Securing the EF’s Future

Sustaining Its Endowment & Upholding Values through DeFi

Abstract

The recent Crypto Twitter discussions on the Ethereum Foundation’s deployment of its treasury to DeFi has inspired the chefs at Steakhouse to revisit the topic of on-chain treasury management. In this article, we share our perspectives on how foundations could engage with DeFi and on-chain opportunities. The TLDR is:

Like traditional foundations and endowments, the crypto treasury management philosophy should prioritize asset-liability management to generate sufficient liquidity to fund expenses

DeFi deployments should align with a foundation’s investment policy statement and mission

A clear protocol evaluation and selection process could help keep the foundation’s relationship with the ecosystem neutral, while showing support to protocols that are aligned with the foundation’s longer term mission and values

Similar frameworks could be adopted by DAOs and other protocol teams overseeing a treasury

The EF has historically focused on funding protocol-level R&D, education, and community building. However, with DeFi's growing importance to Ethereum’s adoption and the EF’s sizable treasury (estimated at ~$900M–$1B), there appears to be increasing interest in how the EF can support DeFi protocols aligned with Ethereum’s core values of decentralization, open access, scalability, and security.

Our view is that EF’s treasury deployment into DeFi protocols should flow first and foremost from a robust and holistic investment policy aligned with the Foundation’s mission.

DeFi teams have already begun lobbying for EF allocations in a piecemeal and fragmentary manner. However, we believe that, like traditional foundations or endowments, the EF’s treasury philosophy ought to prioritize asset-liability management, and risk mitigation to ensure liquidity for perpetual funding. A structured, rules-based evaluation process for protocol selection could maintain neutrality while supporting the DeFi ecosystem, particularly those aligned with the Foundation’s long-term mission and values. Such a framework can be similarly applied by DAOs and other protocols when considering deploying their treasuries into DeFi.

How should a Foundation determine its Treasury Management strategy?

Foundations resemble endowments in their objectives and structural constraints. They usually bear a fiduciary responsibility to pursue the objectives defined by their founding documents. This outlines the types of grants or mission-driven activities they must support. Their investment horizon is longer than that of traditional companies, often near-perpetual, driven by the long-term public good they serve.

To design an effective investment strategy, a Foundation’s Board must align its assets with anticipated liabilities, namely future grant distributions. This process of portfolio immunization typically involves an investment policy statement that ensures grant obligations can be fulfilled on a regular basis and balancing risk and returns to maintain or grow the endowment over time.

No absolute formula dictates the precise strategy that for instance, a Swiss Foundation is obligated to pursue. However, the voluntary Swiss Foundation Code sets out a few guiding principles, that stress the importance of maintaining the Foundation’s mission in mind:

“Everything that a foundation does forms part of a cohesive whole. Its grant-making activities, asset management and administration combine to produce an overall impact. [...] The investment strategy is implemented in such a way that the investment targets are achieved with minimal costs, whilst observing the foundation’s liquidity requirements.”

Looking at the public disclosure of the EF’s activities, we can see that a simplified balance sheet as of October 31, 2024 was approximately as below.

Given the EF’s historical annual grants of $100-150 million - equivalent to c.10-15% of its fiat asset value - its endowment must generate sufficient returns (including ETH price appreciation) to preserve principal and ensure long-term financial stability.

The problem set then is how does the balance sheet generate c.10-15% returns in fiat terms including ETH price appreciation? To our minds, there are three broad categories of asset allocation decisions:

Tactical sale of ETH (preferably when markets are strong) to raise fiat

Generate yield on ETH

Generate yield on fiat or stablecoins

To date, the EF has regularly undertaken 1) to meet its funding requirements, though 2) and 3) do not appear to have been the historical focus of the treasury strategy. With the Ethereum DeFi ecosystem becoming increasingly more mature, with the Lindy effect of certain protocols becoming proven out, a modest DeFi allocation could begin to close the gap to the target return.

Rates Opportunities on ETH

The two main DeFi rates opportunities on ETH are through staking and lending.

Staking rewards have generally provided higher APY compared to ETH supply rates on main lending protocols. For instance, the 1-year average Lido stETH Yield is 3.1% versus the 1-year average ETH supply rate on Aave’s V3 main market of 1.9%. However, the tendency is for supply rates to generally trend up in bull markets, while the staking APY, though relatively stable, has been trending down with the decline in consensus rewards due to Ethereum’s higher staking ratios.

An interesting development in Ethereum DeFi in 2024 has been the emergence of modular lending protocols like Morpho and Euler. Monolithic lending protocols like Aave, Spark or Compound are time-tested, though rely on a singular DAO-led risk management. Meanwhile, modular protocols allow lenders to more finely tailor their risk exposure but are newer and have less track-record.

For instance, low-risk investors using modular lending protocols may choose to allocate to conservative vaults that lend to overcollateralized borrowers with only liquid blue-chip collateral (e.g. wstETH). In contrast, higher-risk lenders with higher APY expectations may choose to supply to vaults that accept a broader range of collateral, such as other liquid staking tokens (LSTs) or liquid restaking tokens (LRTs), in exchange for higher yields.

Rates Opportunities on Stablecoins

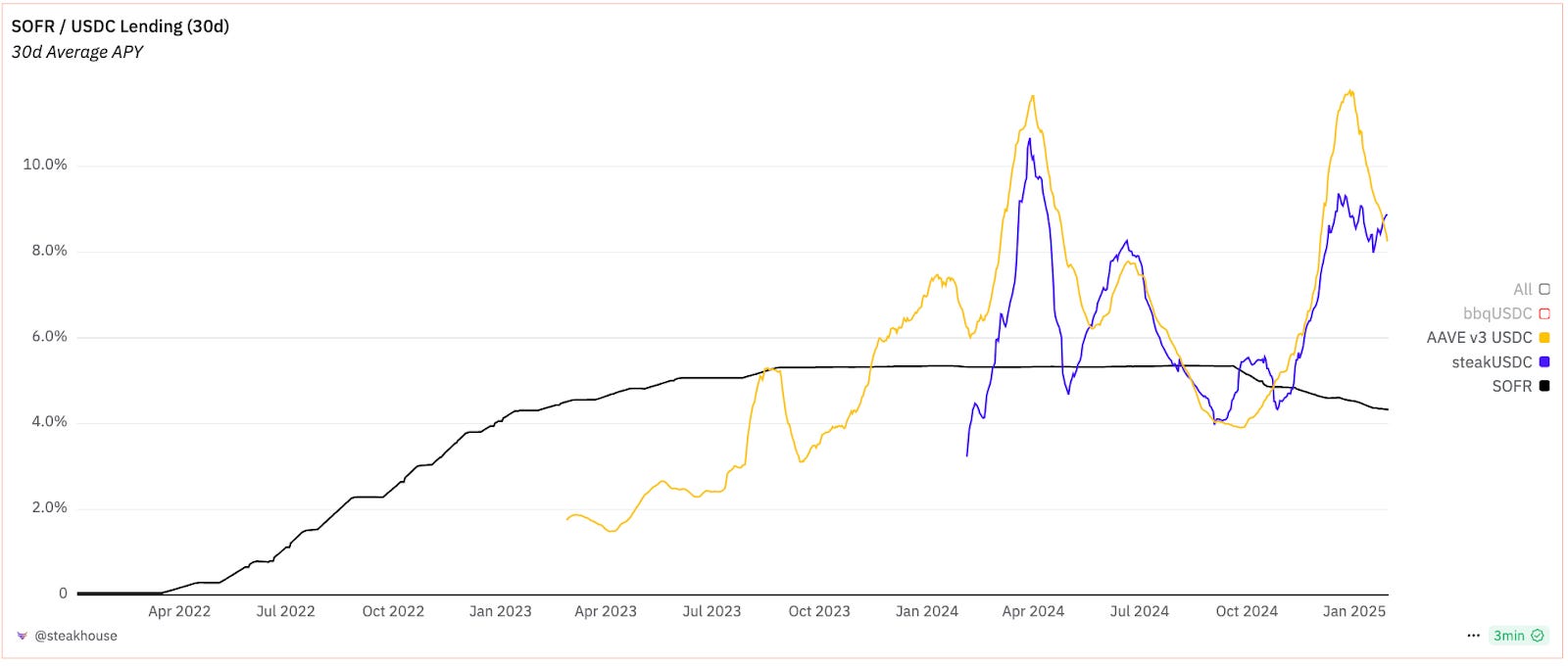

The main DeFi yield opportunity on stablecoins has been through overcollateralized lending. The below chart shows the cyclicality of stablecoin supply rates on major lending protocols. Demand for leverage was low through the bear market of 2022 and 2023, resulting in on-chain lending rates being below the SOFR (Secured Overnight Financing Rate). Rates have been rising steadily since, with periods of high utilization pushing up rates into the double digits in March and December of 2024. Since launch in the beginning of 2023, lending USDC on Aave V3 has averaged 5.6% vs. SOFR’s 5.1%.

Beyond overcollateralized lending, on-chain yield opportunities are beginning to broaden out. Ethena, for instance, has tokenized CEX funding rates and popularized it in DeFi via sUSDe, which has often offered higher yield than traditional lending. Since launch, sUSDe median and mean APRs have been ~12% and 14%, with highly speculative periods providing for materially higher rates. Admittedly, these yields come with added risks, including duration risk (e.g. 7-day cooldown from unstaking sUSDe into USDe) and counterparty exposure (e.g. custodians, exchanges). These cash and carry yields have been composed with other stablecoins, including Sky’s sUSDS, which currently yields 12.5%.

Going forward, we anticipate increased tokenization of real-world assets, expanding on-chain yield options across varying duration and credit risk levels, akin to traditional finance. We monitor developments in this space closely, releasing economic and legal reviews of instruments we use ourselves. We also participate in general curation and selection of tokenized instruments as part of our mandates for Sky or Arbitrum.

The $180m allocation in off-chain assets was rational prior to the era of tokenization. Ever since we launched an RFP on the MakerDAO forums in 2022, the tokenization landscape has rapidly developed and viable options now exist for allocators looking for exposure to traditional financial instruments custodied through on-chain wallets or safes. Nowadays, the $1bn RFP (Spark Grand Prix) for tokenized assets that Steakhouse curated on behalf of the Sky community saw entrants from a wide range of the financial services industry, a strong indicator of the maturity of the space.

Assuming most of the EF’s assets are held in short-term liquid fixed income instruments in CHF and USD, in order to meet short-term funding obligations, we could propose a rebalancing from off to on-chain. Not only would this likely lower costs for the Foundation but it would also increase transparency into the off-chain component of the EF’s holdings.

Off-chain obligations: Based on our extensive experience with Cayman and Swiss Foundations alike, we estimate it would be prudent to reserve $10m in short-term franc-denominated instruments in regulated Swiss banks in order to meet Foundation administrative and operational upkeep expenses for a very long-term period. The remaining $170m could comfortably be moved to comparable instruments on-chain.

We don’t have insight into what the off-chain allocation strategy might look like today. We propose a liquid short-term stablecoin investment policy where the EF could similarly pick multiple providers in order to avoid kingmaking and promote the development of a thriving ecosystem, prioritizing decentralized and open community-driven protocols.

A simple treasury strategy for DeFi engagement

The EF’s engagement with DeFi should ultimately serve two parallel objectives: preserving fiduciary responsibility to sustain its endowment while advancing the ecosystem through value-aligned and deliberate choices. To operationalize this, the EF could anchor its protocol selection process to a set of transparent, measurable criteria that reflect its core principles and keep a robust conflict-of-interest policy front and center. The goal may not be to maximize returns at all costs, but to deploy capital in ways that reinforce Ethereum’s long-term vision of decentralization, security, and open innovation, while prudently managing financial risk.

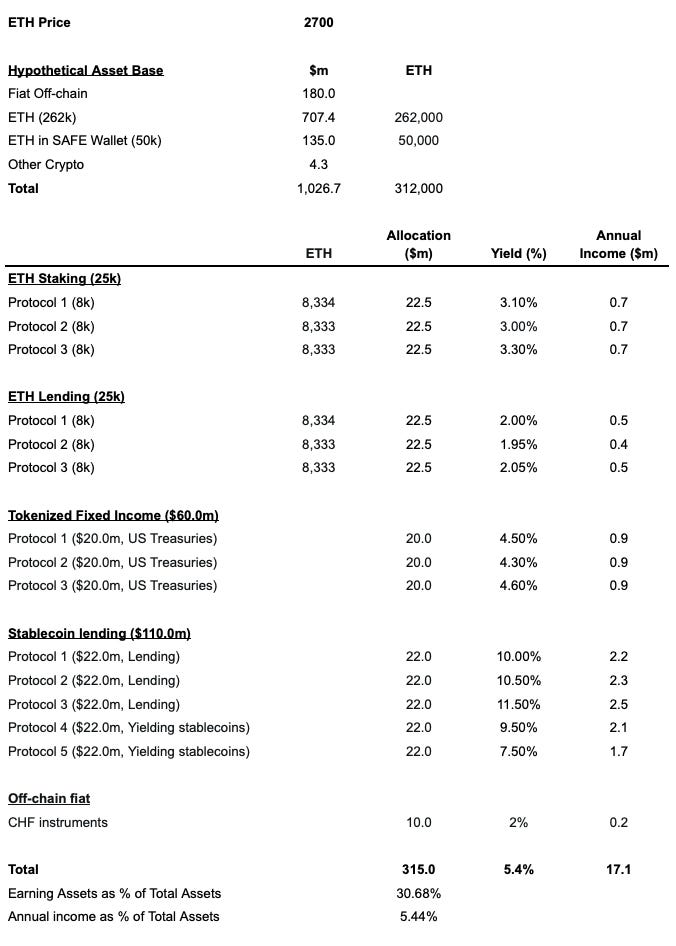

An illustrative allocation - assuming 50K ETH and $180m of off-chain assets are deployed into DeFi - is shown below. In order to avoid winding down the principal value of the Foundation’s endowment, the assets must generate a 10-15% net return in fiat terms, inclusive of the price appreciation of ETH, assuming continued EF grant distribution is equivalent to the current run-rate. Selling ETH to meet fiat currency obligations is a reasonable proposition, though logically not sustainable as the only strategy pursued. Yield generation through the combination of ETH staking, lending and stablecoin lending begin to close the gap to the target return.

There is ongoing debate about whether the EF should sell or borrow against its ETH to fund grants. The tension between the two stems from a difference in understanding of the primary objective of a Foundation.

If the purpose of the EF is mainly to be ‘bullish’ on ETH and accumulate as much of it as possible in a directional way, then the liabilities need to vary to match the assets, so pro-cyclically increase and decrease along with the price of ETH (noting that bear market pro-cyclicality may aggravate the bear market by depriving the ecosystem of development)

If the purpose of the EF is to fund development of the protocol and nurture an ecosystem building on top of it, then the assets need to vary to match the liabilities, potentially meaning that the EF sells ETH even if the price is low

We take the latter position in this exercise and assume that the main objective of the EF is to fund grants that can continue to develop Ethereum and that therefore selling ETH is a logical tool to meet obligations in USD.

An example allocation below shows that if ETH and fiat were deployed into ETH staking, lending and other on-chain stablecoin yielding opportunities, the EF could generate roughly a tenth of the spending needs. This implies that the proposed deployment to income-generating opportunities may not be sufficient to meet the current annual spend. To achieve an income target, a larger proportion of ETH than 50k may need to be allocated to DeFi, sold for stablecoins and allocated into yielding opportunities, or deployed into higher-yielding opportunities through leverage. However, increasing balance sheet leverage is structurally unsound for a Foundation, especially when there are no expected future accruals in the base asset. From the EF’s perspective, borrowing should be reserved for instances when there are significant short-term funding gaps that can be bridged temporarily with a borrowed position.

Additionally, the EF’s ~$180m in fiat/off-chain exposure reflects a clear opportunity for the EF to support DeFi and the blossoming real world asset (RWA) sector. There is no shortage of dollar denominated lending opportunities across DeFi that would enable the EF to earn high single digit APYs to low double digit APYs with relatively low risk.

Real world assets are another suitable opportunity given the very low risk nature of the products in this category. Tokenized public securities have grown from $500 million to $2.5 billion TVL over the past year on Ethereum mainnet alone, with leading financial institutions launching products such as BlackRock, Fidelity, and Franklin Templeton. Allocating to the lowest risk RWAs would enable the EF to earn ~4% in yield on idle cash.

Building a robust evaluation and selection process

In light of the EF’s value of subtractive neutrality and the inherent risks of endorsing a DeFi protocol, it’s imperative for the EF to consider a measured allocation strategy that maintains community’s trust. This could be supported by a structured evaluation and selection process that considers factors like:

Overall Budget Allocation: Designate an initial capped percentage of the EF’s treasury for DeFi protocol support (e.g., 15-20%), scaling over time to be able to reach the EF’s income target subject to risk management. By beginning conservatively, the EF can learn from real-world feedback and refine the program as needed.

Per-Protocol Funding Cap: Impose a ceiling on how much of the EF treasury can be allocated to any single protocol (e.g., 2.5–5%). Limiting exposure to individual projects avoids “kingmaking” scenarios and mitigates risk. It also encourages a broader distribution of support across the DeFi landscape.

Staged Deployment: Rather than a lump-sum contribution, allocate funds gradually based on periodic evaluations. Each stage can hinge on meeting security milestones, governance upgrades, or protocol performance metrics. Staged releases motivate ongoing diligence, encourage sustained collaboration between the EF and the project team, and allow adjustments if conditions change.

Periodic Reviews and Rebalancing: The EF should review allocations at regular intervals (e.g., every 6 or 12 months). If a protocol’s risk profile or ethos alignment evolves, the EF can reduce or divest its position. DeFi is fast-moving. Regular, transparent reviews ensure the EF adapts to changing market conditions, security discoveries, or governance shifts, always keeping the community’s best interests in mind.

Values-based Prioritization: Finally, prioritising the use of applications that could advance core values such as decentralization, permissionlessness, transparency and so forth. A simple allocation key could target a level of DeFi utilization of the Foundation’s endowment that prioritizes applications that distribute authority through on-chain governance, DAOs and community-led decision-making, for example, while still reserving the right to use centralized applications such as USDC or USDT.

By allocating a portion of its treasury to winning and emergent products, the EF can help promote DeFi development and encourage value-aligned innovation. Forward-looking protocols experimenting with new DeFi primitives and aligned with Ethereum’s core values can benefit from EF backing in a self-reinforcing loop, fueling a new wave of creativity and research. Finally, publicly endorsing protocols that emphasize decentralization, security, and permissionlessness sends a clear signal to the broader ecosystem about the standards to which the community collectively aspires.

Conclusion

Ethereum, since launch, has grown into a robust platform for decentralized applications, particularly in the area of DeFi. Over the past few years, DeFi protocols have transformed Ethereum into a global financial layer, securing >$100 billion dollars and delivering open access to financial services worldwide. By allocating a portion of its treasury to time-tested or strategically vital protocols, the EF can fulfill the dual function of generating income to financially support the ecosystem, while also helping secure key DeFi infrastructure, instilling further confidence among developers and users.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, or legal advice. The views expressed herein are those of the authors at Steakhouse Financial and are based on publicly available information and our professional analysis. Nothing in this article should be construed as a recommendation or endorsement of any specific investment strategy or asset allocation. Any references to specific protocols, products, or investment strategies are illustrative and should not be interpreted as financial advice or a solicitation to invest. Readers should conduct their own due diligence and consult with professional advisors before making any financial or investment decisions. Steakhouse Financial and its affiliates disclaim all liability for any losses or damages arising from reliance on the information contained in this article.