DeFi Markets Update 2026-05-26

EURCV on Morpho, USDG Borrow Activity on Kamino, SOFR as the Base Layer For Stablecoin Yields

Welcome to another DeFi Markets Update—your no-nonsense briefing on the cryptobanking plumbing and market pulse.

EURCV Adoption Across Morpho

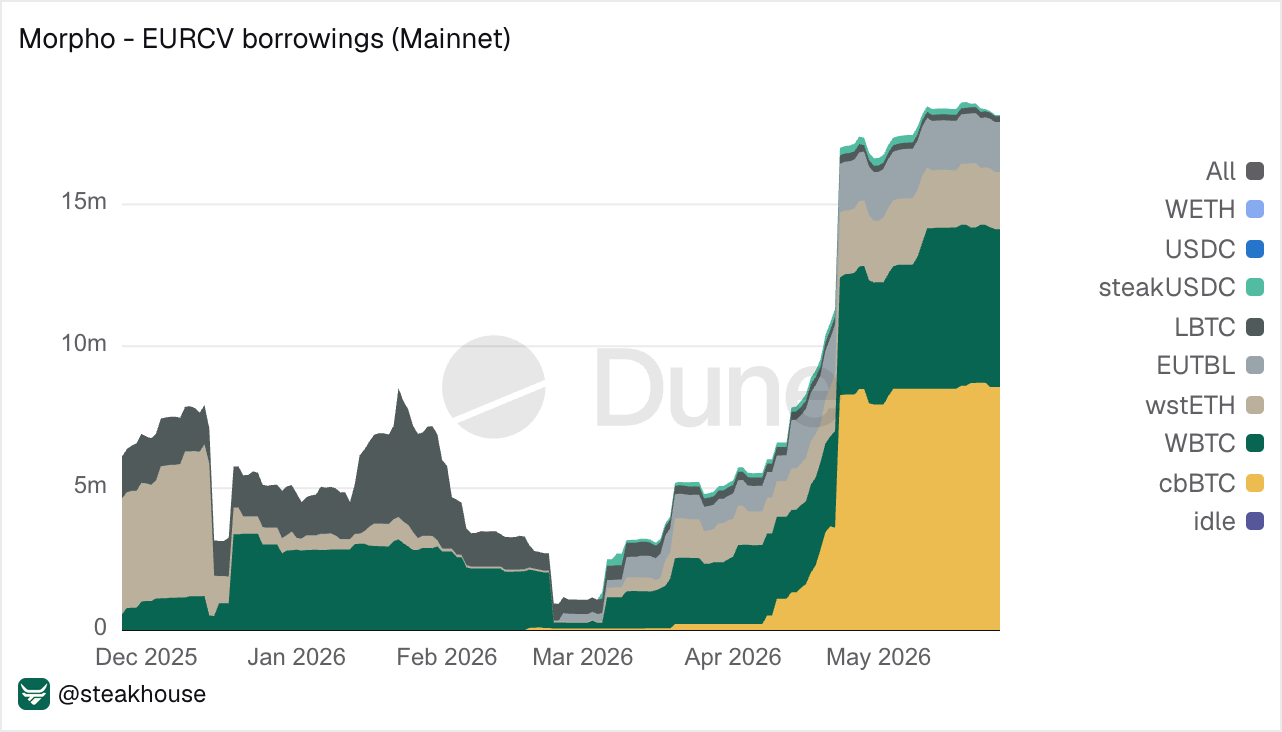

EURCV borrowings on Morpho Mainnet have grown by more than 3x since January 2026, driven largely by cbBTC collateral usage, which expanded from near zero to nearly $9m in borrowings in the last 3 months.

One reason for this recent growth is the cheap EURCV borrowing available against cbBTC collateral on Morpho, with rates below 1% (same rates for all collaterals). Borrowed EURCV can then be deployed into Steakhouse Prime EURCV, which is currently yielding around 3–4%, creating a potential carry opportunity highlighted in one of our previous Markets Updates.

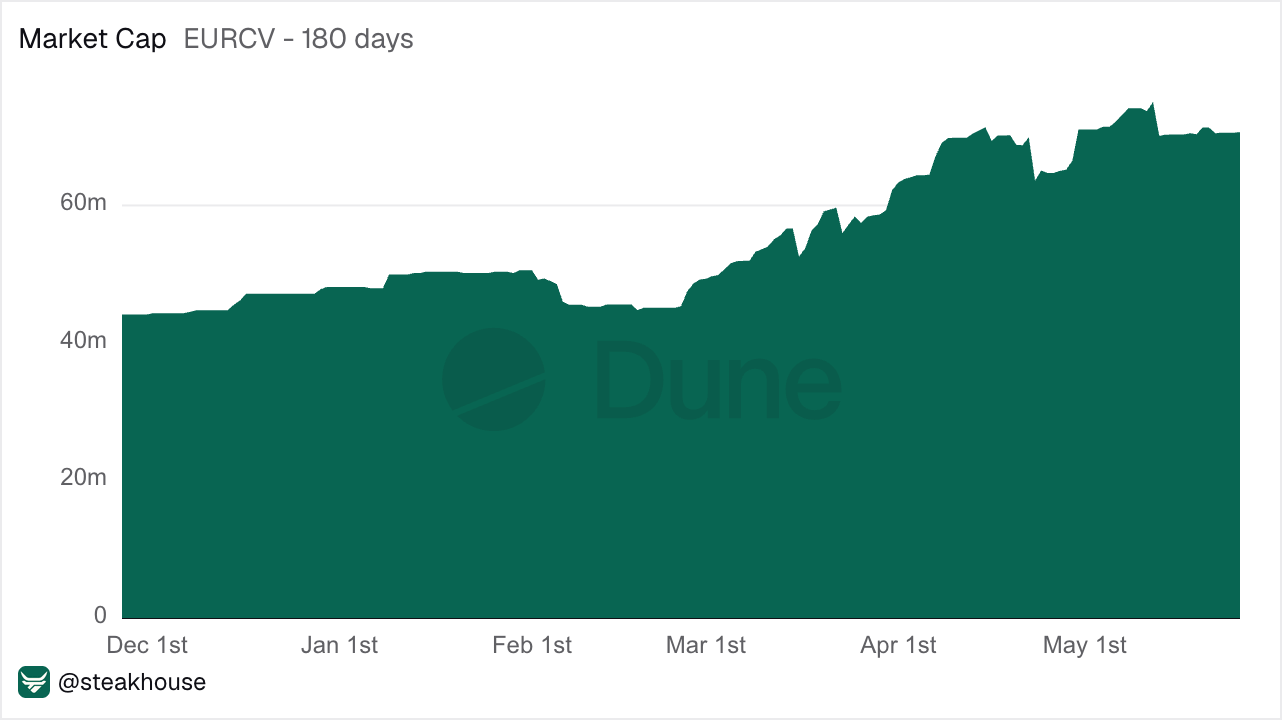

EURCV supply has also continued expanding in 2026, increasing from roughly €48m at the start of the year to over €75m in May, displaying the growing demand for euro-denominated stablecoin liquidity and euro borrowing markets onchain.

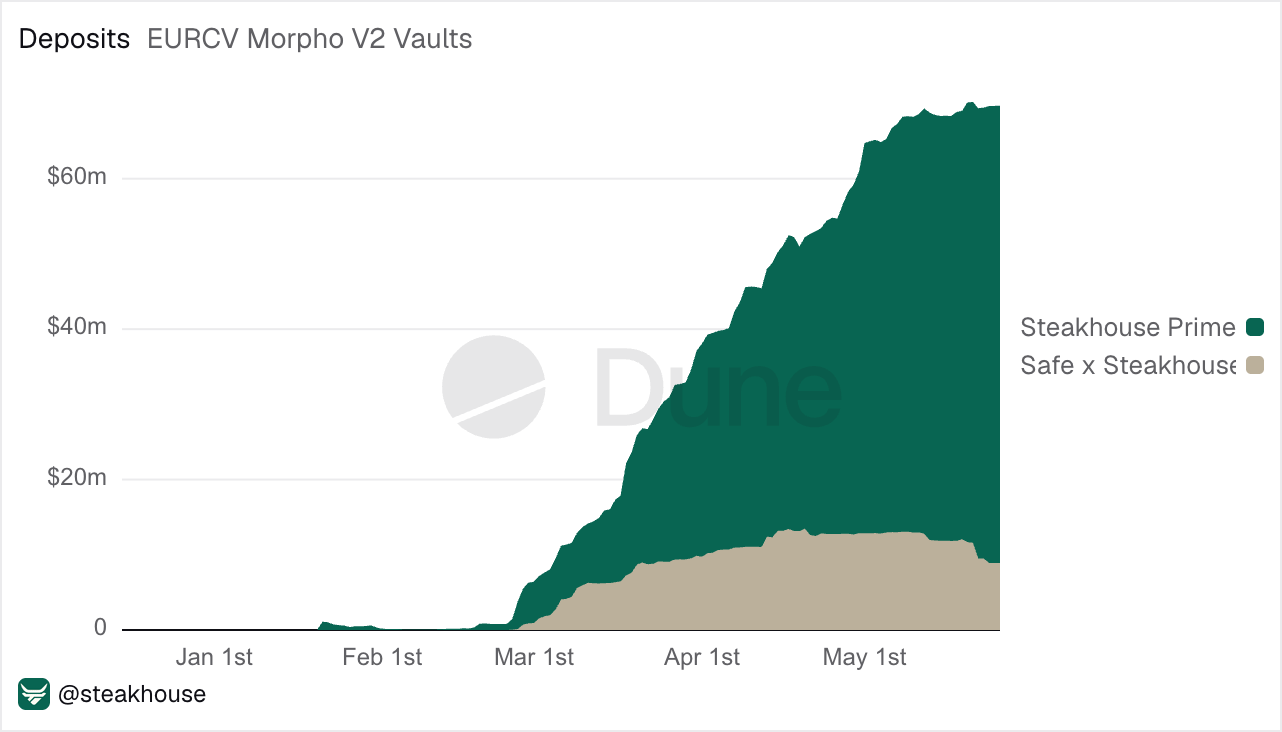

Moreover, Morpho V2 adoption has also continued expanding across Steakhouse EURCV vaults, with more than €30m deposited into V2 vaults since the start of March.

USDG Lending Rates and Borrow Activity on Kamino

Steakhouse USDG vaults on Kamino: Steakhouse USDG and Steakhouse USDG High Yield, are both now earning around 7% APY.

USDG is a dollar-backed stablecoin issued by Paxos through the Global Dollar Network, which expanded to Solana in 2025.

A key driver behind these elevated yields has been the launch of Kamino’s Ethena Market in mid-May 2026, built around leveraged USDe/USDG looping strategies.

The strategy allows users to deposit USDe, borrow USDG at rates around 2.5%, swap back into USDe and repeat the loop with leverage. This has driven strong borrow demand for USDG, pushing utilisation across USDG markets higher and increasing lending yields for USDG suppliers on Kamino.

SOFR as the Base Layer for Stablecoin Yields

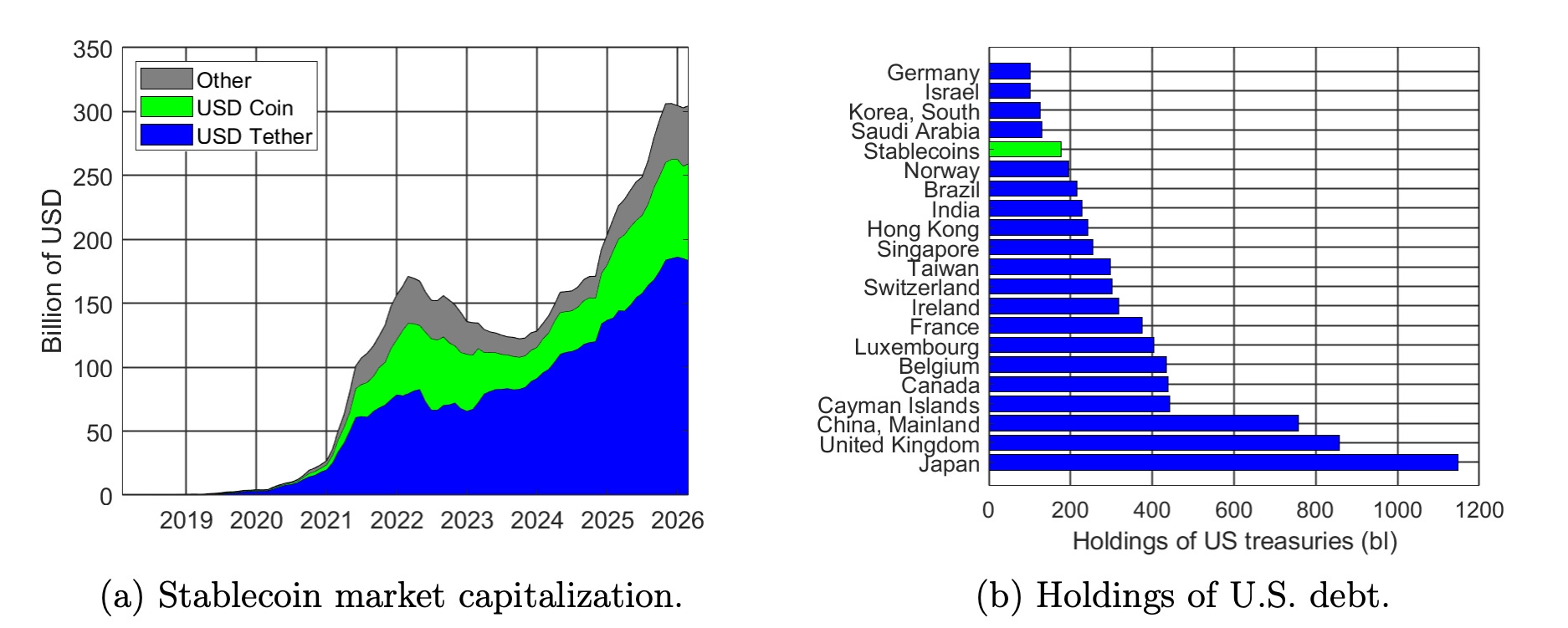

A recent paper, “U.S. Stablecoins and the Global Safe Asset Channel: Private Money Meets Public Debt”, by researchers from the European Central Bank and Politecnico di Milano explains how stablecoins are becoming increasingly connected to U.S. money markets through their reserve structures.

Stablecoin market capitalization has grown quickly over the last few years, with USDC and USDT now holding around $200bn across short-term U.S. government debt and repo-related assets.

As stablecoin supply grows, issuers need to hold more reserve assets. Since those reserves are mainly held in Treasury bills and repo, more stablecoin demand means more demand for U.S. safe assets. This creates a direct relationship between stablecoin markets and U.S. money markets. Because stablecoin reserves earn short-term dollar yields, onchain dollar lending should be priced from those same rates, making SOFR and Treasury yields the rate benchmark for onchain dollar liquidity.

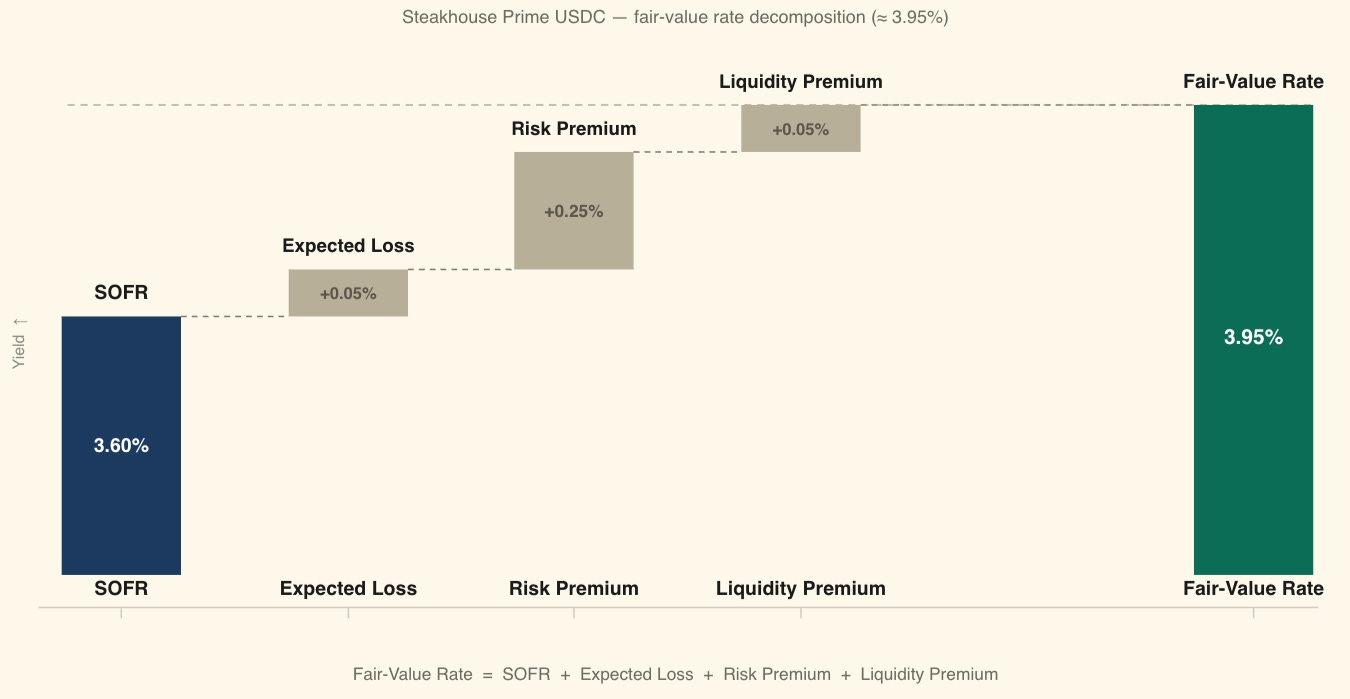

Recently, one of our co-founders at Steakhouse pointed out this dynamic when framing DeFi lending rates through a simple pricing model: yield = risk-free rate + expected loss + risk premium + liquidity premium. In this framework, SOFR acts as the starting point, while the spread above it reflects the additional risks of lending through onchain markets.

For example, we can see this in Steakhouse Prime USDC. Under the framework, the fair-value rate is around 3.95%: 3.6% SOFR + 0.05% expected loss + 0.25% risk premium + 0.05% liquidity premium (note these are illustrative values).

To conclude, stablecoin growth continues making onchain USD lending more connected to traditional money markets. Since USDC and USDT reserves sit largely in Treasury bills and repo, SOFR becomes the benchmark for lending rates.