MakerDAO Financial Report 2022

Despite a challenging 2022, MakerDAO closed the year with a positive surplus and groundbreaking new developments in real-world assets.

Legal Disclaimer

This communication is provided for information purposes only. This communication has been prepared based upon information, including market prices, data and other information, from sources believed to be reliable, but such information has not independently been verified and this communication makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This content is provided for informational purposes only, and should not be relied upon as legal, business, investment, financial or tax advice. You should consult your own advisers as to those matters. References to any digital assets and the use of finance-related terminology are for illustrative purposes only, and do not constitute any recommendation for any action or an offer to provide investment, financial or other advisory services. This content is not directed at nor intended for use by the MakerDAO community (“MakerDAO”), and may not under any circumstances be relied upon when making a decision to purchase any digital asset referenced herein. The digital assets referenced herein currently face an uncertain regulatory landscape in not only the United States but also in many foreign jurisdictions, including but not limited to the United Kingdom, European Union, Singapore, Korea, Japan and China. The legal and regulatory risks inherent in referenced digital assets are not the subject of this content. For guidance regarding the possibility of said risks, one should consult with his or her own appropriate legal and/or regulatory counsel. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any decision. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.

Executive summary

Although the Maker protocol closed 2022 with positive earnings, it experienced a sharp decline in revenues due to headwinds in the crypto-lending sector. Despite these challenges, the protocol pioneered groundbreaking new exposures to real-world assets (RWA), setting the stage for further diversification of Dai collateral types. We believe this activity is essential to ongoing efforts to diversify the collateral backing and sustainability of Dai .

In 2022 we saw:

A transformation for MakerDAO as the overwhelming majority of protocol economics went from being exposed to market demand for crypto-backed lending to real-world assets

A 43% decrease in overall Dai balances, from 9bn DAI at the end of 2021 to 5bn DAI at the end of 2022, driven by a challenging macro environment, interest rate hikes by central banks and a tremendous deleveraging in crypto due to the irresponsibility, misconduct and inappropriate risk management by large investors and centralized financial intermediaries

An 80% reduction in net protocol operating earnings, from 90m DAI in 2021 to 19m DAI in 2022, driven by a 42% reduction in total net revenues from 112m DAI in 2021 to 65m DAI in 2022 and an increase in operating expenses from 21m DAI in 2021 to 46m DAI in 2022

A growing share of assets allocated to RWA, including groundbreaking transactions involving US treasury bill ETFs, resulting in RWA vault balances up to 640m DAI by year-end vs 17m DAI at the end of 2021

Net interest margin (NIM)1 and return on assets (ROA) still under-optimized with a large portion of the peg stability module (PSM) continuing to earn 0% (2.7bn DAI at year-end)

MakerDAO could optimize its balance sheet further by seizing opportunities following ALM Framework guidelines

That the overall exposure to stablecoins isn’t risk free, as highlighted by numerous community voices with respect to GUSD or the prospect of USDC blacklisting the PSM

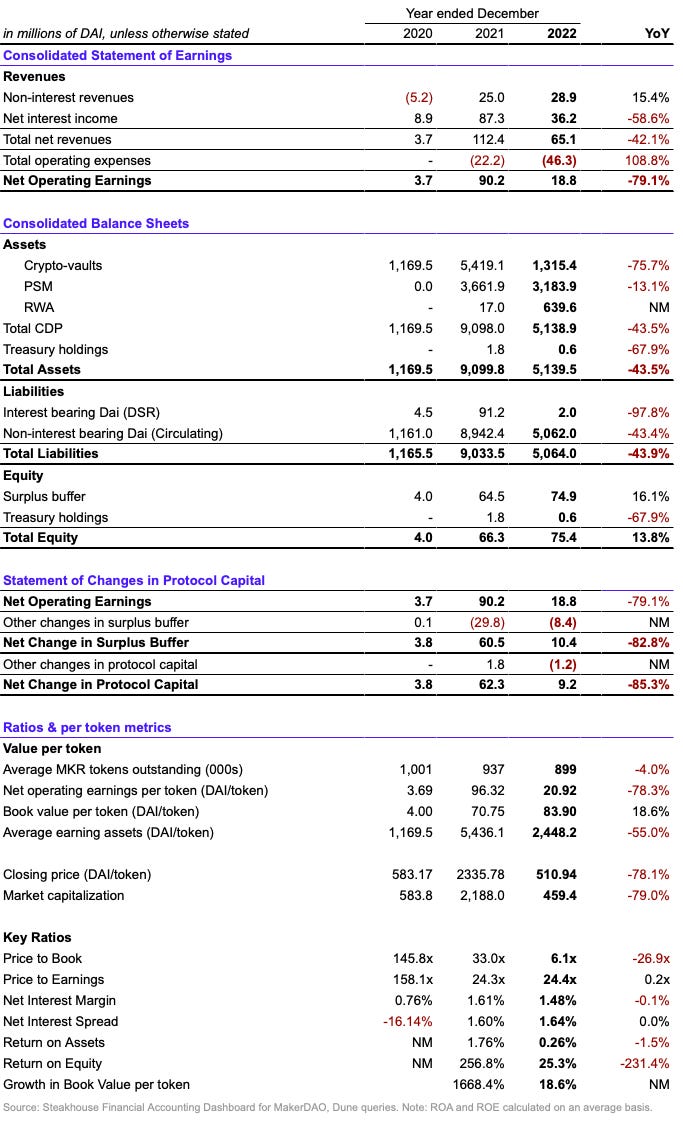

Key financial results for the Maker protocol

Net protocol operating earnings of 19m DAI on total revenues of 65m DAI, inclusive of token compensation expenses

Change in protocol surplus of +10m DAI, +9m DAI including value of tokens held in treasury (as always, excluding MKR tokens)

RWA increase from 17m DAI to 640m DAI, mostly in the second half of the year, crypto-vaults down from 5.4bn DAI to 1.3bn DAI

2022 Financial Statements

Overall, Maker protocol financial results declined precipitously relative to 2021, on the back of a major deleveraging cycle that unwound a large amount of lending demand for crypto collateral

Throughout the year, protocol surplus grew largely thanks to ongoing liquidation income from market volatility, which ended higher on the year

Crypto interest income hit a floor by June 2022, with little additional compression from market turbulence

Maker MOMC decisions drove rates lower to contribute both to the stability of the protocol and to maintain some stickiness in vault positions

Legacy stablecoin vaults (USDC-A, GUSD-A, USDP-A) were liquidated in December to a slight liquidation loss, necessary to unwind a nominal amount of bad debt that had accumulated through phantom stability fees

RWA vaults roared to life just as crypto lending slowed, with a 100m DAI vault opening for Huntingdon Valley Bank and a 500m DAI vault opening for Monetalis Clydesdale

Additional insights on 2022

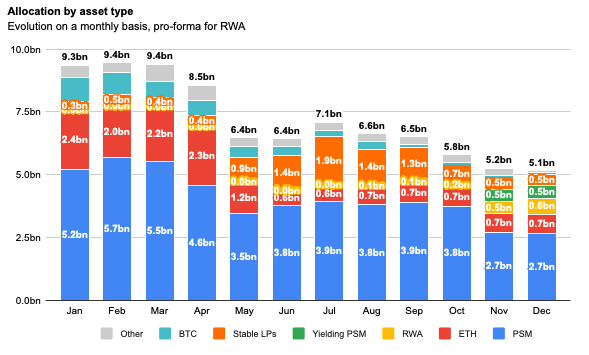

Balance Sheet Evolution

Despite Dai’s soft-peg to the dollar, the Maker protocol balance sheet has been underallocated to productive assets that could earn a positive interest spread. Our team has been advocating for improving the return on assets as, according to our ALM research and modeling of user activity, the Maker protocol was holding an excessive amount of liquidity in the PSM reserves.

The larger narrative is that MakerDAO exited 2022 unscathed through unprecedented market volatility that unwound extractive and criminal elements from our industry. It emerged in 2023 with the bones of a healthy asset allocation framework for a decentralized dollar-tracking stablecoin.

Between January and December, the balance sheet unwound without any impact to the peg or Dai’s stability from 9.4bn DAI at its peak to 5.1bn at the trough at the end of December. Within that change, two major shifts occurred:

A substantial decline in crypto lending as a proportion of the overall balance sheet

Real-world asset exposure increasing >10% of total Maker protocol assets, at about 640m DAI worth–an industry precedent and gamechanger

We introduce a simplified framework for the balance sheet, namely:

Crypto-loans

BTC

ETH and stETH

PSM

Yielding

Non-yielding

RWA

Public credit (US Treasuries)

Private credit (BlockTower)

Other

Within this framework, we also saw yielding PSM assets increase to over 450m DAI behind a Gemini proposal to pay marketing incentives whenever the exposure exceeds a minimum threshold. In our view, the ideal PSM asset is liquidable on-chain, quickly redeemable off-chain, has transparent and verifiable asset reserves, and compensates Maker adequately for its presence in the protocol. At the end of December, our non-yielding stablecoin reserve still represented over 50% of total assets. Nonetheless, we have clearly started moving in the right direction towards correcting this imbalance.

The above chart reflects pro-forma gross revenues, before oracle costs and before set-up costs for RWA vaults. It will therefore not match on-chain revenues 1:1. However, it is meaningful to note that, towards the end of the year:

Crypto-lending revenues compressed to a steady run-rate of about 1m DAI a month

In December, when US Treasury allocations were finally executed and Gemini marketing incentives started coming in, RWA interest revenues alone accounted for 2m DAI

The overwhelming majority of interest revenues in December (ca. 1.3m DAI) came from public credit exposure through Monetalis Clydesdale, with another 0.3m DAI from Huntingdon Valley Bank loans.

Dai Liquidity and Maturity

The Strategic Finance Core Unit has developed a data-driven heuristic for monitoring Dai maturity 6 on-chain, a key variable for token holders to understand as they set the asset allocation policies. In this view, Dai is split between so-called ‘speculative Dai’, locked in DeFi contracts, and ‘organic Dai’, held in EOAs or long-term addresses.

The heuristic was developed using intuition from the May 2022 market crash, which saw a substantial portion of Dai held in EOAs remain in wallets. This was as opposed to Dai held in treasuries, DeFi contracts, bridges, etc. which were rapidly unwound as traders pulled their positions. This behavioral data point gives us an idea of the proportion of Dai that is held as a deliberate decision, rather than as a speculative gamble.

The maximum drawdown of each group can be estimated to categorize the maturity of each vintage of Dai at any given point in time. The usefulness of this model is in helping Maker governance understand the average expected maturity for Dai redemptions. The insight is that although Dai can functionally redeem within a block for underlying collateral, in practice it is much stickier, which correspondingly allows for some maturity extension on the asset side.

Dai is one of the few stablecoins that continue to see organic usage, akin to the distribution visible in USDC and to a lesser extent, USDT. Most other centralized or decentralized stablecoins over concentrate liquidity in centralized choke points or have limited on-chain utility beyond reflexive liquidity mining. Throughout the turbulence of 2022, much of the unwinding of Dai’s circulating balance came from a handful of contract types, notably decentralized exchanges and bridges.

Throughout the year, the amount of DAI locked in the Pot, to earn the Dai Savings Rate (DSR), declined from >100m DAI to almost 0, dramatically reducing interest expenses. As interest revenues from RWA vaults started to come into view, the Maker Open Market Committee (MOMC) proposed experimenting with raising the Dai Savings Rate from 0.01% to 1.00% at the end of the year.

One of MakerDAO’s core strategic advantages relative to other lending protocols remains the broad use and adoption of Dai as a currency of exchange throughout the ecosystem, as well as in the meatspace economy in limited instances. Designing mechanisms to reward Dai holders for entrusting their capital with the protocol is a sound allocation strategy that could see interest expenses increasing if the ROA improves substantially.

Crypto-vaults

Maker governance responded to early market turbulence by cutting rates on vaults, with a view to ease liquidation auctions, minimize the likelihood of cascades being triggered on large vaults and incentivize vault maintenance but not necessarily full exits.

The Risk CU worked on an impact analysis to uncover the changes brought about by bringing wstETH-B stability fees to 0%. They found that stETH exposure actually increased from 150m DAI to 170m DAI during the fee cut period despite a 30% drop in the collateral price, largely due to a single whale opening new positions.

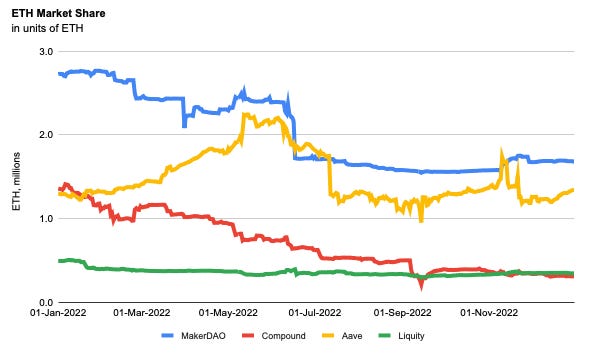

Generally, stablecoin borrows have declined precipitously across key protocols, suggesting there has been substantial and likely durable de-risking from the overall crypto-lending markets.

Maker revenues declined roughly in line with the broader crypto-lending market in key ilks such as ETH or WBTC. ETH locked in collateral among the top protocols by TVL declined about 40% from the end of December 2021, with Aave broadly holding on to share (net positive market share by volume) and Liquity declining slightly less than market, both largely at the expense of Compound.

The WBTC market has seen a marked drawdown, with a 30% decline in WBTC outstanding from 258k BTC at its peak at the beginning of the year to ca. 184k by December 2022. Maker roughly tracked this decline in circulating tokens and fell to third place amid the loss of large whale users (Celsius exited in July 2022 and Nexo followed in December 2022).

Greater access to real-world asset collateral introduces a key new element of diversification to protocol revenues, increasing the sustainability of durable DSR increases and increasing the likelihood of future burns (on pause since the beginning of the year). The tradeoff is the introduction of new elements of risk in the equation, with real-world and legal considerations that token holders must weigh on the balance when making governance decisions.

Asset-Liability Management view on 2022

As defined in the ALM Framework, a stablecoin protocol must observe two hard constraints to make DAI safe: solvency, i.e. sound backing of DAI, and liquidity, i.e. keeping the peg strong.

You can find the ALM structure of MakerDAO at the end of 2022 here with the key components reproduced below.

At the end of the year, and consistently over the year, the asset allocation was heavily focused towards stablecoins with a ~70% exposure. Of those, the DAI/USDC LPs are yielding almost nothing and only GUSD exposure (increased to 500m DAI at the end of the year) was yielding 1.25% (now 1.5%).

As one can see in the liquidity metric, the overweight exposure to stablecoins makes the protocol much safer than strictly required in terms of liquidity.

Most of the earnings of MakerDAO at the end of year are derived from public credit (currently only Monetalis Clydesdale), driving about half of Maker revenues for only a 10% exposure.

By the start of 2023, on an annualized basis, the protocol is poised to generate over 43m DAI in revenues across a range of assets but largely RWA vaults. Assuming 36m DAI of expenses, this would leave 7m DAI in net operating earnings to the protocol.

On the solvency constraint, Capital at Risk was estimated at 86m DAI at the end of the year versus a 75m DAI Surplus Buffer. Nevertheless this still feels sensible as one could attribute a potentially lower capital at risk exposure value for stablecoins (here 1%, one could also argue 0%). The Capital at Risk for crypto-backed loans is also set at 3% (normalized value) but due to the low exposure currently, in reality is probably far lower (Risk CU put it around 5m DAI at the end of the year). We still strongly recommend holding a higher Surplus Buffer to better protect the solvency of the system.

Therefore, in respect to the ALM Framework guidelines, MakerDAO is still heavily underinvested and leaving substantial revenues on the table. The overall exposure to stablecoins isn’t providing incremental safety either, as numerous community members on the forums have voiced regarding GUSD or about the risk of Circle blacklisting USDC held by the protocol.

One way MakerDAO Governance could mitigate these risks is to allocate towards money-market fund-like instruments, with a focus on three components:

Low transaction fees (which should be close to 0)

Liquid (so it can be controlled directly through on-chain governance and be liquidated safely)

Safe legal structure (diversified across jurisdictions and legally inoffensive)

If such an allocation were made, MakerDAO Governance could have sufficient revenue to gradually increase DSR (1% at the end of the year), or consider restarting the burn above a certain threshold. Increasing the Surplus Buffer should still remain a priority, in our view.

Overview of Real World Asset vaults

Ongoing risk monitoring and reporting for these vaults will be available from our team member roo on the forums.

Public Credit

Monetalis Clydesdale: US Treasuries

The Monetalis Clydesdale transaction is a 500m Dai vault collateralized by short-term United States Treasury ETFs. Roughly 70% of this collateral is allocated to IB01, holding treasuries with a maturity less than one year, and the remaining collateral is comprised of IBTA, holding treasuries with a maturity between one and three years. The vault was brought on-chain in October of 2022 and began purchasing these ETFs the same month. While there were material upfront costs, all Dai up to the debt ceiling have been deployed and the vault is generating substantial stability fees for the DAO.

Private Credit

HVB

The Huntingdon Valley Bank vault represents a 100m DAI loan participation facility with a publicly traded state-chartered commercial bank based in Huntingdon Valley, Pennsylvania. The transaction continues to build steam and create additional loans on behalf of MakerDAO. While we’re still in the process of getting additional transparency to the underlying loans, HVB has deployed in excess of 15m DAI from the 100m DAI committed to the participation. The assets to date consist of business loans, construction loans, and real estate, and are performing as expected and have not experienced any delinquency or defaults. The remaining ~85m sits in a money-market fund, which is producing substantial stability fees for Maker given where short-term interest rates have moved. As 2023 progresses, HVB is expected to accelerate the deployment of cash from the trust.

Blocktower S1-4

The BlockTower deal is composed of four revolving credit facilities, which combine for a total debt ceiling of 150m DAI and are collateralized by asset-backed facilities, forward flow agreements, whole loans, and/or structured credit products. The transaction was closed in December 2022 and BlockTower began ramping up one of the four vaults, purchasing one structured credit bond and drawing roughly 5m DAI to fund the purchase, alongside their junior capital. We expect BlockTower to continue adding assets to this vault throughout early 2023, while looking to deploy other strategies in the three remaining vaults.

Pioneer RWA Vaults

RWA vaults 001 through 005 are considered “Pioneer RWA Vaults” and represent Maker’s earliest efforts in the RWA space. The transactions, in order, are 6s Capital, New Silver, ConsolFreight, Harbor Trade Credit, and Fortunafi. Collectively, roughly 34m DAI has been issued against this collateral, with the majority held in the 6s Capital and New Silver vaults. New Silver has been making active use of their vault, where hundreds of individual loans have been issued and repaid. New Silver has received approval from the community to explore and upsize the transaction, looking for a new debt ceiling of 50m DAI. The 6s Capital vault has a balance of over 14m DAI; however, that money is sitting idly in a trust account, at the discretion of the asset originator. It’s important to note that the balance shown on-chain for 6s is accruing continuously at a rate of 3.00% and the actual amount of Dai repaid to the vault will be less than that amount.

Future developments

Entering 2023, there is a great deal of demand from asset originators ready to engage MakerDAO. The strategic finance team has been actively hiring and is increasing its bandwidth to help onboard new transactions, providing necessary risk and legal assessments as requested by the community. To start the year, the largest and most pressing deals will be in relation to the USDC PSM and BlockTower’s MIP 90 proposal. Coinbase is still actively working in concert with MakerDAO token holders and core unit teams to find a custody solution for the assets in the USDC PSM, and the execution details of MIP90, which is expected to function similarly to Monetalis Clydesdale, are actively being developed. Given the state of the crypto lending markets and the attractive short-term interest rate environment, we expect Real World Assets to be an exciting driver of the DAO and DeFi innovation in the years to come.

Mine Safety Disclosures

Ethereum’s Merge completed successfully in September 2022, so this section of the report will be discontinued until MCD launches on another proof-of-work blockchain.

Overheads and reorganization

One of the major headline features of Maker governance has been the approval of the so-called Endgame Plan, a long-term governance and organizational overhaul that aims to simplify the core protocol, leave a thin software layer, and push out organizational complexity and complex vault management to segregated teams with scrutinized access to Dai minting capabilities.

Within this plan is a proposal to continue accumulating and increasing surplus buffer equity through real-world asset exposure, before eventually migrating to fully decentralized collateral over time. The aim is to strengthen the resilience of the protocol in the face of external threats.

Throughout 2022, a lot of focus has been placed on the ongoing operating expenses of the Core Units, which peaked at ~55m DAI on an annualized basis during the summer, and closed the year at ~45m all-in of token expenses.

The expenses fell into the following categories:

4m through direct payments, delegate compensation, grants or special purpose funds

12m through MKR token vesting, typically paid out to core unit contributors

30m through overhead expenses to protocol core unit teams

Non-exhaustive list of risks

On-chain governance may encounter unforeseen difficulties when handling off-chain conflicts

Liquidations for crypto-collateral can be settled reasonably easily on-chain. However, liquidations for off-chain collateral have not been tested yet and represent a source of uncertainty to the ability of the protocol to enforce off-chain measures for maintaining collateral value.

Many vaults are reliant on third-party servicers. Any events that compromise the ability of these servicers to fulfill their obligations inhibit the DAO’s ability to monitor, secure, and collect payments in relation to the RWA vaults.

Not all vaults are credit-risk remote. Deteriorating economic conditions could impair the DAO’s collateral if not sufficiently secured by junior capital.

MakerDAO continues to be exposed to the possibility of government enforcement or seizure

Unilateral government enforcement resulting in seizure of off-chain collateral could adversely affect the integrity of the protocol and the ability of MakerDAO to maintain Dai’s tracking of the dollar.

There is realistically little that governance could do to minimize this risk further, once it has ensured that all of its off-chain collateral is safeguarded in vehicles that are in line with current legislation for the respective jurisdictions they are incorporated in.

Material changes in interest rates could negatively impact Maker’s collateral value or stability fee generation

Maker is increasing its exposure to the US yield curve with corresponding duration and interest rate risk as a result. Although most of its exposure is on the very short-end of the curve, it is nevertheless not immune to changes in market conditions that could affect the principal value of its assets.

Other Resources

https://makerburn.com

https://maker.blockanalitica.com/

https://daistats.com/

https://expenses.makerdao.network/

MakerDAO works as designed even if the world around it doesn’t

Given the backdrop of a challenging global macro environment, 2022 delivered headwinds across a spectrum of economic sectors.

Throughout this, MakerDAO continued to function exactly as designed, with all the relevant accounting informationreadily at-hand. Our friends at Makerburn regularly provide updates that are required-reading for people around the ecosystem every morning. These financial reporting innovations are a significant improvement on existing quarterly reporting standards for traditional companies. The stability of a protocol can be inspected by simply consulting blockchain transactions or by querying tables on tools such as Dune Analytics.

Where these emerging systems need improvement is on monitoring and updating transactions that take place off-chain. Although MakerDAO has pioneered real-world structures that allow the allocation of protocol owned assets in real-world investments, we are still one step removed from monitoring these transactions on a real-time basis like we can with crypto collateral. Importantly, whatever solution we come up with must allow for independent verification in order to be useful, otherwise it will suffer from the same limitations as centralized price oracles.

MKR token holders have approved MIP14c3-SP13, an RFP kick-off for third parties to propose solutions to this problem. The Strategic Finance Core Unit is taking on additional due diligence responsibilities to monitor and evaluate 1 these real-world asset vaults. Creative solutions exist as a proof-of-concept for how off-chain transactions could be recorded on-chain. There is a lot of work left to be done but we are on the right track. 2023 will hopefully bring some new innovations to continue merging meatspace and blockspace, a journey that MakerDAO itself kicked off back in the day.

Regarding our choice of accounting policies, we have made these open and subject to change. This is a collaborative endeavor with the MakerDAO community that we expect will evolve over time.

That said, we have a few key principles that we believe strongly in and likely won’t change regardless of pressure or disagreements:

Conservatism: on-chain realities rule the day as far as the protocol is concerned

In the absence of on-chain reality, we shouldn’t settle for hacks or stopgaps but work to bring them on-chain in a reliable and independently verifiable way

We can count off-chain income in a pro-forma way but this shouldn’t drive major allocation decisions

We should similarly also find ways to count markdowns in value if and when they occur as quickly as possible, and push to marking them manually if necessary, more often than necessary

Native tokens (endogenous collateral, ‘treasury tokens’, whatever you want to call it) have 0 market value

The fact that ERC-20 tokens show a balance when minted tokens are sitting in a native treasury address is a software feature and a massive, very dangerous ‘social’ bug

These tokens could be burned or 10x could be minted and have no economic impact

Releasing them into the market would make it highly unlikely to realize the market value anyway

Appendix A: Overview of Accounting Standards (Maker GAAP)

The figures in this report are illustratively organized to show what MakerDAO’s financial position resembles economically speaking. However, there is no single entity that collects the below results or speaks for its figures. The smart contracts that regulate peer-to-peer interactions are permissionless and the protocol accumulates and spends surpluses to maintain the equilibrium of the system.

We collect smart function calls and events from Dune in a master query that classifies each transaction into a place in a virtual chart of accounts. We are mapping these function calls based on the closest available parallel in traditional accounting. It is important to note that distributed ledger transactions can be meaningfully different from their traditional counterparts and these mappings should be taken with a grain of salt.

To that end, given the public and open nature of blockchain transactions on Ethereum, it is possible for anyone to query the same transactions for themselves and make their own mappings. Nevertheless, we believe these to be the first major set of crypto-GAAP standards made publicly available.

What we call the canonical view is everything that is reflected on-chain and has changed the state of the blockchain. This is a straightforward matter as far as crypto collateral is concerned.

The problem arises with real-world transactions that take place off-chain and may accrue over several months before being reflected on-chain. We have tried to solve this problem by showing a second set of pro-forma financial statements that capture the activity that has taken place off-chain, as a way of showing a reasonable approximation of the economic state of the protocol. However, this is an imperfect stopgap.

During 2022, we built on our work developing long-form financial models and results to illustrate the functioning of the protocol to a broader audience that is literate in traditional accounting terms. We have been working towards our end-state: a transaction-level accounting dashboard that is capable of classifying every single event in the MakerDAO protocol into its respective chart of accounts.

In our view, there are two fundamental business models of relevance in our industry:

Traditional companies with a crypto-component, which may make use of the blockchain to disintermediate industries and use the margin released to either build a better product or gain share by offering the same product at a lower price

Pure crypto protocols which aim, over time, to become thin application layers to mediate peer-to-peer transactions with minimal human interaction

Our team is mostly interested in developing the equivalent of a crypto-GAAP standard for financial reporting and transparency for the latter case. With the work we have done on Maker, to our knowledge, our team is the first to have mapped out a top protocol fully with a double-entry accounting ledger.

The data is available freely on Dune and we invite the community to contribute and comment. We believe an open approach to implementation is the best way to roll out crypto accounting standards, which should be the primary way that self-regulation can demonstrate the value of transparent financial record-keeping.

We are aware that our team’s data publications and Dune queries are already being recycled in commercial research publications around the industry. There is nothing preventing these players from also repackaging our crypto GAAP work and reselling it to their subscribers.

To the extent such firms end up recycling our crypto-GAAP query too, or portions thereof, we would kindly request voluntary ongoing donations of part of their subscription revenue attributable to MakerDAO reports to the Maker Pause Proxy address (0xBE8E3e3618f7474F8cB1d074A26afFef007E98FB).

The only way we can move past the sordid legacy of the crypto grifters we have been afflicted with in 2022 is by proving the potential of public blockchains for improving the common interest. We are passionate about showing how we can do better than mandatory quarterly paperwork: real-time transaction transparency and an open standard for classification.

Appendix B: 2022 Financial Statements–Pro-Forma View

These statements are the on-chain versions, with three additional key manual adjustments:

Oracle gas expenses are smoothed to actual expenses, rather than registering as single outflows

This is closer to an as-incurred perspective, which regulates the accounting between 2021 and 2022, as the 8m bullet payment in early 2022 was partly to reimburse the Maker Foundation for incurred gas expenses and partly to fund the wallet for 2022 gas expenses

Off-chain RWA vault interest income is recorded in interest income and principal balances are recorded in the balance sheet, both under a gray marking

Negative revenues are a reflection of vault opening fees and setup costs, largely behind MIP65 (Monetalis Clydesdale), offset in later months as interest revenues start to accumulate

Modified balance of Dai outstanding to close the gap

The pro-forma view is fictitious and not a representation of on-chain reality, so we can take liberties with the record of Dai in circulation to balance the statements

This is an estimate of what the protocol would look like, had the expenses and income we adjusted taken place at the times we adjusted them on-chain.

1: Defined as net interest revenues over earning assets

2: Defined as net operating earnings over average assets