Make Interest Compound Again (MiCA)

A look into EURCV

Euro stablecoins are growing rapidly under MiCA, but still only account for a fraction of the global stablecoin market. EURCV, a regulated euro stablecoin issued by SG-FORGE, is one of the first to anchor serious lending infrastructure onchain.

The Steakhouse EURCV vault on Morpho deploys euro liquidity across five lending markets, spanning ETH and BTCs collaterals, USD stablecoins, and tokenised euro money market fund shares. While deposits have grown as borrowing demand continues to build, and early borrowers face favorable rates.

This piece covers the fundamentals behind EURCV, the state of the euro stablecoin market, what the Steakhouse EURCV vault looks like from the inside, and what the emerging yield spreads in euro markets tell us.

EURCV: A Fully Regulated Onchain Euro

Today’s stablecoin economy runs almost entirely on dollars. For euro-based users and institutions, every deposit into a USD-denominated vault carries implicit foreign exchange risk. Until recently, the euro stablecoin market lacked a credibly regulated, institutionally-backed option that could anchor serious lending infrastructure.

Societe Generale’s digital assets subsidiary, SG-FORGE, issued EURCV in 2023 as a euro-denominated stablecoin. SG-FORGE was the first entity to receive a digital asset service provider license from France’s financial markets authority (the AMF) in July 2023, and it operates as a licensed electronic money institution under supervision of the French banking regulator (the ACPR). Those two licenses place EURCV under the same dual regulatory framework that governs traditional banking and financial services in France.

On 1 July 2024, EURCV transitioned to a Markets in Crypto-Assets Regulation (MiCA) Electronic Money Token. MiCA requires full reserve backing in euros, transparent reserve reporting, a 1:1 redemption mechanism, and, critically, free transferability without whitelisting. As a result, with this transition, EURCV removed whitelisting requirements instead of requiring gateway approvals to move between addresses. After it, making the token fully composable across DeFi.

The reserves backing EURCV are held in euro-denominated bank deposits and high-quality securities administered by Societe Generale, which has operated continuously since 1864. For users evaluating counterparty risk, this is a meaningfully different proposition from stablecoins issued by entities outside the European regulatory perimeter. That institutional backing does not eliminate risk, but it does change the nature of it.

The Euro Gap

In traditional foreign exchange markets, the euro accounts for approximately 28.9% of daily trading volume, second only to the dollar. Onchain, the picture looks nothing like that. Dollar stablecoins command over $315 billion in circulating supply, while Euro stablecoins, collectively, sit at approximately €710 million. The second largest currency in the world holds less than 0.3% of the stablecoin market.

The gap reflects several structural factors. The US dollar is the world’s reserve currency. Global trade, commodities, and capital markets are predominantly dollar-denominated. When the first stablecoins launched, they followed that gravity: US venture capital funded them, US exchanges listed them, and dollar liquidity drew borrowers and lenders into a self-reinforcing cycle. Even European users defaulted to USDC and USDT because that was where the depth sat.

Regulatory uncertainty affected stablecoins across the board, including dollar-denominated ones. The difference is that dollar stablecoins grew despite regulatory ambiguity, carried by the sheer gravitational pull of USD liquidity and global demand for dollar-denominated settlement. Euro stablecoins had no equivalent tailwind. Without clear rules, European institutions and users saw little reason to issue or hold euro tokens when dollar alternatives already existed and worked. MiCA, years in the making, only took effect in mid-2024. Before it, the regulatory case for euro stablecoins simply was not there.

Within the euro stablecoin market, concentration is high. EURC (Circle) is the largest euro stablecoin by supply. EURCV follows at approximately €74 million, with adoption accelerating in recent months. The remaining tracked stablecoins collectively hold a small share of the total.

The effect of MiCA has been measurable. Since enforcement began in mid-2024, the euro stablecoin market has roughly tripled in size. Over 50 crypto-asset licenses have been issued across the EU. Issuers are launching, institutions are evaluating, and the first lending markets built around euro stablecoins are beginning to take shape.

The Steakhouse EURCV Vault

A stablecoin without lending markets is just a token sitting in a wallet. Lending is what turns a stablecoin into productive capital, creating borrowing demand, generating yield for depositors, and giving users a reason to circulate the token.

More fundamentally, lending markets establish a base yield for the currency onchain. USDC lending rates on venues like Aave and Morpho have become the de facto reference rate for dollar-denominated DeFi, the equivalent of a risk-free benchmark. For euro stablecoins, no such benchmark exists yet because there is not enough liquidity depth to establish one, and these are the markets where that begins to change.

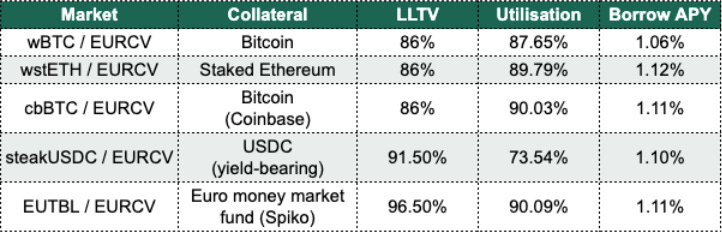

The Steakhouse EURCV vault, deployed on Morpho in January 2025, is one of the first dedicated euro lending venues onchain. It pools EURCV liquidity from depositors and allocates it across five isolated lending markets, each with its own collateral type, Liquidation Loan-to-Value ratio (LLTV), and risk profile.

Vault parameters:

Governance: Safe multisig (5/8 signers), Aragon DAO guardian, 7-day timelock

Performance fee: 0%

Net APY: 0.25% (0.19% base + 0.06% MORPHO incentives)

Total deposits: 20.36 million EURCV (~$23.57M)

Idle liquidity: 16.17 million EURCV

The vault serves five markets:

Three markets accept Bitcoin and Ethereum collateral at 86% LLTV, meaning borrowers must maintain collateral worth at least 116% of their loan. The steakUSDC market pairs a dollar-denominated yield-bearing position against euro borrowing at 91.5% LLTV. The EUTBL market accepts tokenised shares of Spiko’s Euro Money Market Fund at 96.5% LLTV, the highest capital efficiency in the vault, reflecting the tight correlation between a euro money market instrument and a euro stablecoin.

The EUTBL market is worth noting separately. EUTBL represents tokenised shares of Spiko’s Euro Money Market Fund, backed by short-term European government debt. Borrowing EURCV against a euro-denominated money market instrument is a practical example of how yield spreads form onchain: the difference between the fund’s return and the borrowing cost reflects the market’s pricing of liquidity and collateral quality between two closely correlated euro assets.

Deposits in the Steakhouse EURCV vault grew following the native integration with Safe wallet, which simplified the deposit flow for users ranging from individual holders to multisig treasuries. However, while supply has increased substantially, borrowing demand is still building its way across the markets. The capital allocated to active markets shows healthy utilisation (73-90%), but the majority of vault deposits remain idle. This is typical of early lending markets where supply arrives first and borrowing demand follows as the ecosystem matures and use cases solidify.

The Opportunity

For European users and institutions who want their onchain balances denominated in euros rather than dollars, these markets offer a direct path. A user can deposit BTC or ETH as collateral and borrow EURCV, maintaining crypto exposure while holding euro-denominated liquidity. This avoids the implicit forex risk of sitting in USD stablecoins, since if the dollar weakens against the euro, a euro-based user holding USDC loses purchasing power in their home currency. Borrowing EURCV eliminates that exposure, with current borrowing rates across the vault ranging between 1.06-1.12% depending on the market.

The natural question is why borrow EURCV instead of borrowing USDC and swapping to euros. There are two main reasons. First, the swap incurs a spread and a gas cost that often exceeds the rate differential. Second, and more importantly, borrowing EURCV means the debt is euro-denominated. A European business paying salaries, vendors, or taxes in euros avoids carrying an implicit EUR/USD position. The simplicity has real value for anyone whose liabilities are in euros.

The steakUSDC market serves a different purpose. Here, the collateral is a dollar-denominated yield-bearing position. Borrowing EURCV against it creates a direct EUR/USD exposure onchain. As a result, if the dollar strengthens, the collateral appreciates relative to the debt. This market begins to bring foreign exchange dynamics into composable lending, accessible to any user rather than restricted to institutional FX desks.

Current utilisation is high on allocated capital, but the overall vault has significant idle liquidity. For borrowers, this translates to favourable rates. As demand scales and idle capital gets deployed, rates will adjust upward. Early borrowers capture the benefit of an emerging market where supply has outpaced demand.

Risks

The most immediate risk for borrowers is similar to what users face on USD markets: collateral volatility. BTC and ETH fluctuate daily against the euro, and a sharp drawdown can trigger automatic liquidation if a position breaches its LLTV threshold. The isolated market structure means each pair has its own liquidation conditions, so risk is compartmentalised but still present. All positions also carry smart contract risk inherent to the Morpho protocol and the underlying collateral tokens, and while audits reduce, it does not eliminate this exposure. EURCV itself, while regulated, introduces counterparty risk on reserves held by Societe Generale. The bank is systemically important and has operated for over 160 years, but no institution is risk-free.

At the market level, the vault’s pools are still small relative to traditional lending. A large position entering or exiting rapidly could face slippage, and the euro stablecoin market as a whole is nascent enough that liquidity may not always be available at expected rates. MiCA is new legislation; amendments to licensing, reserve standards, or permissible use cases could affect EURCV’s operational status and, by extension, vault users. Current lending rates across the vault sit below 1.1%, and as more euro liquidity comes onchain, rates may compress further.

Euro Stablecoin Adoption is On the Rise

Yield spreads are beginning to form in onchain euro markets. The gap between EURCV lending rates and USDC lending rates reflects currency preference, liquidity depth, and the relative maturity of each market. As euro-denominated lending deepens, these spreads will tighten and begin to price the same factors that drive spreads in dollar markets: credit quality, platform architecture, and capital mobility.

The euro stablecoin market does not need to match the dollar market to be useful. It needs enough depth for borrowers and lenders to transact in their native currency without defaulting to dollar exposure as the only option. MiCA created the regulatory foundation. Institutional issuers like SG-FORGE provided the assets. Now, lending infrastructure like the Steakhouse EURCV vault on Morpho are providing the markets where those assets become productive. The rest is a matter of adoption, and adoption follows utility.

Follow Steakhouse Financial for more European poasting.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. DeFi lending involves risks including smart contract risk, liquidation risk, and market risk. Past yields are not indicative of future performance. Users should conduct their own research and assessment before interacting with any protocol or vault.