Fonbnk: Mobile payments and stablecoins in Kenya

Fonbnk’s tokenization of airtime minutes and integration with mobile money services present an innovative model with the potential to expand financial services to underbanked populations in African ma

PDF | ePub

Introduction

Founded by Christian Dufus in 2021, Fonbnk has emerged as a prominent player in the African DeFi space. The project is well-known for its unusual approach to on-ramping underbanked populations into crypto, which involves leveraging existing networks of pre-paid SIM cards to facilitate on-ramping by allowing the exchange of airtime, mobile money or bank transfers for stablecoins.

In most African countries, the overwhelming majority of mobile phone users rely on pre-paid SIM cards and a pay-as-you-go model for purchasing the necessary data. This is a departure from the subscription-based and contract-oriented systems prevalent in the global north. A primary factor influencing this difference is the economic context in Africa.

Affordability remains a key concern for a significant portion of the population, and the traditional postpaid subscription models, which are common in the global north, may be less practical. Pre-paid plans allow users to have more control over their expenses and pay for mobile services (a.k.a. “airtime”) on a need basis, aligning with the financial constraints faced by a substantial portion of the population.

Initially, telecom companies relied on airtime credits which were primarily used for purchasing talk time and data for mobile phones. The key moment came when telecom companies and financial institutions recognized the potential to expand the utility of airtime credits beyond mere communication services. These companies introduced the concept of mobile money, exemplified by groundbreaking services like M-Pesa – launched in 2007 by Vodafone's Kenyan associate, Safaricom – which marked a pivotal moment in the financial landscape. This innovation empowered users to seamlessly handle and transfer funds via their mobile devices, fundamentally transforming financial transactions, especially in regions lacking traditional banking infrastructure.

M-Pesa's introduction revolutionized the accessibility of financial services, allowing users to deposit, withdraw, and transfer funds with ease. Transaction volumes on the M-Pesa platform experienced steady growth, reaching an impressive 26 billion transactions and a volume of KES 35.86 trillion ($250 billion) for the financial year ending on March 31, 2023. This nascent digital currency could then be used for a variety of financial transactions, such as transferring money to family members, paying bills, purchasing goods and services, and even accessing credit and savings services. Widespread mobile phone ownership facilitated easy adoption, driven by a lack of traditional banking access that created demand for these alternative solutions. Now, African telecom operators run the largest mobile money businesses in the world and facilitate close to $453.6 billion of transactions in Africa annually.

With a specific focus on the Sub-Saharan African market, Fonbnk capitalizes on the continent’s extensive telecom infrastructure by offering a solution for individuals holding prepaid mobile SIM cards. The company allows such users to swap their airtime minutes, mobile money or bank deposits for stablecoins (e.g., USDC, USDT or Celo’s cUSD) across various blockchain networks including Ethereum, Polygon, Celo, Stellar Network, Algorand, Solana, TRON, Avalanche, Base, Optimism and NEAR.

Fonbnk’s tokenization of airtime minutes and integration with mobile money services present an innovative model with the potential to expand financial services to underbanked populations in African markets. The company’s approach has the potential to serve as a unique on-ramp into the crypto space for hundreds of millions of users, thus expanding access to this nascent technology to those who might have otherwise been left behind. This article delves into Fonbnk’s solution to explore how the company is positioning itself to achieve these goals.

African markets are the ideal setup for stablecoins

“In Africa, extreme devaluation of local currencies has driven the adoption of cryptocurrencies — especially stablecoins” - Duncan Muchangi, Co-Founder, Fonbnk

Inflation Dynamics in African Economies

Currency depreciation is a challenge faced by many African countries across the continent. Factors such as economic policy mismanagement, political instability, external debt, and global economic conditions have contributed to cycles of extreme currency devaluation that hurt the ability of consumers to save while also increasing the difficulty of day-to-day financial activity.

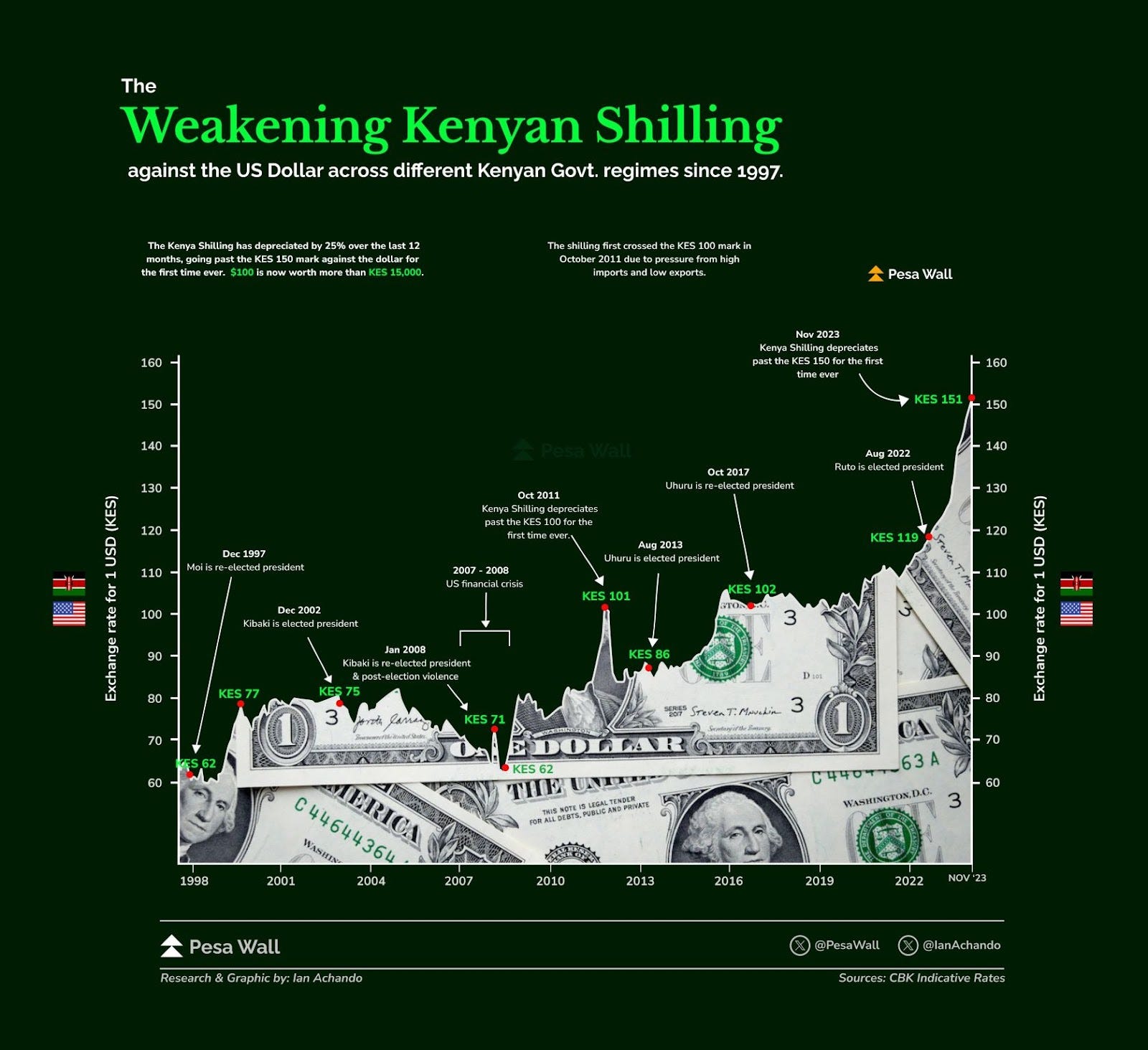

For instance, the East African reports that in the twelve months ended November 2023, the US dollar appreciated by approximately 25% against the Kenyan Shilling. Looking at a longer timeframe, the figure below from Pesa Wall shows that in December 1997, one US dollar was worth 62 Kenyan Shillings, whereas by November 2023, the exchange rate was 151 Shillings for every US dollar.

Accordingly, this example from Kenya demonstrates how African consumers and businesses have a pressing need for a reliable refuge that can protect their hard-earned money against the ravages of inflation.

US Dollar Shortages are Shaping African Economic Challenges

As reported by Bloomberg, African currencies were the worst performers in the world in 2023, with about a dozen sliding at least 15% against the US dollar. Major African economies such as Kenya, Egypt, and Nigeria grappled with mounting challenges in securing hard currencies essential for purchasing imports and meeting international financial obligations. The impact of the dollar shortages extended beyond the financial markets, affecting consumers and local businesses as import costs surged, leading to inflation.

According to Afrexim Bank’s Africa Trade Report 2023, Africa’s merchandise imports and exports grew to US$706 billion and US$724.1 billion respectively in 2022. Additionally, a 2023 World Bank Report highlighted the continued upward trajectory of remittances into Sub-Saharan Africa, reaching $53 billion in 2022.

Despite the ever-growing increase in trade and remittances, it is worth noting that the inherent dollarization of imports and exports has exposed local merchants, importers, and exporters to substantial losses, particularly with the persistent weakening of African currencies against the dollar. This phenomenon has been exacerbated by widespread dollar shortages in local banks, prompting a fervent demand for alternatives.

The strain is most evident in the devaluation of local currencies. Notably, in Nigeria, the prices of prescription drugs tripled in 2023. Over in Zimbabwe, one of the largest retailers, OK Zimbabwe, reported sales volumes below the break-even point due to rising costs and an unfavourable exchange rate. In Malawi, the price of corn, a staple food, doubled in 2023. Further, in Zambia, Mozambique, and Nigeria, challenges in securing foreign financing have compelledauthorities to increase their issuance of domestic debt in limited markets, leading to higher borrowing costs.

These complex interplays of economic forces and resultant economic imbalances have created an environment that is fertile ground for the emergence of stablecoins.

On-chain stablecoins are being used more frequently

Stablecoins are a product category in the crypto space that can credibly claim to have found strong user demand from outside the industry. In emerging markets, they provide a readily accessible haven from the persistent devaluation of local currencies. Moreover, stablecoins offer a viable solution to the U.S. dollar shortages that plague banking systems across Africa.

The utility of stablecoins has not gone unnoticed by African businesses and retail users alike. Users on the continent have begun to harness the potential of this new parallel dollar market, with USDT and USDC emerging as the leading stablecoin products.

The growth in demand for stablecoins as an alternative to combat dollar shortages has paved the way for the rise of solutions such as Fonbnk’s, with the company providing on- and off-ramp solutions for users into stablecoins.

As seen in the chart below from Chainalysis, despite a slight retreat in Q2 2023, stablecoins dominated on-chain transfer volume in Sub-Saharan Africa between July 2022 and July 2023.

Source: The Chainalysis 2023 Geography of Cryptocurrency Report

The African telecom market is rapidly growing and innovating very fast

As discussed in the introduction, the mobile telecommunications landscape in many African countries relies on prepaid SIM cards and a pay-as-you-go model for data, driven by economic contexts where affordability is crucial. Furthermore, the introduction of exclusive handsets tailored for the African market, coupled with the growing prevalence of integrated services like mobile money, has spurred the widespread adoption of mobile technology across the continent. Although

conditions differ from country to country, the prevailing trend indicates that mobile technologies are playing a pivotal role in fostering connectivity across the continent.

According to GSMA, the mobile industry contributed $170 billion in economic value to the Sub-Saharan economy in 2023, accounting for 8.1% of the region's GDP. There are 489 million unique mobile subscribers, representing a 43% penetration rate. Additionally, there are 287 million mobile internet users, indicating a 25% penetration rate. This growth is attributed to expanded 5G services across 15 countries, access to better smartphones, and a thriving fintech and mobile-money-based financial products ecosystem catering to individuals and small businesses.

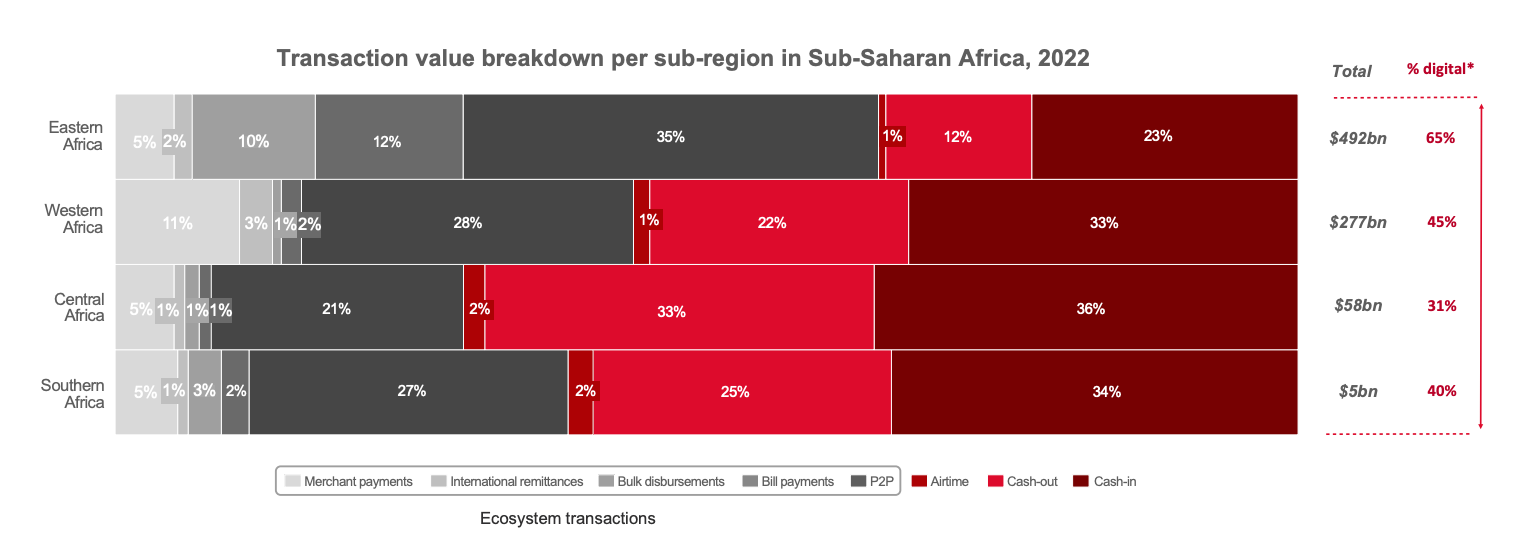

The surge in unique mobile subscribers originating from Sub-Saharan Africa is truly remarkable, constituting almost two-thirds of the global total. This region has witnessed growth in digital financial inclusion, reflected in the staggering figure of 218 million active 30-day accounts. What makes this statistic even more notable is the substantial transaction volume associated with these accounts, totalling $832 billion in 2022. Here, Eastern Africa leads the way, contributing approximately 50% ($492 billion) to this total transaction volume.

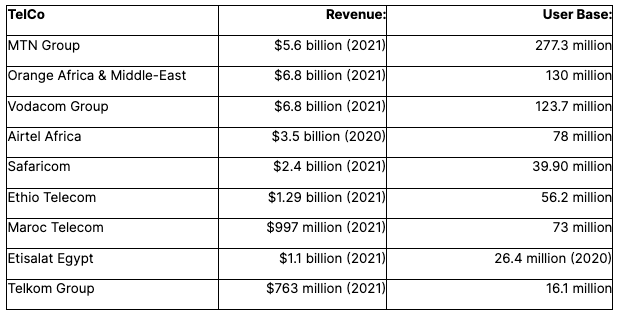

As of the latest available data, the telecommunications sector across Africa has been experiencing significant growth, both in market value and user base as summarized below:

In Africa, we find a growing mobile telecommunications landscape coupled with users that are already comfortable with the idea of digital currencies that they spend using their mobiles.

M-Pesa is a privately issued Kenyan Shilling

Mobile money services like M-Pesa run by Safaricom have empowered users to seamlessly deposit, withdraw, transfer money, pay bills, and purchase goods and services using their telco-issued phone numbers and sim cards.

The Agent Network Backing Mpesa:

M-Pesa operates through an extensive network of agents, typically local shops or small enterprises, acting as intermediaries between users and the M-Pesa mobile banking system. These agents facilitate cash-in and cash-out transactions, allowing users to deposit or withdraw physical cash from their M-Pesa accounts.

M-Pesa agents serve as vital liquidity providers within the ecosystem, facilitating the conversion between electronic and physical cash. Each agent operates with an electronic float (e-float) account directly linked to M-Pesa. Through these accounts, agents deposit funds to ensure liquidity for customer transactions. The funds deposited by agents are managed and held by M-Pesa in collaboration with partner banks such as Co-operative Bank of Kenya, KCB Bank and NCBA Bank. This setup ensures the smooth flow of funds within the M-Pesa network, enabling users to seamlessly conduct transactions using both electronic and physical forms of currency.

M-Pesa customers, utilizing their mobile phone numbers, may either, engage with fellow M–Pesa customers by sending the e-money directly from one customer phone number to another or engage with agents through two primary methods:

M-Pesa Withdrawal: Customers exchange e-money on their phones for liquid cash by sending the value to the agent via the withdraw cash option in the M-Pesa menu. This transaction increases the agent's e-float but decreases their cash on hand.

M-Pesa Deposit: Customers deposit physical cash with agents to have e-money credited to their phones. This transaction decreases the agent's e-float but increases their cash on hand. In the event the agent’s e-float is depleted due to excessive deposit events, the agent will have to deposit additional funds into their e-float account.

Send Money via M-Pesa: Users holding e-money in their M-Pesa accounts may directly send funds from their mobile phone number to another user’s mobile phone number.

M-Pesa's operation relies heavily on the management of the e-money within its treasury, making it somewhat akin to a Kenyan shilling (KES) stablecoin. Here's why:

Fixed Value Representation: Similar to stablecoins that are pegged to a fiat currency, M-Pesa's e-money is directly linked to the Kenyan shilling. Each unit of electronic money within the M-Pesa system represents a corresponding value in Kenyan shillings, maintaining a stable exchange rate.

Liquidity Management: M-Pesa agents play a crucial role in maintaining liquidity within the system. They deposit cash into M-Pesa’s treasury at partner banks to facilitate e-money transactions and vice versa, agents ensure that there is always a balance between electronic and physical currency, stabilizing the value of the e-money.

Collaboration with Partner Banks: M-Pesa collaborates with various partner banks to manage the funds within its treasury. These banks hold the deposited funds and ensure their security and stability, further contributing to the stability of e-money within the M-Pesa ecosystem.

Widespread adoption and User Confidence: With a network of over 600,000 agents and over 50 million users, users of M-Pesa have confidence in the stability of the e-money, knowing that each unit of e-money is backed by an equivalent value in local currency (e.g Kenyan shillings). This confidence encourages the widespread adoption and use of M-Pesa as a reliable medium of exchange and store of value, similar to the trust placed in stablecoins.

Despite being a product wholly owned by Safaricom, M-Pesa has developed compatibility with other mobile money platforms operated by competing telcos. This interoperability allows users to seamlessly transfer funds between M-Pesa and other mobile money services, regardless of the telco service provider. By breaking down barriers between different platforms, users have greater flexibility and choice in managing their finances, fostering competition and innovation in the mobile money sector.

Fonbnk adds USD Stablecoin integrations on top of M-Pesa and airtime minutes

"As of now, Fonbnk's operations span across five African nations, with an ambitious roadmap to extend our footprint to a total of 24 countries. We're laying down the tracks for seamless integration across Sub-Saharan Africa." - Christian Duffus, Founder, Fonbnk

The Fonbnk in-App Token: MIN

At the heart of Fonbnk's infrastructure lies MIN, an in-app ledger token designed as an accounting unit. Unlike other tokens, MIN doesn't exist on any blockchain; instead, it's a digital representation of value within Fonbnk's ecosystem. MIN serves as a ledger entry/medium of accounting representing stablecoin reserves held in Fonbnk's treasury maintaining a fixed value of $0.01 per MIN.

Within the app, MIN offers several utilities such as: (i) In-App Transactions: Users can send MIN to other Fonbnk users within the app, facilitating peer-to-peer transactions seamlessly, (ii) Conversion to USDC: MIN can be exchanged for USDC within the Fonbnk app, allowing users to withdraw stablecoins to their preferred external wallet, and (iii) Listing on Marketplace: Market makers list MIN tokens on the Fonbnk marketplace for sale, providing liquidity and enabling trading opportunities within the ecosystem.

These utilities empower users within the Fonbnk platform, enabling efficient transactions and interactions while maintaining the stability and redeemability of MIN tokens within the confines of Fonbnk's ecosystem.

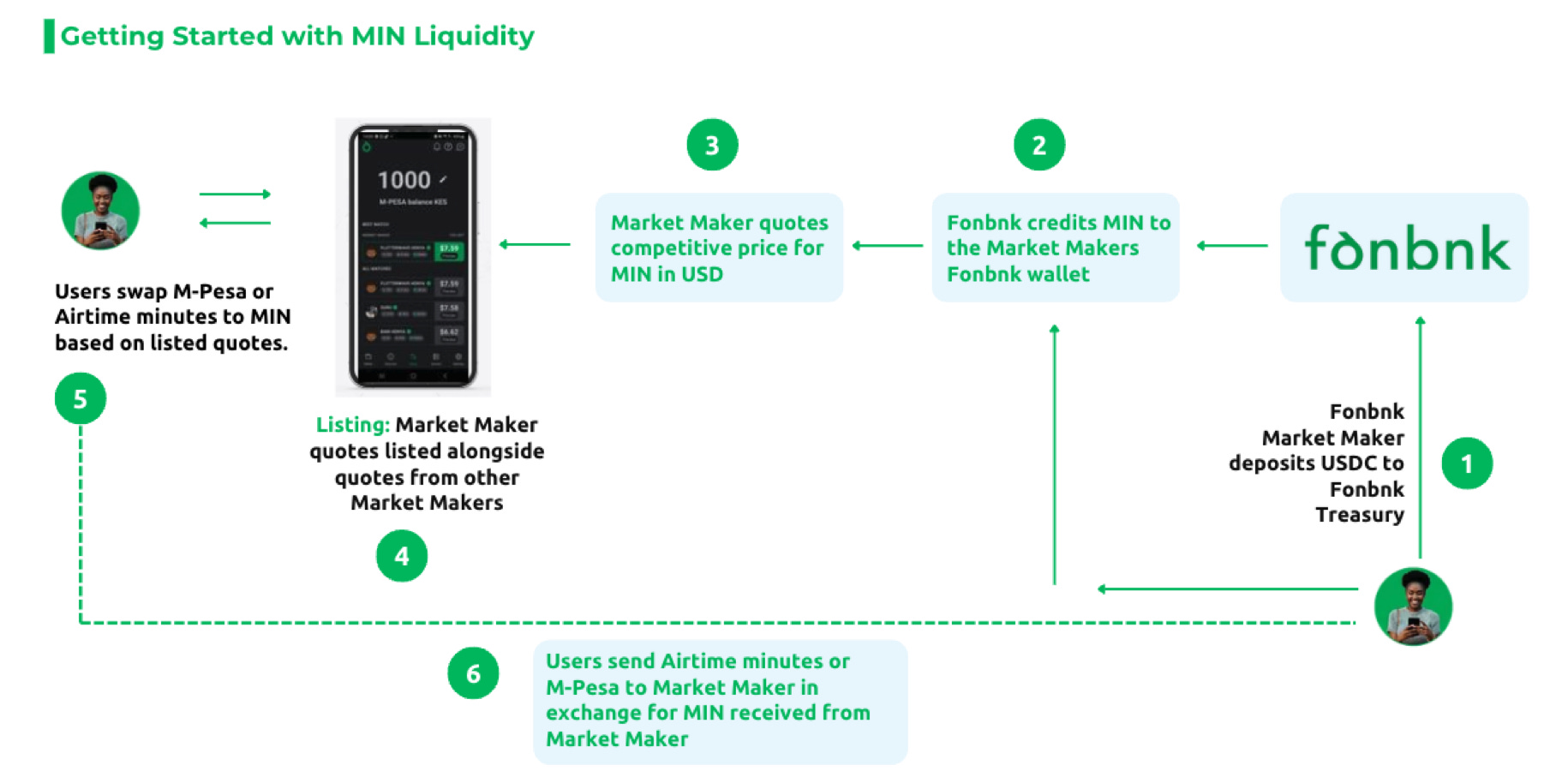

Liquidity for M-Pesa / Airtime Minutes swaps to MIN:

Fonbnk Market Makers play a crucial role as liquidity providers within the ecosystem, facilitating the seamless conversion between airtime minutes or M-Pesa on one hand and MIN tokens on the other. Each Market Maker maintains a MIN liquidity pool within the Fonbnk App, ensuring the availability of MIN tokens for users looking to exchange their airtime or M-Pesa for MIN. These market makers are a blend of automated market makers, airtime vendors, local businesses, crypto exchanges, payment service providers, and money service operators.

To become a Market Maker and contribute to the liquidity pool, individuals need to meet the following requirements:

Have a Valid Phone Number or Mobile Money Account:

Market Makers must possess a valid phone number capable of holding airtime minutes from supported telcos (e.g. MTN, Vodafone, Safaricom etc.) or a mobile money account with the ability to hold and transfer funds using prevalent mobile payment methods like M-Pesa in their region. This ensures they have the necessary channels to receive payments from users

Supported Wallet Address by Fonbnk:

Additionally, Market Makers need to have a wallet address supported by Fonbnk for receiving MIN tokens. Fonbnk supports over 100 wallets, including popular options such as Bitpay, Metamask, Coinbase Web3 Wallet, Trust Wallet, Electrum Wallet, among others. This compatibility ensures smooth transactions and accessibility for both Market Makers and users.

Market Makers Deposit USDC

Market Makers initiate the process by depositing USDC from their supported wallets (such as Bitpay, Metamask, Coinbase Web3 Wallet, Trust Wallet, Electrum Wallet, among others) into the Fonbnk treasury. This action mints MIN, which is credited to the Market Maker Fonbnk App account.

Fonbnk Credits MIN

Upon receiving the USDC deposit, Fonbnk credits the corresponding amount of MIN tokens to the Market Maker's Fonbnk account. 3. Market Maker Sets Quotes: The Market Makers then set their quotes to be listed on the Fonbnk exchange. They are at liberty to independently establish their spreads, resulting in varying quoted rates among different liquidity providers. 4. A User seeking to on-ramp from KES to a stablecoin is then presented with multiple competitive quotes from different Market Makers as illustrated in the screenshot below.5. Transaction Execution: Upon selecting a preferred quote, the user proceeds to execute the transaction. This entails the user releasing airtime minutes or M-Pesa to the chosen Market Maker, who then releases MIN tokens to the user's account.

In terms of profits and spread, margins generated by the liquidity providers potentially exceed 1%. Despite such lucrative margins, these liquidity providers manage to remain competitive against traditional USD exchange desks in shopping malls, banks, payment networks, and other financial entities. This setup empowers users and exposes them to more favorable dollar rates.

The table below offers a snapshot of the competitive quotes provided by Fonbnk market makers in comparison to the USD forex rates offered by local banks.

Two primary types of liquidity providers exist within Fonbnk's ecosystem: P2P liquidity providers and institutional liquidity providers. P2P providers specialize in supporting micro-transactions, requiring a minimum liquidity of $10 and facilitating transactions starting from as low as one MIN ($0.01).

On the other hand, institutional providers made up of players like Flutterwave, Kotani Pay and OTC service providers such as Bitmama have an unlimited liquidity ceiling and are capable of handling numerous small-scale transactions, with a maximum transaction limit of $200 per wallet per day.

Fonbnk opted to remain under a $200 maximum transaction limit to adhere to regulatory thresholds, particularly FinCEN's de minimis threshold of $2000. By ensuring transaction limits stay below this threshold, Fonbnk has aligned itself with the "closed-loop exemption" concerning prepaid airtime marketplace dynamics, akin to gift card exchanges. This framework ensures a limited U.S. nexus, streamlining operations and reducing regulatory complexities. with reduced regulatory obligations and effectively manage compliance risks.

The $200 maximum transaction limit per wallet per day may be high or low depending on the context. i.e. It may seem low compared to other existing liquidity provision deals offered by other DeFi platforms. Further, it is still on the lower end of transaction limits even within the M-Pesa ecosystem, for instance, M-Pesa's maximum transactions per person per day can reach up to KES 500,000 ($3,800).

However, in terms of trading volume, there is a significant number of small-scale transactions that occur particularly among lower-income segments of the population. For many locals, $200 per person per day may be sufficient for a full month's financial transactions, including payments for goods and services, remittances, and bill payments.

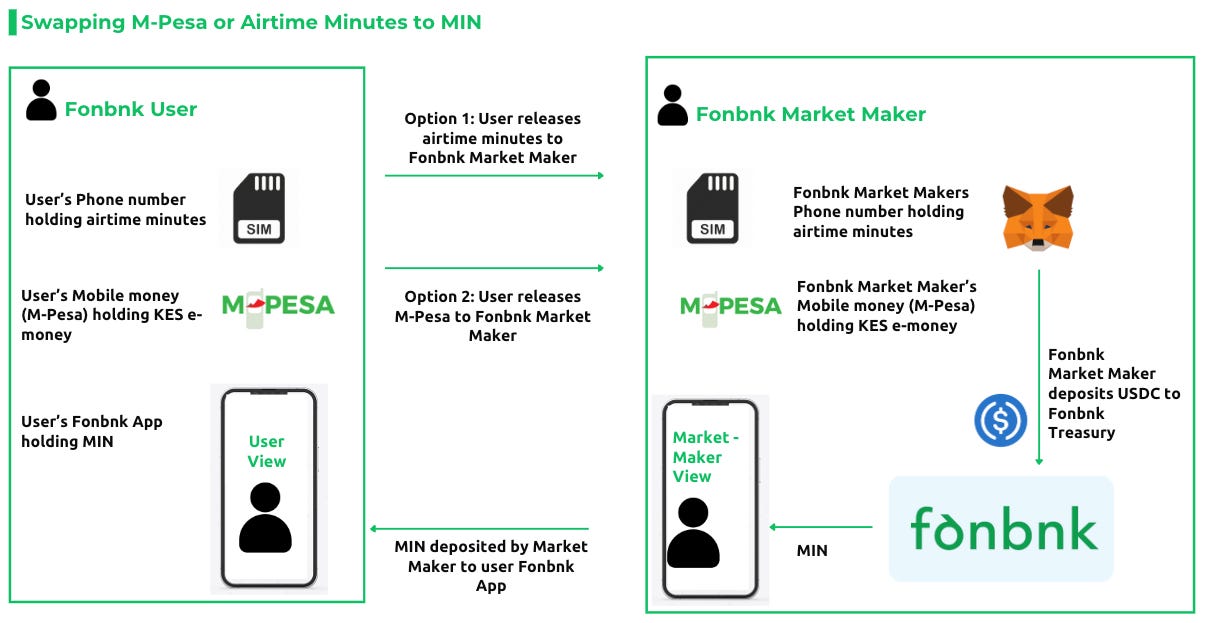

Swapping M-Pesa and Airtime Minutes to MIN

To get started, Fonbnk users need either of (i) a valid phone number that can hold airtime minutes from supported telcos, or (ii) a mobile money account with the capability to hold and transfer funds using prevalent mobile payment methods in their region (e.g M-Pesa).

The process starts with accessing Fonbnk's mobile widget, which is seamlessly integrated into various global partner wallets. From there, users can choose their preferred exchange medium, airtime, mobile money, or bank transfer, and initiate the transfer to their wallet.

Behind the scenes, Fonbnk's marketplace algorithm takes over. It matches users with leading liquidity providers in their region, ensuring that they get the best possible price, liquidity, and availability for their transactions. This sophisticated algorithm is the backbone of Fonbnk's platform, enabling seamless and efficient exchanges that cater to the unique needs of each user.

Based on the matching within the app, users may then exercise either of the following two options in the purchase of MIN from the matched Liquidity Provider:

Option 1: Swapping Airtime Minutes to MIN

Users also have the option of swapping Airtime Minutes to MIN by sending airtime minutes from their phone numbers to the phone number associated with the matched LPs. Upon receipt of the airtime minutes, the LPs credit MIN to the user's Fonbnk account. This transaction effectively reduces the LPs' MIN balance but increases their airtime minutes on the respective mobile number associated with their LP account.

Option 2: Swapping M-Pesa to MIN

Users have the option to swap M-Pesa to MIN. This is initiated by the user who sends e-money via M-Pesa from their phone numbers to the phone number associated with the matched Market Maker. The Market Maker then releases MIN to the user's Fonbnk account.

Given that MIN is a ledger entry of USDC (1MIN = $0.01), the value of the MIN received by users is at the prevailing exchange rate between the local currency (e.g. KES) and USDC. Fonbnk imposes a 1% charge on liquidity providers for initiating a swap on the Fonbnk app.Converting MIN to USDC

By following the steps in the illustration above, users can seamlessly swap their MIN tokens for stablecoins (USDC) within the Fonbnk app. The key steps are as follows:

User Initiates Swaps: This step begins when the user decides they want to exchange their MIN tokens held within the Fonbnk app for stablecoins (USDC).

Select Stablecoin and Network: After initiating the swap, the user is prompted to select the stablecoin they wish to receive, such as Circle’s USDC, Tether’s USDT, or Celo’s cUSD.

Select Network: In step 2, users select the blockchain network on which they want to receive the stablecoins. Supported networks include Polygon, Celo, Stellar Network, Algorand, Solana, TRON, Avalanche, Base, Optimism, Near, and Ethereum. Users are further prompted to insert the wallet address where they want to receive the stablecoin.

Initiate Transaction: With all details confirmed, the user initiates the swap transaction within the Fonbnk app. This action signals Fonbnk to proceed with the exchange process. Fonbnk executes the transaction by debiting the corresponding amount of MIN from the user’s Fonbnk app balance and credits the equivalent amount of the selected stablecoin to the user's designated wallet address. This ensures that the user receives the stablecoins they requested in exchange for their MIN tokens.

The USDC credited to the user’s selected address is released from Fonbnk’s treasury. This treasury serves as a pool of USDC reserves held by Fonbnk to facilitate transactions and provide liquidity for user exchanges. The user thus receives the stablecoins they requested in exchange for their MIN tokens.

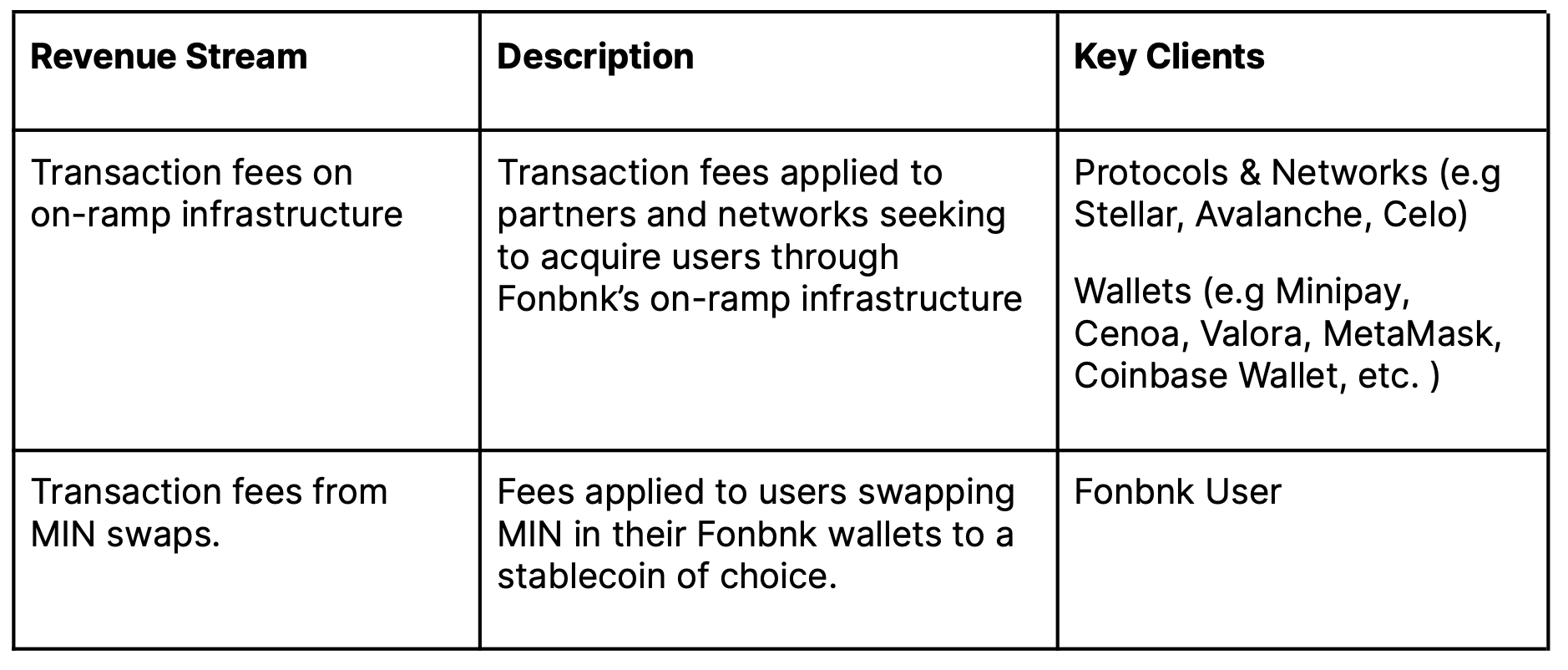

Revenue Model & Fees

As the company prepares to scale up, it is actively engaging in initiatives to attract institutional USDC and USDT liquidity providers. The aim is to establish partnerships with entities or individuals that can contribute USDC and USDT liquidity to further enhance and expand the liquidity pool within Fonbnk, ultimately providing a more efficient and seamless experience for the millions of users that would be engaging in airtime swaps and other transactions on the platform.

For example, a partnership with the mobile web browser Opera Mini (with 2.2m users in the region) aims to bolster Fonbnk adoption as an on-ramp provider. These types of partnerships could drive demand for larger USDC/USDT liquidity providers (LPs) on Fonbnk, which is the bottleneck for growth as more users join.

According to Fonbnk, the company's value proposition centers around its unique ability to aggregate dollar liquidity across the continent, creating opportunities for liquidity providers (LPs) through short-term, high-spread, high-volume use cases.

By bringing in external liquidity providers, Fonbnk aims to strengthen its position and increase the depth of the market, which can lead to improved market efficiency and better pricing for users participating in the Fonbnk Distributed Exchange.

Challenges for Fonbnk

While there is much to like about Fonbnk’s novel approach to bringing underbanked users into Web3, Fonbnk also faces a number of headwinds that it must navigate. These are as follows:

Dependence on crypto-wary telcos that have a low risk appetite for crypto-based services may result in operational challenges and unpredictable shutdowns for Fonbnk's platform.

Fonbnk's model relies heavily on existing telecommunication infrastructure. Using these established networks, users can exchange either airtime minutes or mobile money with Market Makers. This exchange is facilitated by sending the corresponding value to the Market Maker's mobile number. In return, MIN tokens are deposited directly into the user's account within the Fonbnk platform.

The risk of reliance on telco infrastructure is that crypto-based services have historically faced skepticism and strong opposition from local mobile money operators in Africa, many of whom operate as both telcos and mobile money operators. Instances of arbitrary shutdowns of APIs and mobile money paybill accounts have severely limited the potential of crypto-based services, leading to frustration for these ventures.

Take for example, the case of Kipochi in February 2013. Kipochi aimed to challenge locally operated mobile money operators, such as M-Pesa, by leveraging Bitcoin and ensuring interoperability with various vendors. The strategic approach involved forming partnerships with telcos in the region, intending to create a consumer wallet based on USSD and mobile web technologies. The goal was to brand this wallet in collaboration with local operators, providing a decentralized and versatile mobile money solution.

However, the venture faced a significant setback within a remarkably short timeframe. Approximately a week after establishing a connection with M-Pesa through the merchant provider Kopo Kopo, the project was abruptly shutdown and it took the project team over a week to uncover the reason. Eventually, it was revealed that Safaricom, possibly acting under the influence of Vodafone in London, had compelled Kopo Kopo to terminate the collaboration with Kipochi.

Fonbnk addresses this risk by decentralizing the on-ramp process. Unlike its counterparts, Fonbnk refrains from establishing APIs or accounts with existing telcos. Instead, it adopts an escrow pathway where users autonomously transfer airtime minutes or M-Pesa directly to Market Makers. This decentralized approach shields Fonbnk from the arbitrary shutdowns of APIs that other players encounter, bolstering its resilience and sustainability within the market.

While Fonbnk has not experienced such aggressive action thus far, there is a potential risk in the event of a mass scale-up. Arbitrary actions, similar to those faced by other crypto-based services, can pose a significant threat to the scalability of Fonbnk's business. Such actions have the potential to disrupt the seamless operation of cryptocurrency-based services, impeding the achievement of Fonbnk's goals in providing alternative financial solutions. This underscores the importance of proactively addressing potential regulatory and operational challenges to ensure the sustained growth and stability of the platform.

Fonbnk on-ramp solution is subject to increasing competition from other platforms with similar value propositions.

The burgeoning expansion of new wallets in Africa has sparked a growing demand for reliable on-ramps facilitating the conversion of local currency to stablecoins. Multiple market players are entering to meet this demand. However, Fonbnk's current swap limitation of $200 per wallet per day could potentially discourage high-volume Market Makers from participating, given the capped earning potential.

In addition to facing the limitations above, Fonbnk further encounters limitations related to airtime swaps and M-Pesa transactions. For airtime swaps, users are constrained to send amounts ranging from Ksh. 5 to Ksh. 10,000, limiting the maximum value of a Fonbnk swap to Ksh. 10,000 per airtime transaction. Similarly, M-Pesa imposes restrictions such as, a maximum daily transaction value of Ksh. 500,000, and a maximum amount per transaction of Ksh. 250,000 on its users.

These restrictions presents several challenges for Fonbnk:(1) Reduced Market Engagement: High-volume Market Makers might hesitate to engage with Fonbnk due to the restricted transaction size. This could lead to diminished liquidity and fewer competitive quotes, ultimately impacting users seeking efficient transactions. (2) Limited User Flexibility: The transaction limit on Fonbnk may impede users requiring larger conversions of local currency to stablecoins. This constraint could result in user frustration and dissatisfaction, particularly among those with substantial transaction needs.

Below is an analysis of other on-ramp providers in Africa:

Highly evolving regulatory landscape within the DeFi and Crypto landscape.

The uncertain regulatory landscape surrounding cryptocurrency, stablecoins, and decentralized finance (DeFi) poses a significant risk to Fonbnk's operations. With regulations in flux, there is uncertainty about how Fonbnk's activities may be interpreted or scrutinized by governmental bodies. While countries like South Africa, Botswana, Namibia, and Mauritius have implemented laws requiring licenses for crypto-related services, Fonbnk is yet to obtain such licenses in these jurisdictions. This exposes Fonbnk to legal and operational risks, including potential legal challenges, disruptions in operations due to changing regulatory interpretations, and damage to the platform's reputation.

Conclusion

Stablecoin on-ramp platforms have strategically positioned themselves as key players in addressing the challenges of dollar scarcity in Africa as the demand for stablecoins as an alternative currency has surged.

With over 50 million African consumers relying on mobile money for daily financial transactions, pivoting towards on- and off-ramp solutions layered on mobile money is a crucial bridge for merchants to access the stablecoin market, empowering them to navigate economic uncertainties with stability and security.

As the adoption of stablecoins continues to grow across the continent, the role of on-ramp service providers as facilitators for access to digital dollars for local businesses and consumers underscores their importance in driving financial inclusion and innovation in the African market.