DeFi Markets Update 2026-06-10

Apyx Depeg, Token Terminal’s Analysis of Steakhouse Fi, What Basin changes for tokenised Treasuries

Welcome to another DeFi Markets Update—your no-nonsense briefing on the cryptobanking plumbing and market pulse.

Apyx Depeg with STRC price’s fall triggers Morpho Liquidations

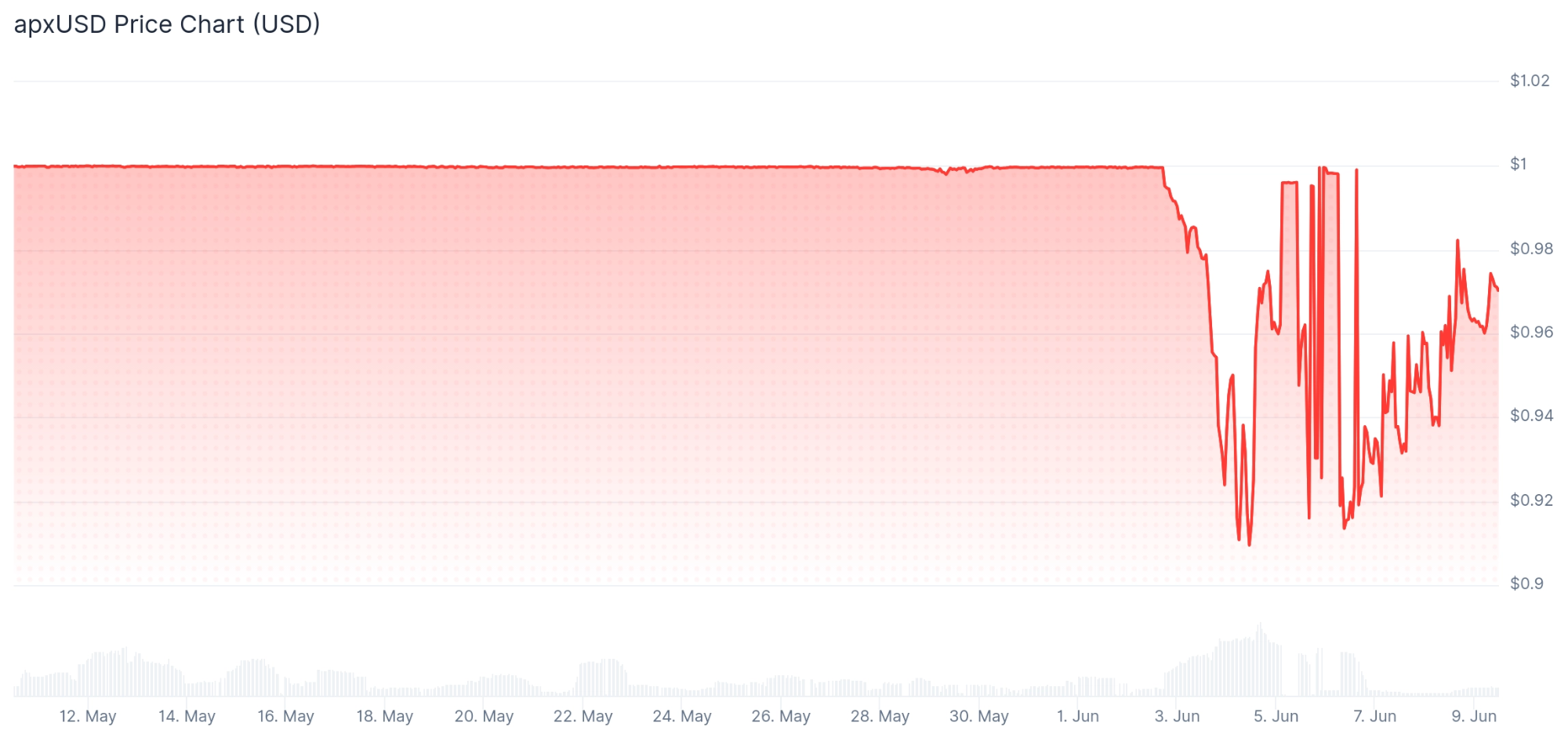

Last week, apxUSD, Apyx’s STRC-backed stablecoin, saw its largest depeg to date, declining to $0.909. According to Apyx’s post-mortem, this happened as BTC fell, triggering retail panic and causing Strategy’s perpetual preferred stock STRC, the main asset backing apxUSD, to fall from near its $100 par value to $90.38.

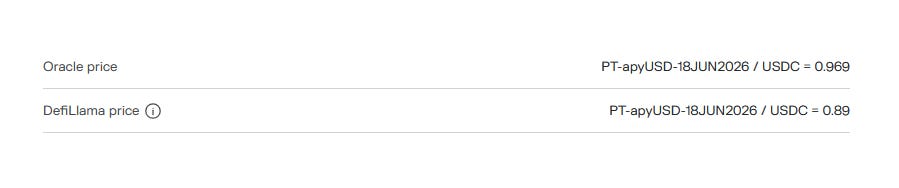

The event was notable for the divergence between Morpho market oracle prices and apxUSD secondary-market prices. The affected oracles used an exchange-rate-based NAV intended to reflect the fair net asset value of the product’s backing assets. As apxUSD depegged, the market price adjusted more quickly than the NAV-based oracle price, creating a gap between market and oracle valuations. The slower decrease in the NAV exchange rate led to liquidations being triggered in a mechanically ordered sequence.

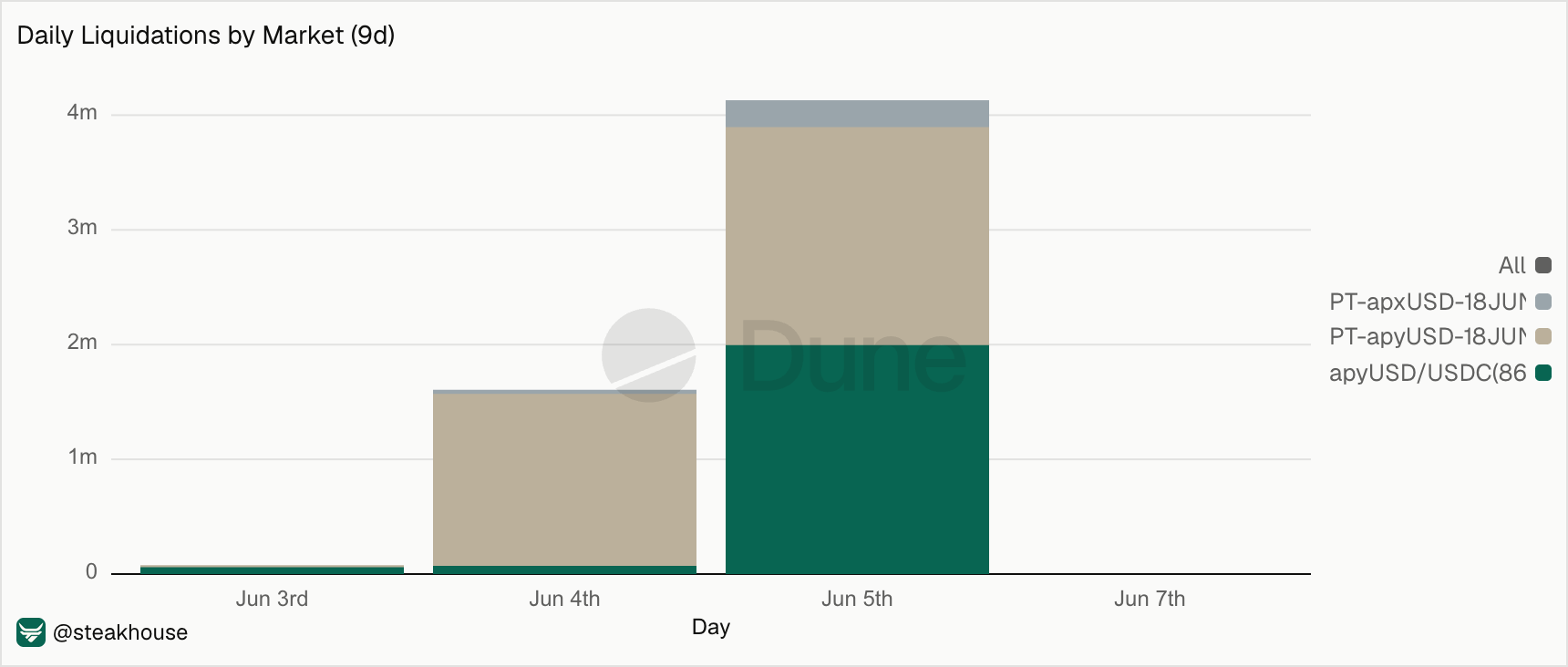

The Apyx USDC vault was affected through its Morpho allocations. The vault lends USDC into Apyx-related markets, including apyUSD/USDC and the Pendle PT-apxUSD/USDC markets. As apxUSD and related assets repriced during the depeg, leveraged borrower positions breached liquidation thresholds, leading to a rise in liquidations across those markets.

The depeg began around June 3 and peaked on June 5, when liquidations across these Morpho markets exceeded $4m in a single day.

The event did not cause any bad debt, and liquidations were handled orderly. The impact stayed contained within the Apyx vault and its related Morpho markets.

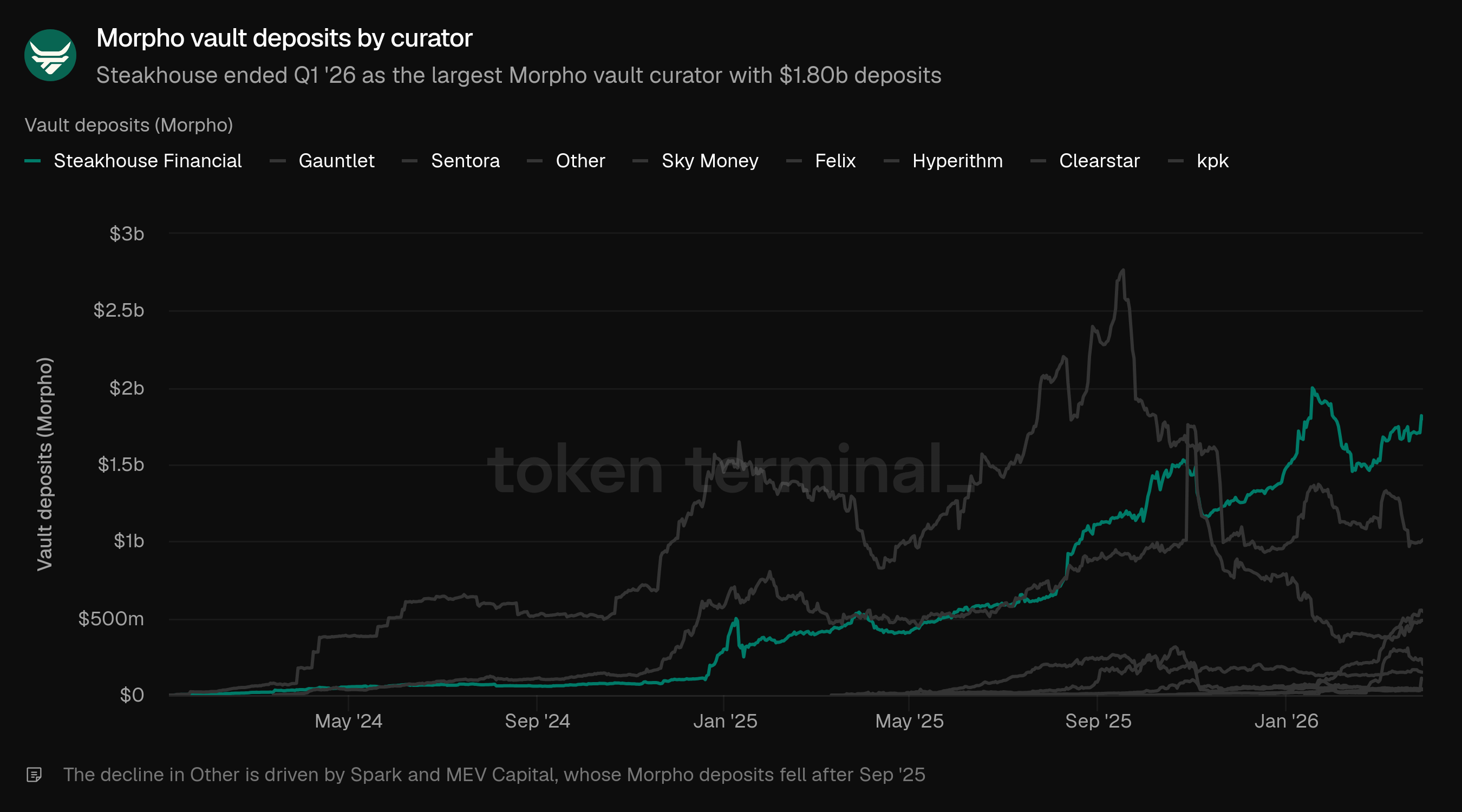

Token Terminal’s Analysis of Steakhouse Financial

Last week, Token Terminal published its Q1 2026 analysis of Steakhouse Financial, which we recommend reading in full. Below is a short summary.

According to the report, we ended Q1 as the largest curator on Morpho, with Morpho deposits increasing 9% QoQ from $1.64bn to $1.79bn.

Morpho Vault Curation accounted for 94.42% of Steakhouse TVL in Q1, up from 90.79% in Q4, while Kamino Vault Curation fell from 9.21% to 5.58%.

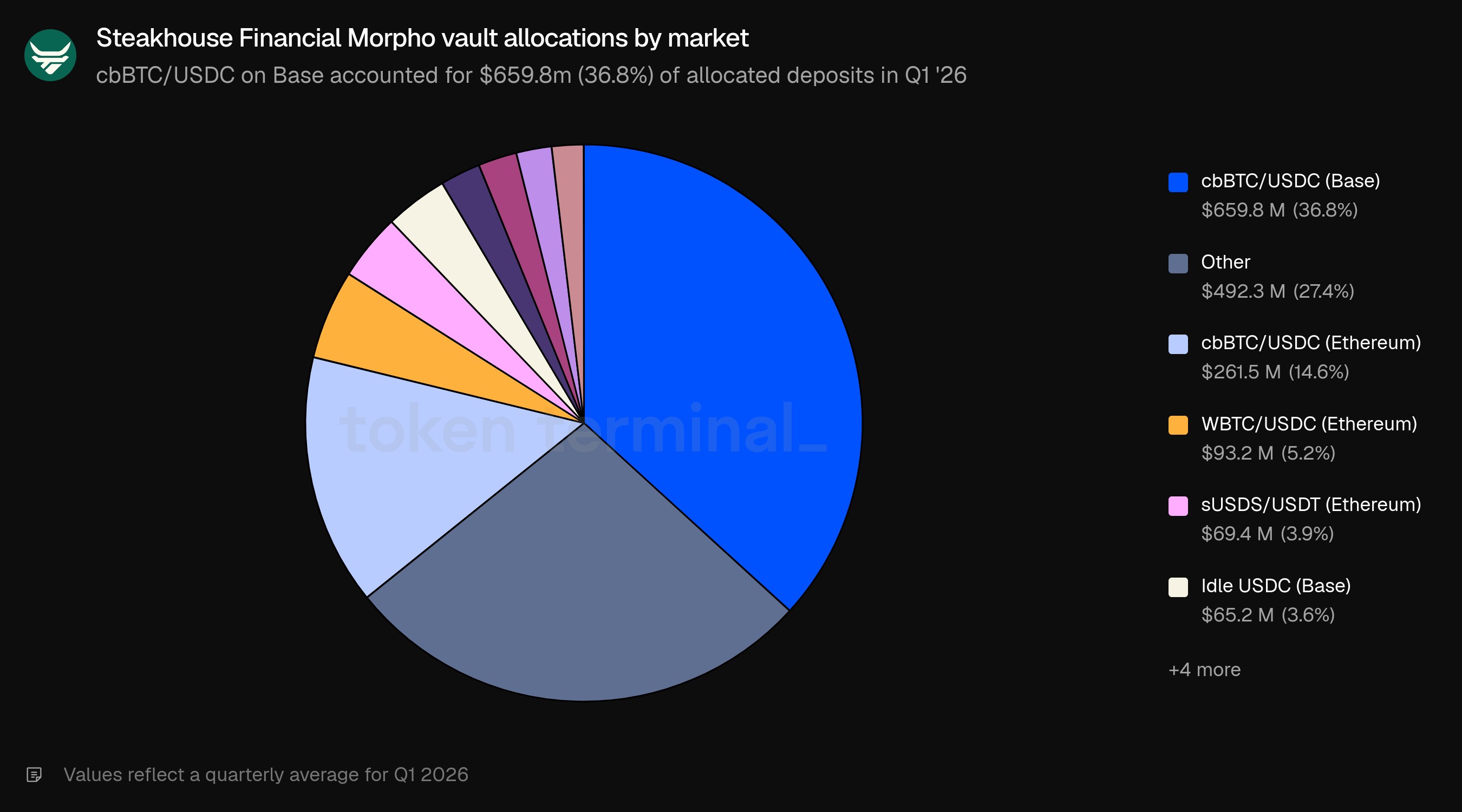

Q1 took place during a period of lower lending activity across DeFi. Aggregate lending TVL averaged $82.5bn during the quarter, down 18.2% QoQ but still up 44.8% YoY, while our curator deposits continued to grow. During the Feb/March volatility, markets where our vaults were exposed processed $234m of liquidations while maintaining full redeemability across nearly $1.7bn in deposits.

Steakhouse vaults Q1 allocation mix was concentrated in stablecoin lending against liquid collateral. BTC-backed USDC markets accounted for more than 56% of allocations, with cbBTC/USDC on Base as the largest destination. This is consistent with our conservative curation approach focused on collateral quality, liquidity, and risk-adjusted demand.

In Q2 so far, we continue to be the largest curator on Morpho with around $1.7bn in deposits and approximately 2x the TVL of the next largest curator. Much more Steak to come in Q3, with more updates soon!

What Basin changes for tokenised Treasuries

Grove’s Basin has been announced almost a month ago with up to $1bn in committed daily liquidity for tokenised RWAs. The product focuses on reducing the settlement friction associated with Treasury-backed assets by enabling instant access to USDC.

Centrifuge recently published an article on JTRSY, the Janus Henderson Anemoy Treasury Fund, which will support instant 24/7 redemption into USDC via Basin once it launches. The article focuses on how this changes the utility of tokenised Treasuries across onchain markets.

Historically, Treasury products have typically operated with T+1 redemption timelines, creating a tradeoff between earning Treasury yield and keeping USDC immediately available. With Basin, JTRSY can keep short-duration Treasury exposure while giving holders access to USDC when liquidity is required.

The article points to three areas where this becomes most relevant: stablecoin reserves, treasury management and lending collateral. In each case, the value comes from making Treasury-backed assets more operationally useful inside onchain systems.

In practise, for treasuries and allocators, Basin changes how idle capital can be managed. A DAO treasury can hold part of its idle USDC in tokenised Treasury exposure, keep earning yield, and move back into USDC when capital is needed for incentives, investments or expenses.