able to trade without susceptibility to control by a few individuals or entities?

Deeper markets with low bid-ask spreads make it more likely to maintain a free and fair market in stETH trading

What exposure to a total return profile for Ethereum does stETH offer as an underlying asset in ETPs?

A total return profile for Ethereum that includes a broad-based approximation of the whole staking rewards market would more accurately reflect the economic functionality of the consensus algorithm

Conclusions

Is trading in stETH correlated with ETH commodity futures listed on the CME futures market?

Overall, the results of our correlation analysis provide empirical evidence strongly supporting the conclusion that stETH prices generally move in close alignment between spot ETH markets and the CME ETH futures market. We therefore take the view that fraud or manipulation that impacts stETH prices would likely similarly impact ETH prices and CME ETH futures prices. Surveillance regimes at CME and in venues that list stETH or ETH can assist in detecting any potential impact of fraudulent or manipulative acts and practices

APs would also be able to efficiently hedge subscriptions and redemptions to the vehicle and protect ETP investors

Is stETH able to trade without susceptibility to control by a few individuals or entities?

stETH markets demonstrate strong depth and narrow bid-ask spreads in line with other digital asset commodities, suggesting the market in stETH trading is fair and efficient

What exposure to a total return profile for Ethereum does stETH offer as an underlying asset in ETPs?

A total return profile for Ethereum that includes a broad-based approximation of the whole staking rewards market would more accurately reflect the economic functionality of the consensus algorithm

Trading in stETH is highly correlated with ETH futures at CME

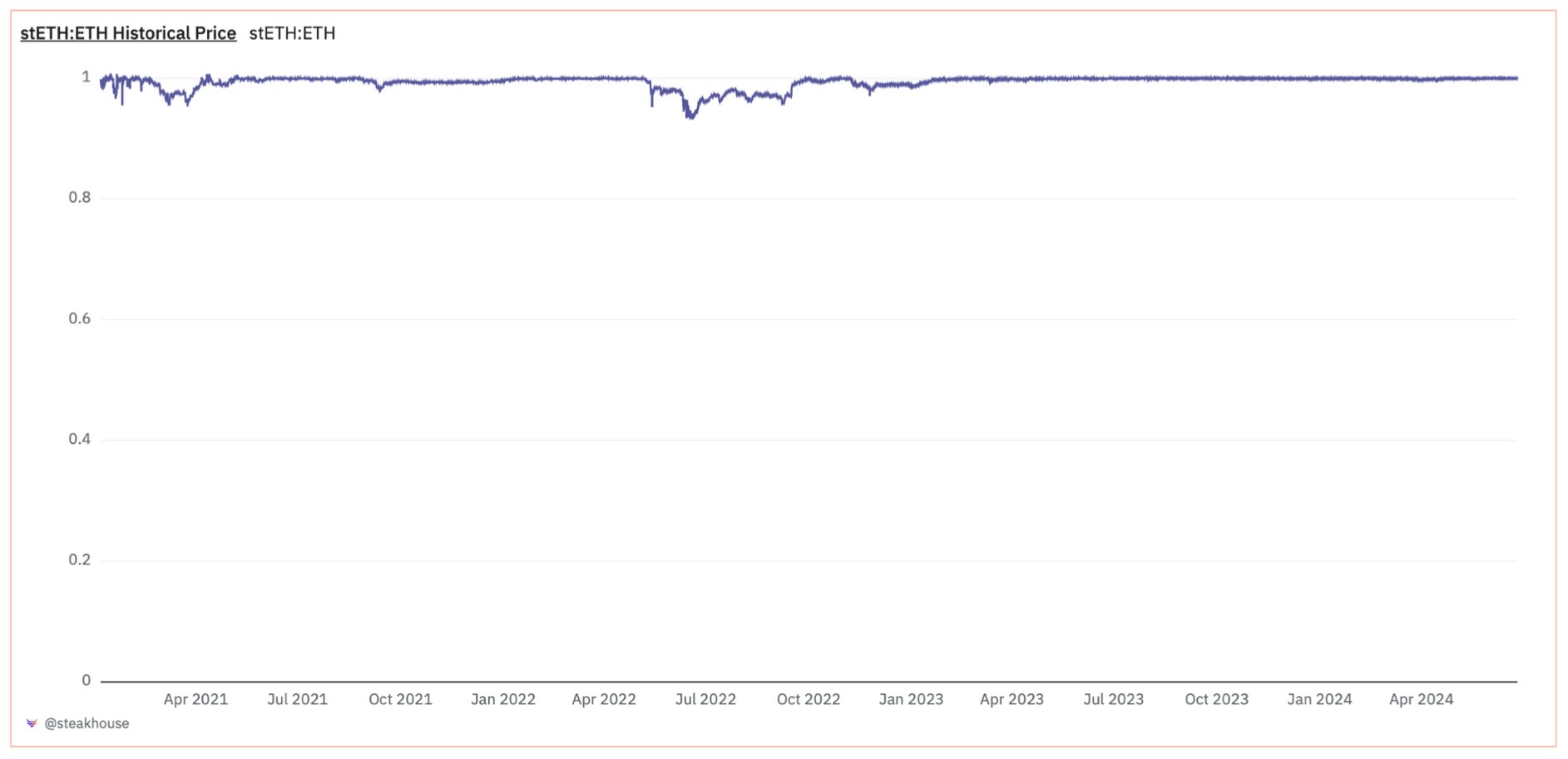

stETH trading takes place primarily over decentralized AMM pools (DEX) on the Ethereum blockchain and on centralized exchanges (CEX) such as OKX or ByBit, across different time frames. The trading patterns reflect two different regimes across time:

Prior to withdrawals being enabled from the Ethereum Consensus Layer (CL) on May 17, 2023, during Ethereum’s Proof of Work phase and in the early instances following the Shapella upgrade that began the transition of the consensus algorithm to Proof of Stake

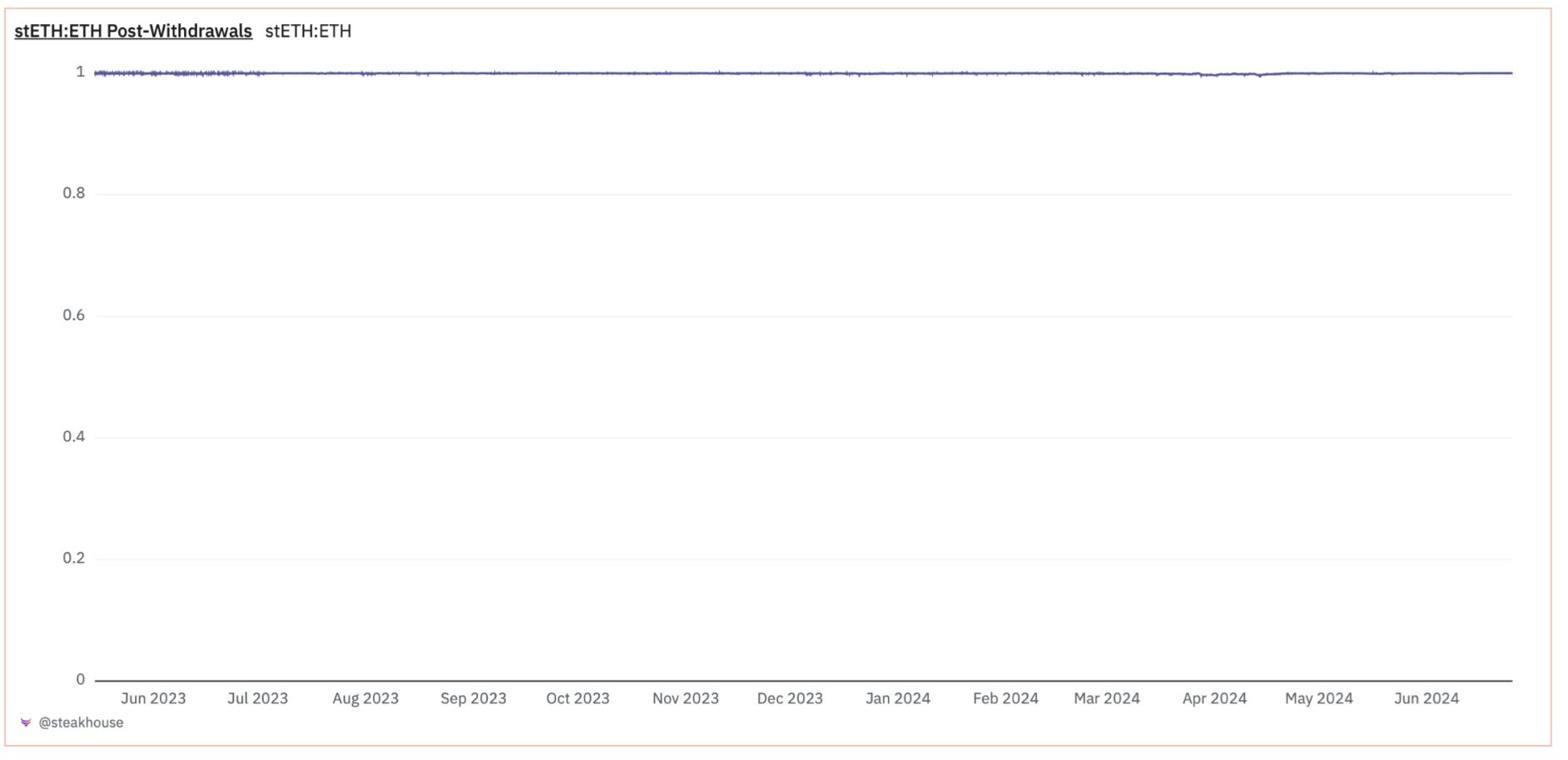

After withdrawals being enabled from the Ethereum Consensus Layer (CL), completing the transition of the consensus algorithm to Proof of Stake

The first regime in particular featured a number of instances of decoupling between the relationship of 1 stETH and 1 ETH. This is notably because Ethereum’s transition process to Proof of Stake consensus disallowed withdrawals until the transition completed with the Shapella upgrade.

Our analysis examines the correlation dynamics between ETH futures and both ETH spot prices and stETH prices across three distinct scenarios.

For stETH data, we use TradingView API data for CEX pairs of stETH/USD. For ETH commodity futures data, we rely on tick-by-tick historical data from CME. For ETH spot prices, we rely on Coinbase data sourced through TradingView APIs. Python notebooks are available on our github.

Each scenario explores different timeframes and periods to understand how correlations behave under various market conditions:

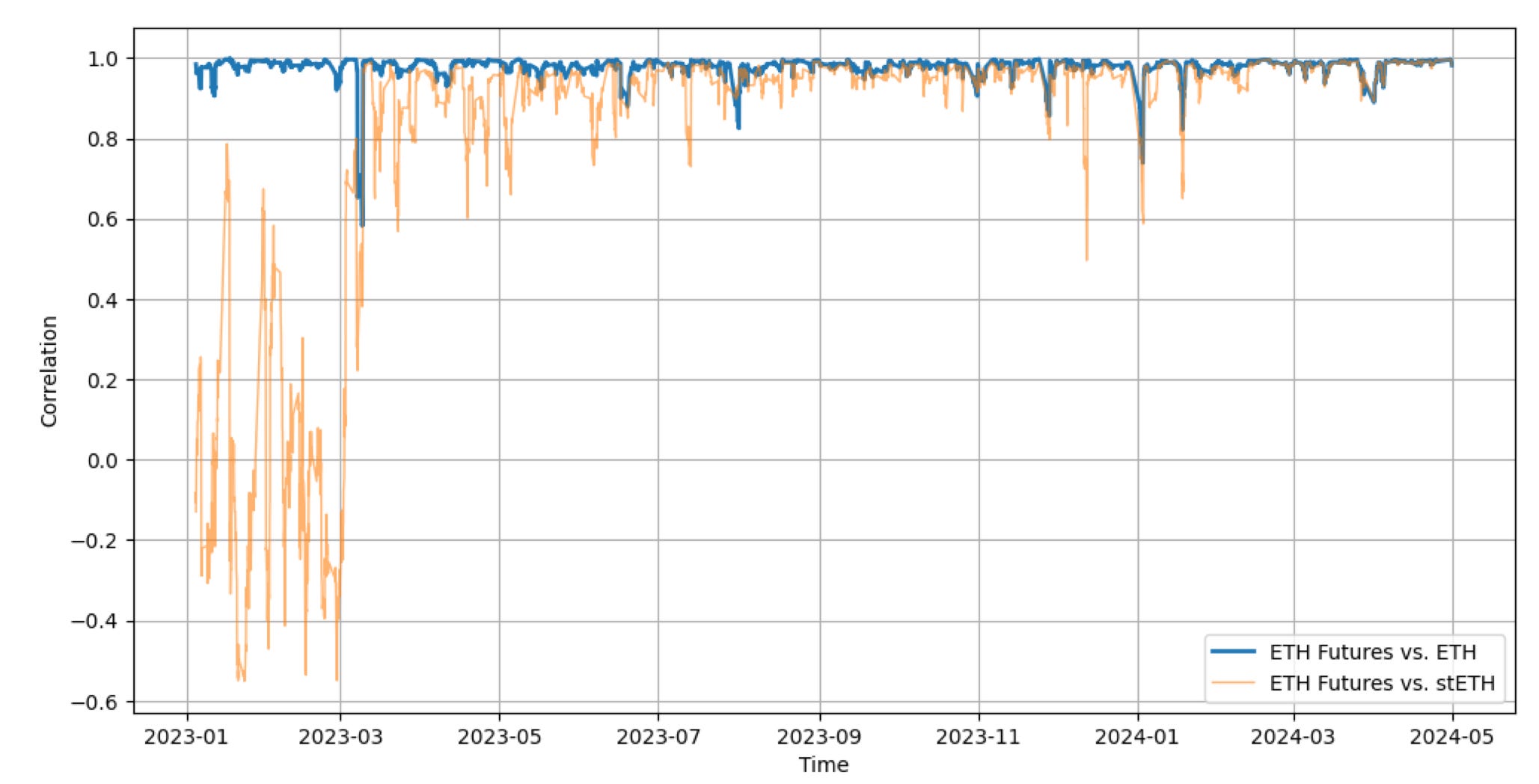

Scenario 1: Explores correlations on a 1-hour timeframe from January 1, 2023, to April 30, 2024, providing a comprehensive view over an extended period to gauge long-term correlation trends.

Scenario 2: Analyzes the 1-hour timeframe from April 30, 2023, to April 30, 2024, specifically omitting the early 2023 period noted for its lower correlation on stETH. This scenario aims to demonstrate that, excluding this initial volatility, the correlation has remained consistently high and stable.

Scenario 3: Focuses on a 5-minute timeframe from May 12, 2024, to June 12, 2024, offering insights into the immediate and granular market reactions, highlighting how quickly market dynamics are reflected in pricing correlations.

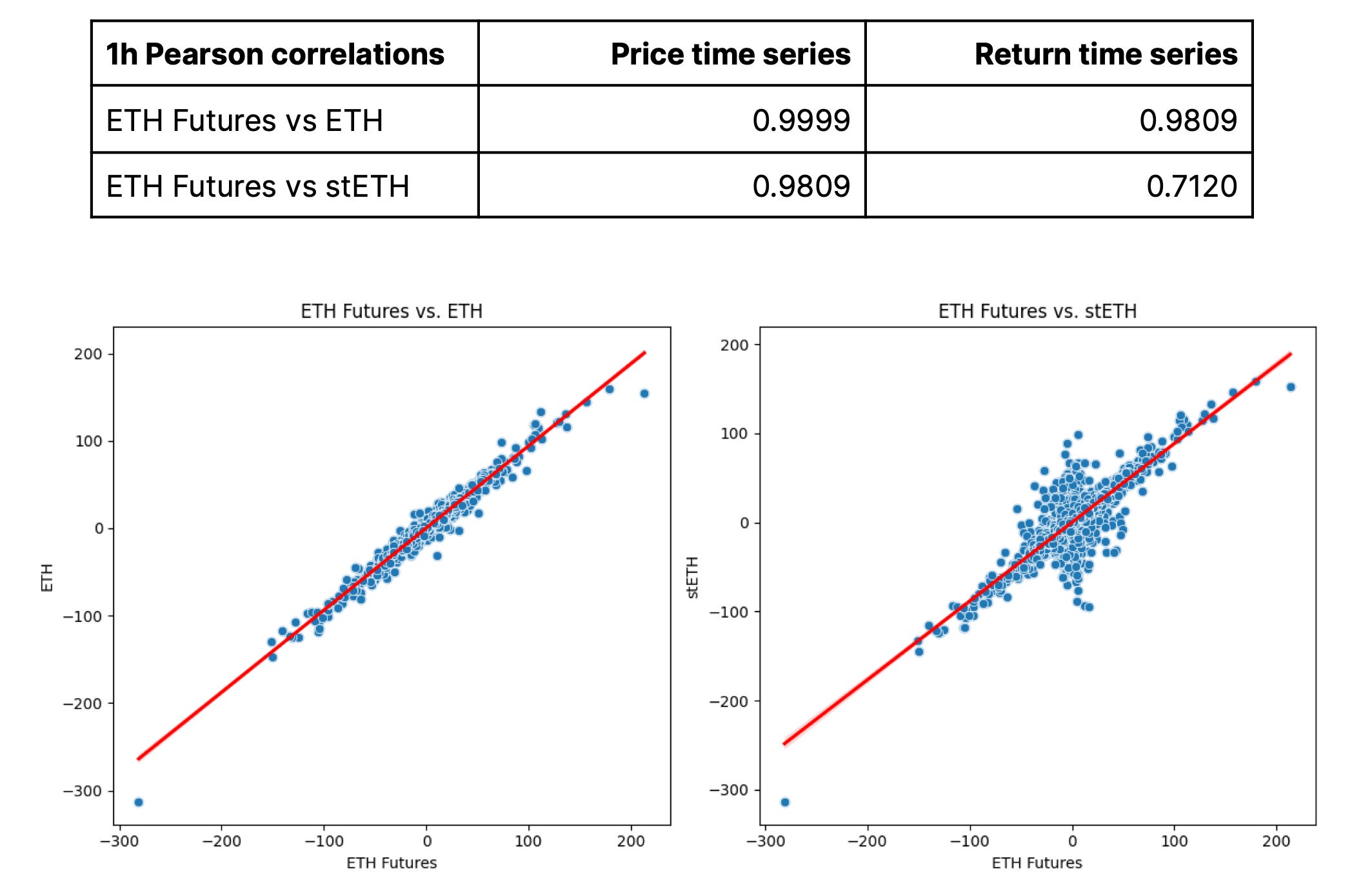

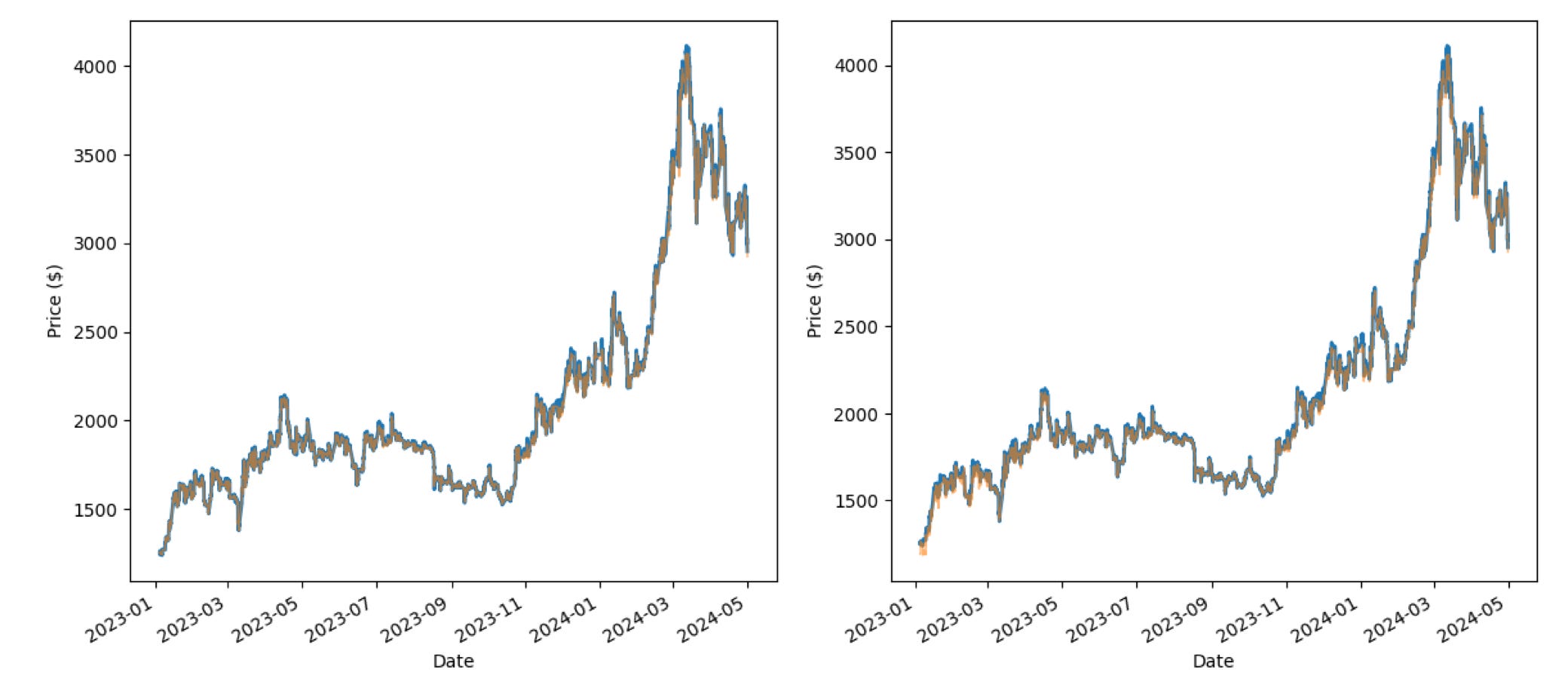

Scenario 1: January 1, 2023 to April 30, 2024 (1h ticks)

In Scenario 1, we compared 1 hr CME ETH futures from January 1, 2023, to April 30, 2024 for both ETH and stETH on prices and USD-based returns.

As Coinbase found in its File No. SRNYSEArca-202370, ETH prices listed at Coinbase track very closely to front-month ETH CME futures. What we also find is an overall alignment with stETH prices on a 1h timeframe, suggestive of a close relationship between all three commodities.

A rolling correlation analysis showcases the shift in regimes for the stETH asset, namely before and after withdrawals enabled. For stETH, this feature was enabled on May 17, 2023, which is when rolling correlations trend closer to 1.0. The relevant analysis in the current regime starts on April 30, 2023 through to the present, which is the timeframe selected for Scenario 2.

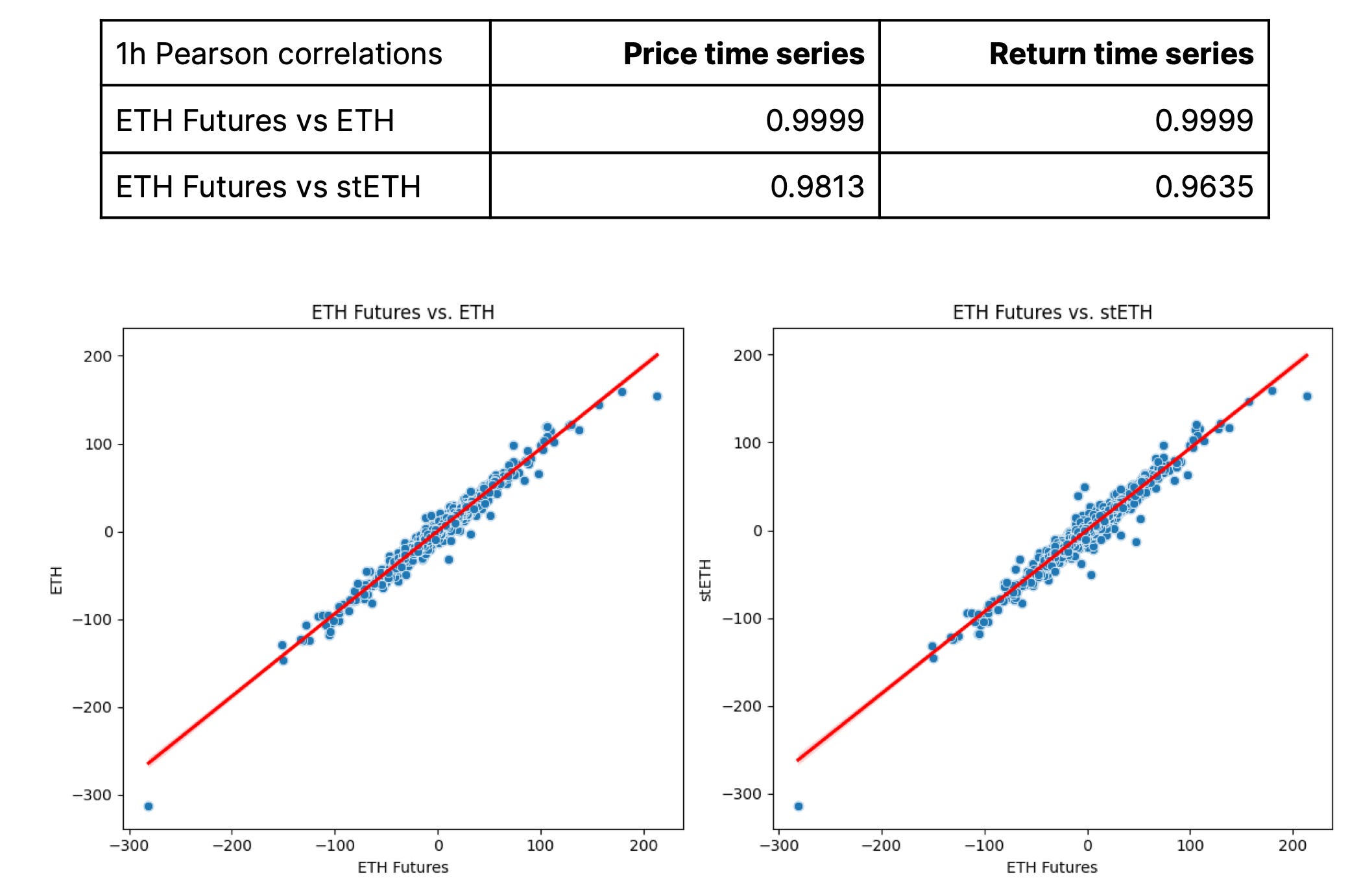

Scenario 2: April 30, 2023 to April 30, 2024 (1h ticks)

In Scenario 2, we compared 1 hr CME ETH futures from April 30, 2023, to April 30, 2024 for both ETH and stETH on prices and USD-based returns.

In this regime, the stETH vs CME Futures price shows a much tighter correlation and the correlation on returns over time is also much closer to 1. Excluding the early 2023 period in the prior regime (before withdrawals), the chart shows a highly stable and strong correlation between ETH Futures and both ETH and stETH prices, consistently above 0.9. However, occasional sharp drops in the correlation with stETH (typically related to periods of high volatility in price) suggest transient divergences in how stETH reacts to market conditions compared to ETH Futures and spot ETH.

To provide more insight into periods of higher volatility, we focused on a smaller time frame at smaller price ticks in Scenario 3.

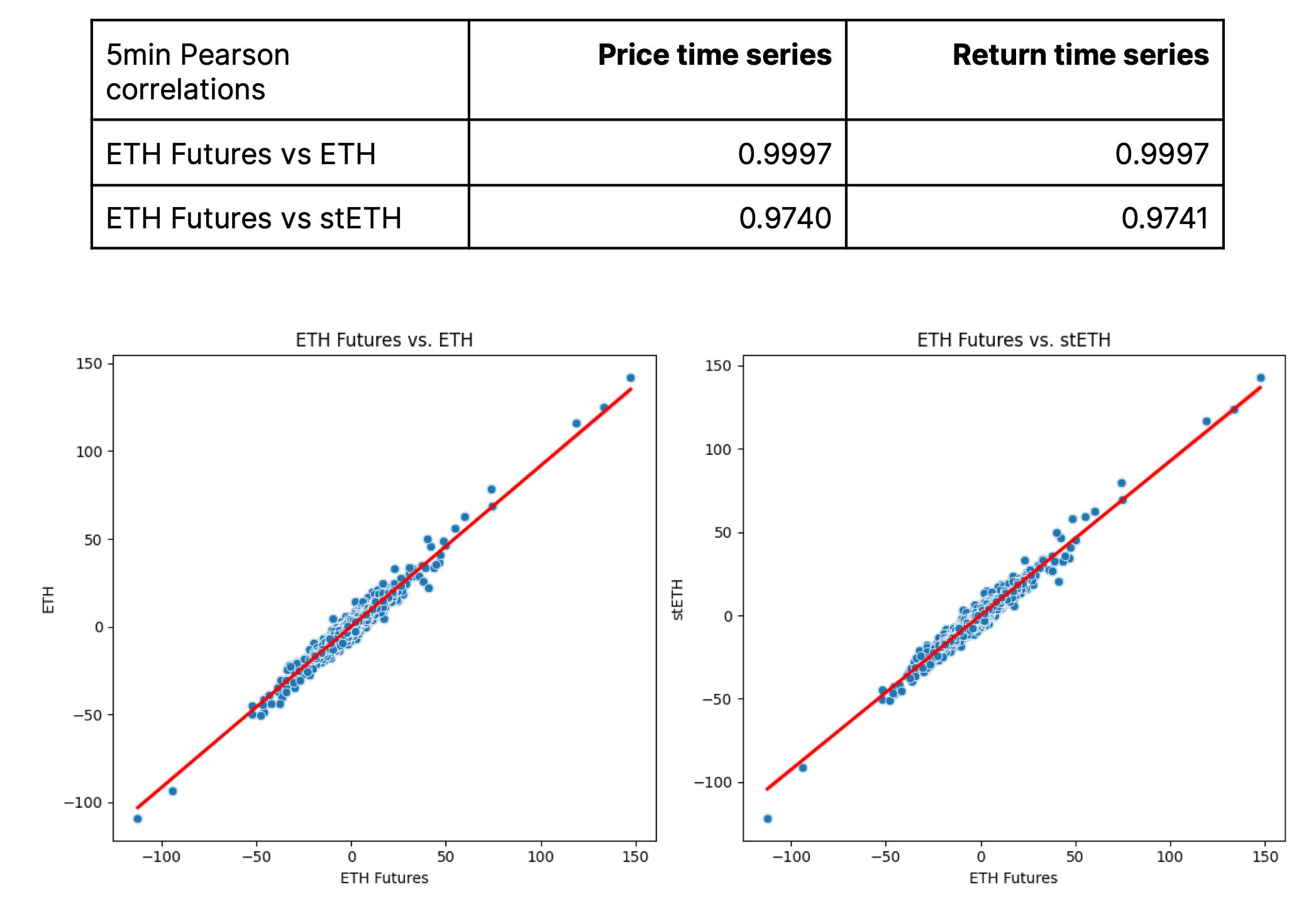

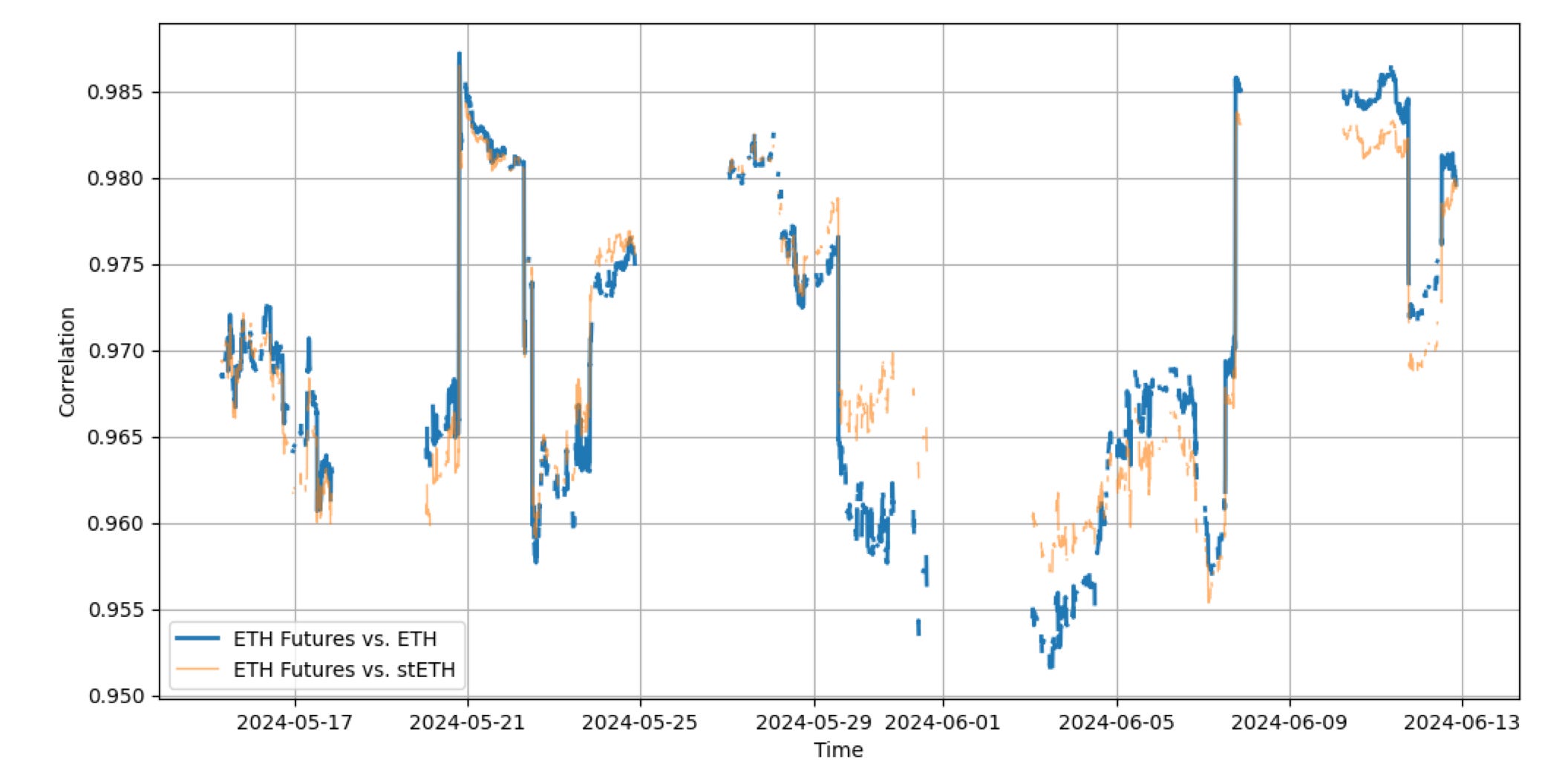

Scenario 3: May 12, 2024 to June 12, 2024 (5min ticks)

In Scenario 3, we compared 5-min tick CME ETH futures from May 12, 2024, to June 12, 2024 for both ETH and stETH on prices and USD-based returns.

Moving to a 5-minute timeframe results in a slightly lower correlation on returns, reflecting the increased data volatility at finer time scales. However, over the last month, both ETH and stETH display almost identical correlations in both price and returns.

Operating from Sunday 5:00 PM to Friday 4:00 PM CT with daily hour-long breaks at 4:00 PM and closures on US bank holidays, CME Futures show pronounced spikes in correlation charts on shorter timeframes, especially after weekends.

Conclusions

The question we sought to answer is whether trading in stETH correlated with ETH commodity futures listed on the CME futures market. The high and sustained correlations would suggest that authorized participants (APs) in any ETPs have relied on deep commodity futures markets for hedging redemptions and subscriptions to stETH-based ETPs.

Any staking exposure in ETPs must be measured in a regime where withdrawals are possible from the CL, and this includes stETH. In this regime, namely Scenario 2 and 3, there are instances where prices of stETH experienced higher deviations than 10bps relative to CME futures. The vast majority of these deviations returned to the baseline within a few hours. This evidence is consistent with an unencumbered and efficient market, with well functioning arbitrage activity. Just as with any and all assets, deviations of a longer duration may occasionally occur, but they are ultimately arbitraged away.

Overall, the results of our correlation analysis provide empirical evidence strongly supporting the conclusion that stETH prices generally move in close alignment between spot ETH markets and the CME ETH futures market. We therefore take the view that fraud or manipulation that impacts stETH prices would likely similarly impact ETH prices and CME ETH futures prices. Surveillance regimes at CME and in venues that list stETH or ETH can assist in detecting any potential impact of fraudulent or manipulative acts and practices.

stETH markets are deep, actively traded and liquid

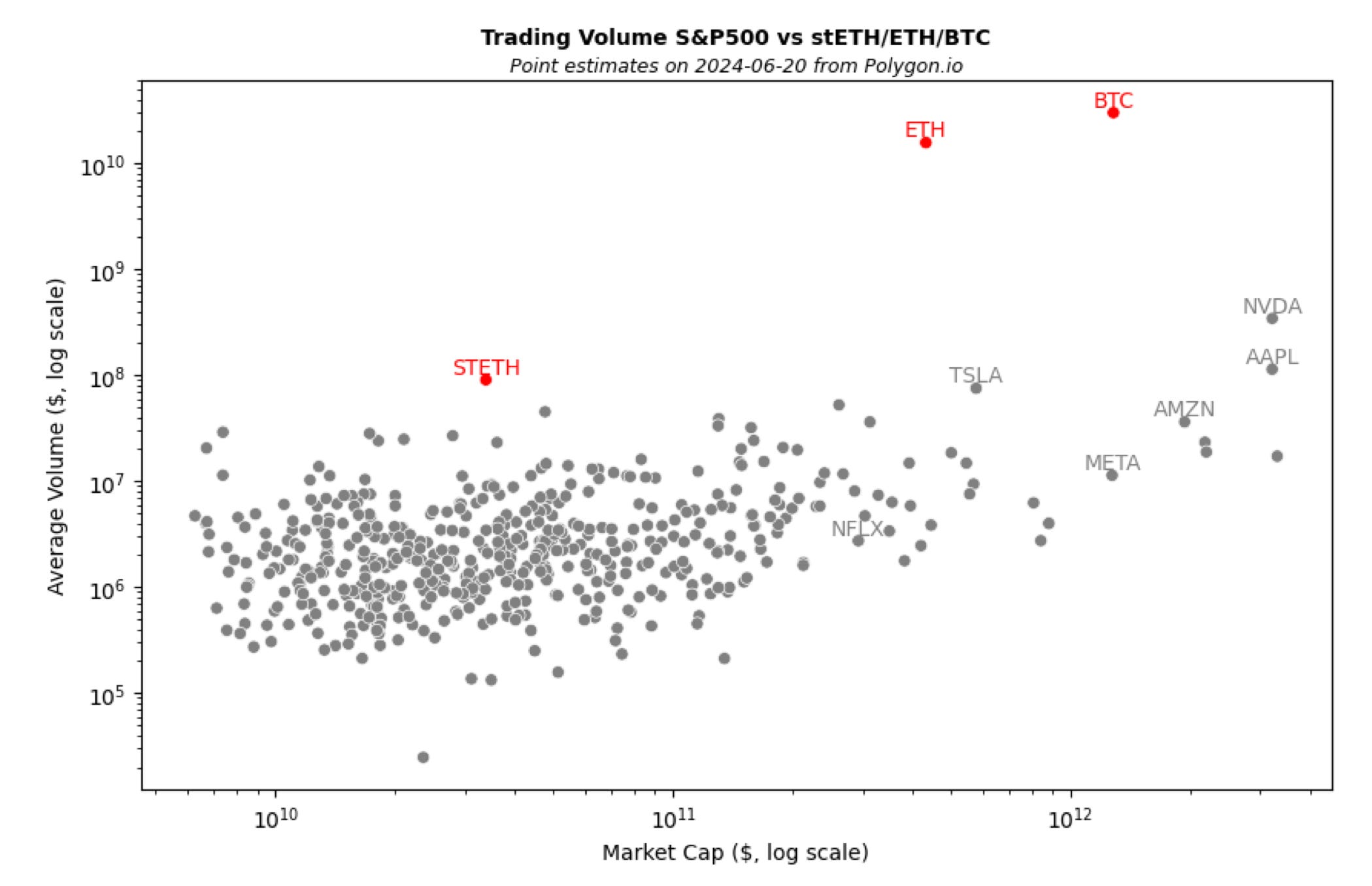

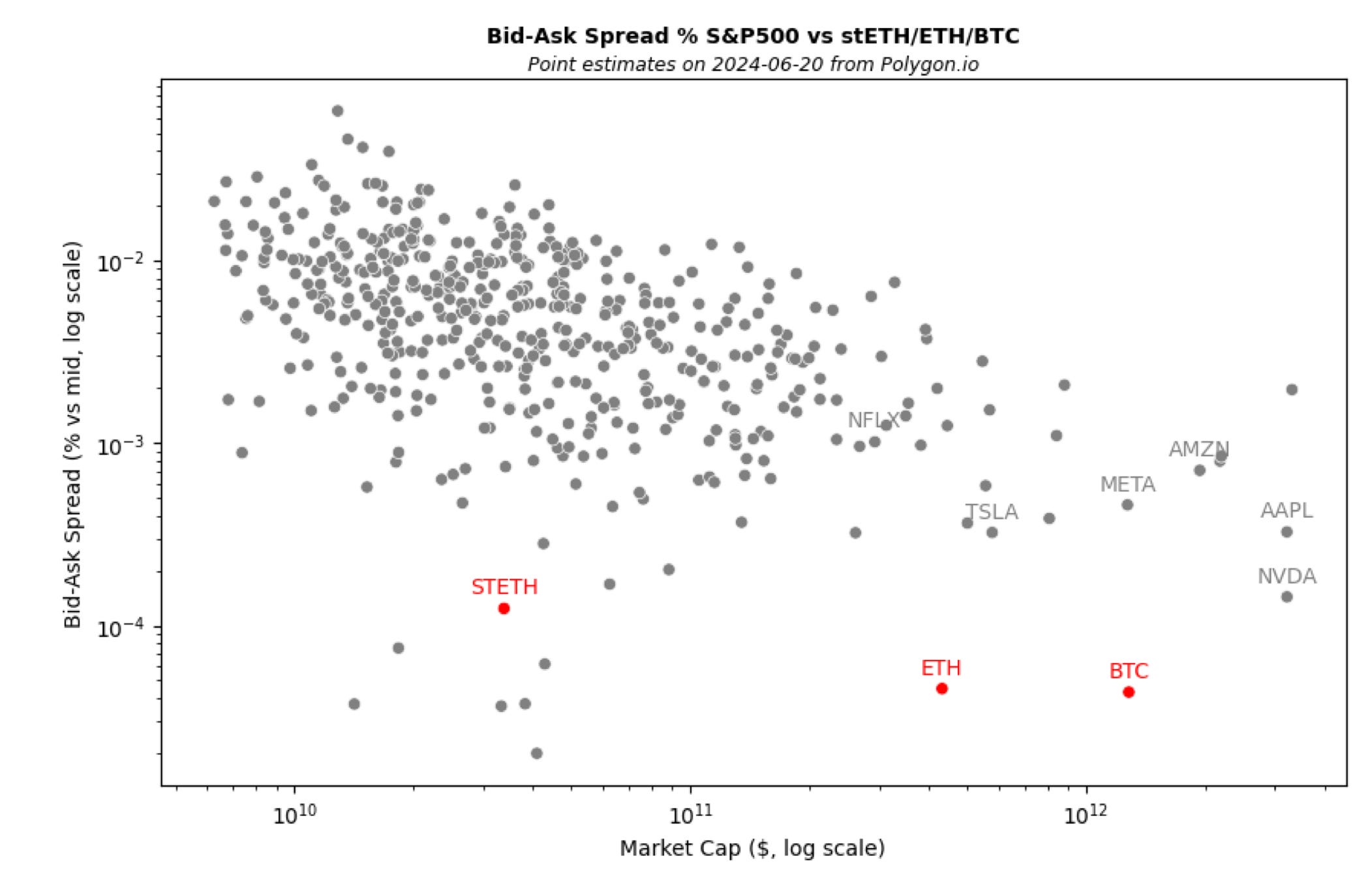

We concur with Coinbase’s view that the greater the liquidity depth, trading volume and market capitalization of a commodity, the lower the risk that it can be manipulated by a bad actor.

The ETH and stETH markets generally benefit from very significant depth and liquidity. As of June 20, 2024, the total market capitalization of ETH and stETH totaled $410B and $32B respectively. Their respective trading volumes compare very favorably to stocks that comprise the S&P 500, which benefit from a deep and liquid market in the US. We take the view that tighter spreads are indicative of a well-functioning market with higher liquidity and lower adverse selection costs. Notably, we believe that greater risks of fraud and manipulation would result in wider spreads from dealers and traders to compensate for the additional risk.

The equity and digital asset data for the above charts is sourced from Polygon.io APIs, with a point-estimate on June 20, 2024, for trading volume and bid-ask spreads. Trading volume was calculated averaging the latest 10 trading days ending June 21, 2024. Market capitalization was calculated as of June 20, 2024.

In the first graph, daily trading volume for stETH is solidly inside the S&P 500 density for its relative market cap. Notably, other crypto such as BTC and ETH are relatively high volume for their respective market caps. In the second Bid Ask spread % graph, stETH ranks on par with other digital asset, like BTC and ETH.

stETH can be used to build fairer and more accurate staking ETPs

Unlike staking products tied to 1-3 centralized counterparties for staking, stETH-based ETPs diversify the sources of staking rewards. This reduces the impact of any single validator's performance issues or failures, providing a more resilient and reliable product. This also leads to a more decentralized and stable reward.

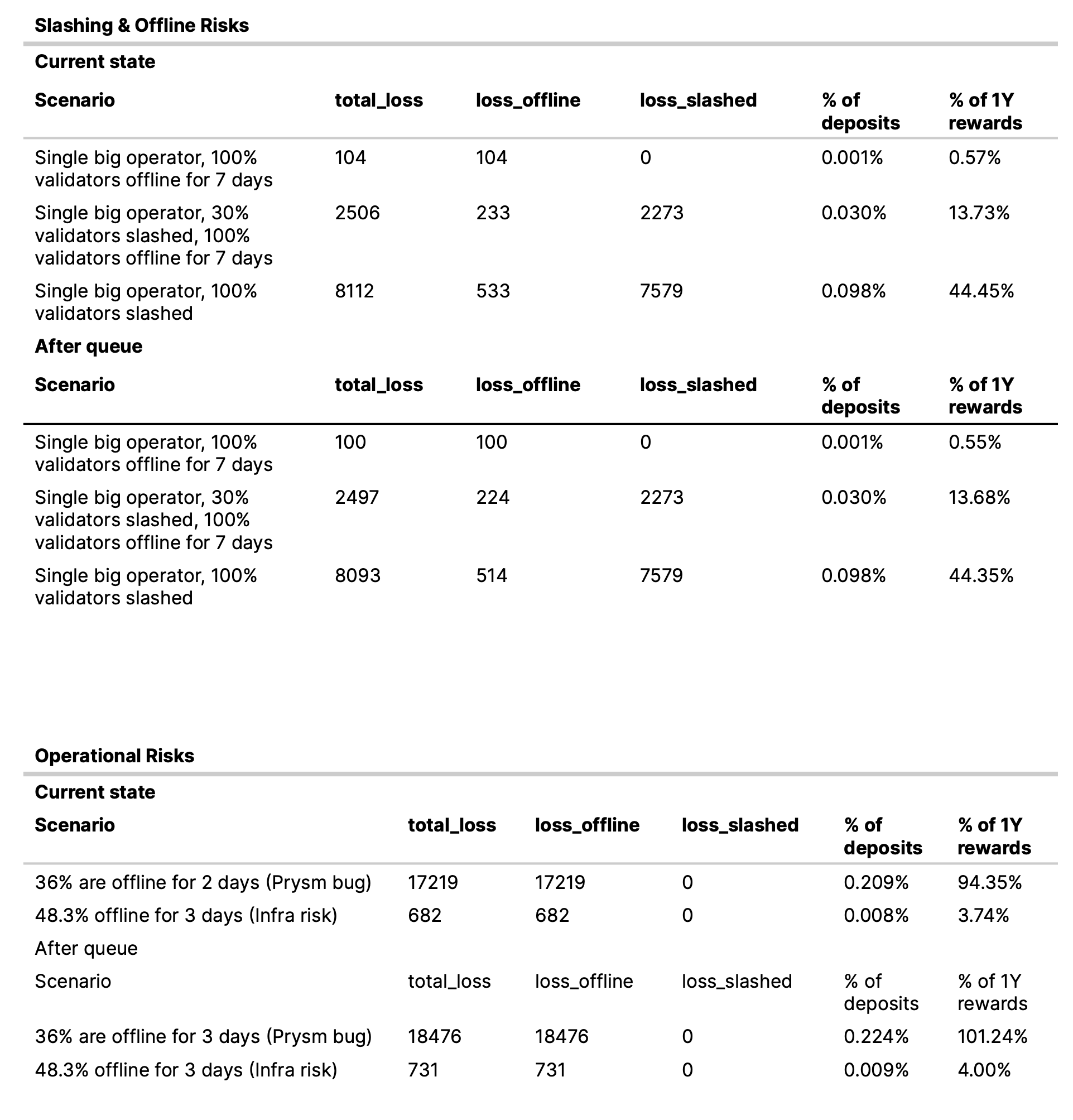

The sources of risk in staking, including stETH, largely relate to so-called slashing risks and a broader set of operational risks. We consider slashing risks as those imposed on validators attempting to subvert the consensus algorithm through malicious operations of validator software. Generally, these types of operations are costly for the perpetrator and on the whole quite unlikely overall. The other source involves operational mismanagement from the node operator side, and relates to non-malicious operations that nevertheless incur a penalty for not following the consensus algorithm as programmed.

Lido DAO contributors evaluated the different sources of risk and estimated, for a point in time in September 2023, what the extent of different scenarios of risk could be. Although slashing and offline risks represent a larger loss given slashing, in practice, they are far less likely than operational risks.

Slashing insurance is one way that node operators aim to mitigate the impact of these risks. However, to date, no major slashing or operational risk event has taken place within professional node operators, suggesting there is no track record as to the effectiveness of slashing insurance to meaningfully mitigate the impact of such risks occurring.

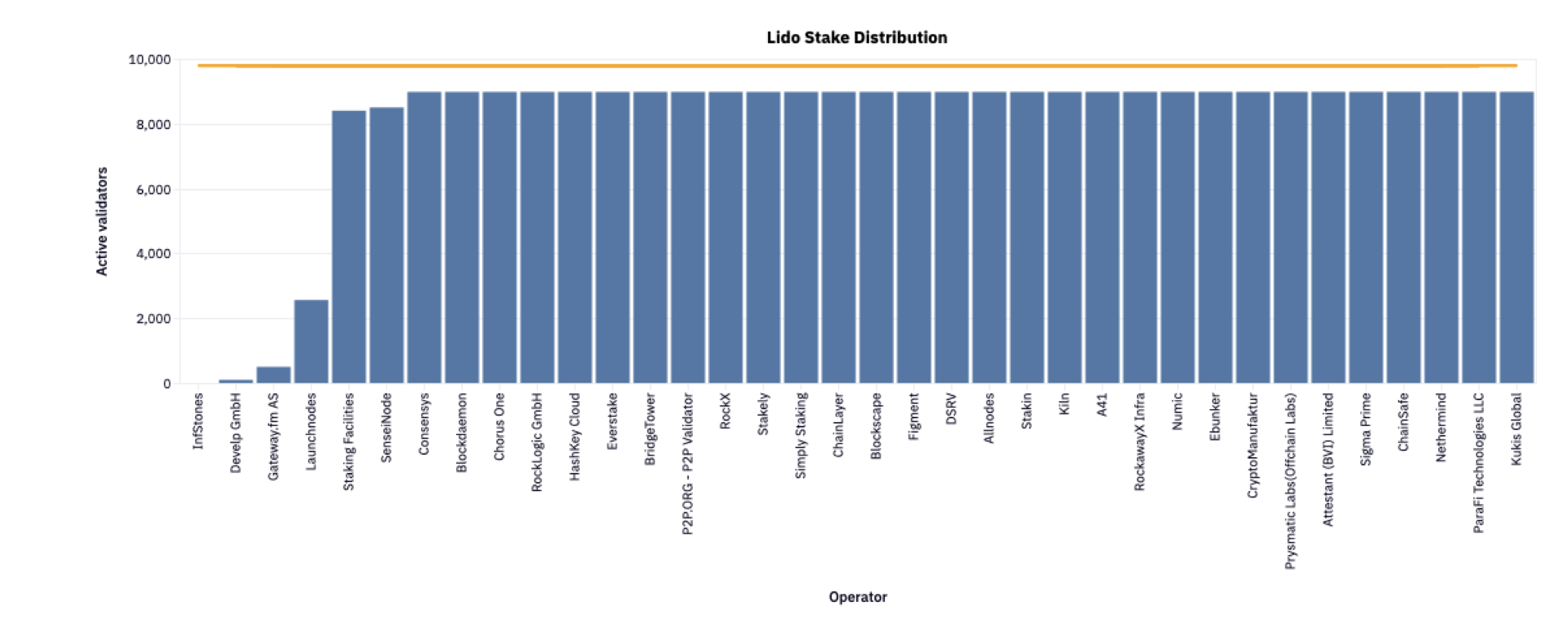

A more robust market-based solution is to offer diversified exposure to many different node operators - certainly more than just 2-3. The rationale is that operational risk is far more likely to be correlated and impactful when all of the validators in a staking provider are operated by the same organization. Reliance on stETH effectively achieves higher levels of diversification relative to working with single counterparties, keeping the exposure to any one node operator within a narrow band.

A visual representation of this diversification is in the distribution of stake within Lido stETH to its underlying node operators. Many of these are professional node operating companies themselves. Through Lido stETH, the concentration risk to any single node operator is constrained programmatically.

This diversified exposure also contributes, as a public good, to the broader robustness of the Ethereum blockchain as a whole, ensuring that the operation of the consensus algorithm remains distributed across many counterparties and mitigating single-point risk.

Furthermore, as fully on-chain infrastructure, stETH offers its users, as well as the broader public, full transparency into the mechanism of the protocol.

Finally, from a purely product-based perspective, the availability of deep secondary market liquidity can help ETP issuers build exchange traded products with a larger percentage of the NAV allocated to securing the Ethereum network and therefore sharing in its cryptoeconomic rewards. Existing Ethereum staking ETPs are unable to offer this, as staking is inherently an illiquid activity that requires ETH to be locked in place through public smart contracts. Therefore, the ability for an ETP to guarantee fully liquid redemptions is constrained.

Consequently, these illiquid ETPs must keep a certain amount of ETH reserves unstaked in order to guarantee an efficient flow of subscriptions and redemption. As an example, an Ethereum staking ETP such as 21 Shares’ AETH offers investors in the ETP an equivalent of ~1.5% staking rewards, relative to the prevailing rate which is closer to 3.5% at time of writing. A comparable product entirely based on stETH would not have to face this constraint and would be able to grant a more efficient and lower cost ETP for investors.

We take the view that such a product would be equivalent to existing ETH or ETH staking products, in the sense that they all represent ETPs with underlying digital asset commodities. Crucially, stETH is not in itself a staking service, so use of the token, including minting and burning, does not represent an outsourcing of functions or operations by an ETP issuer. We believe the stETH or wstETH digital asset commodities are sui generis digital assets with strong utility characteristics. These tokens are themselves no more financial investment instruments nor securities than ETH or BTC, for similar reasons.

An stETH-based ETP provides investors with access to a wider pool of staking rewards. Unlike staking products tied to a single counterparty, stETH-based ETPs diversify the sources of staking rewards. This reduces the impact of any single validator's performance issues or failures, offering investors a more resilient and reliable product. This also leads to a more decentralized and stable return.