DeFi Markets Update 2026-05-15

Steakhouse Growth, EtherFi New Markets, Are Stablecoins Stable?

Welcome to another DeFi Markets Update—your no-nonsense briefing on the cryptobanking plumbing and market pulse.

Steakhouse Continues to Grow After the Spring of Exploits

We all know Q1 2026 was a rough period for DeFi lending, with multiple collateral and lending incidents across the market. At Steakhouse, we are proud to say our vaults recorded less than $0.1 of bad debt across the period, while total deposits have continued growing.

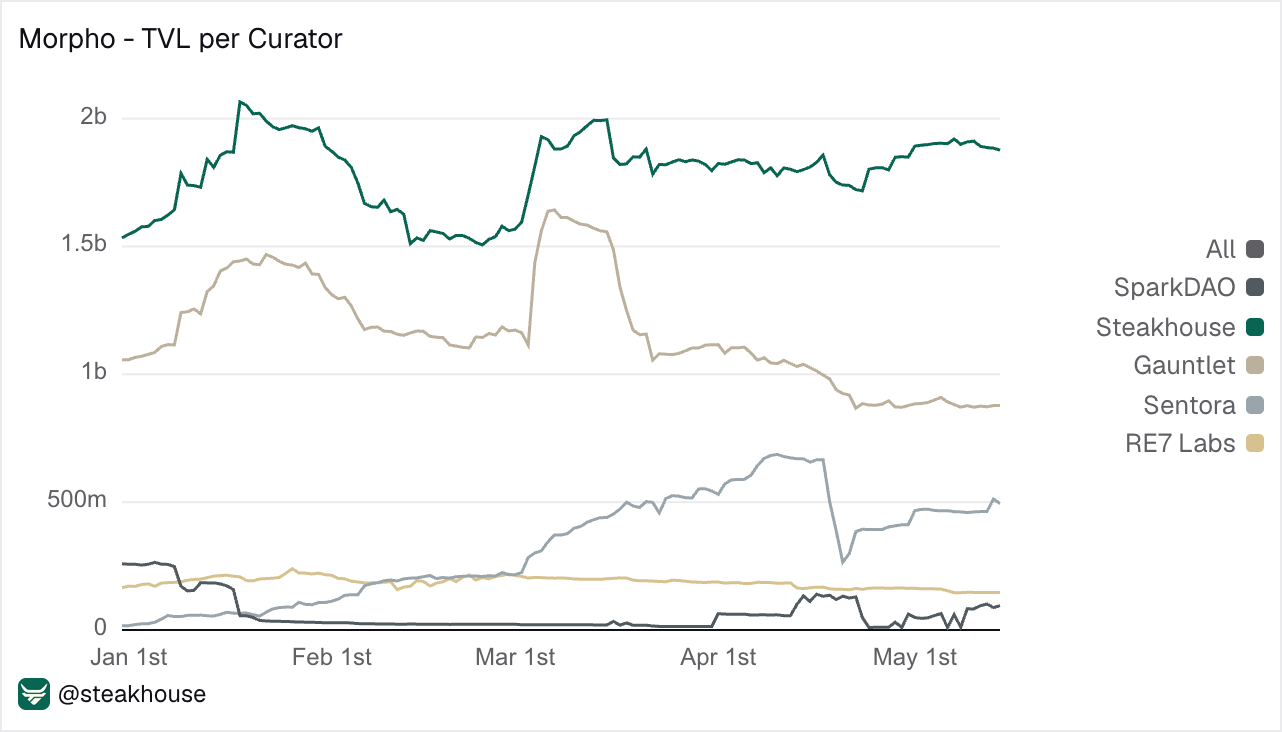

We are now the only curator managing more than $1B on Morpho and are steadily approaching $2B in total vault deposits.

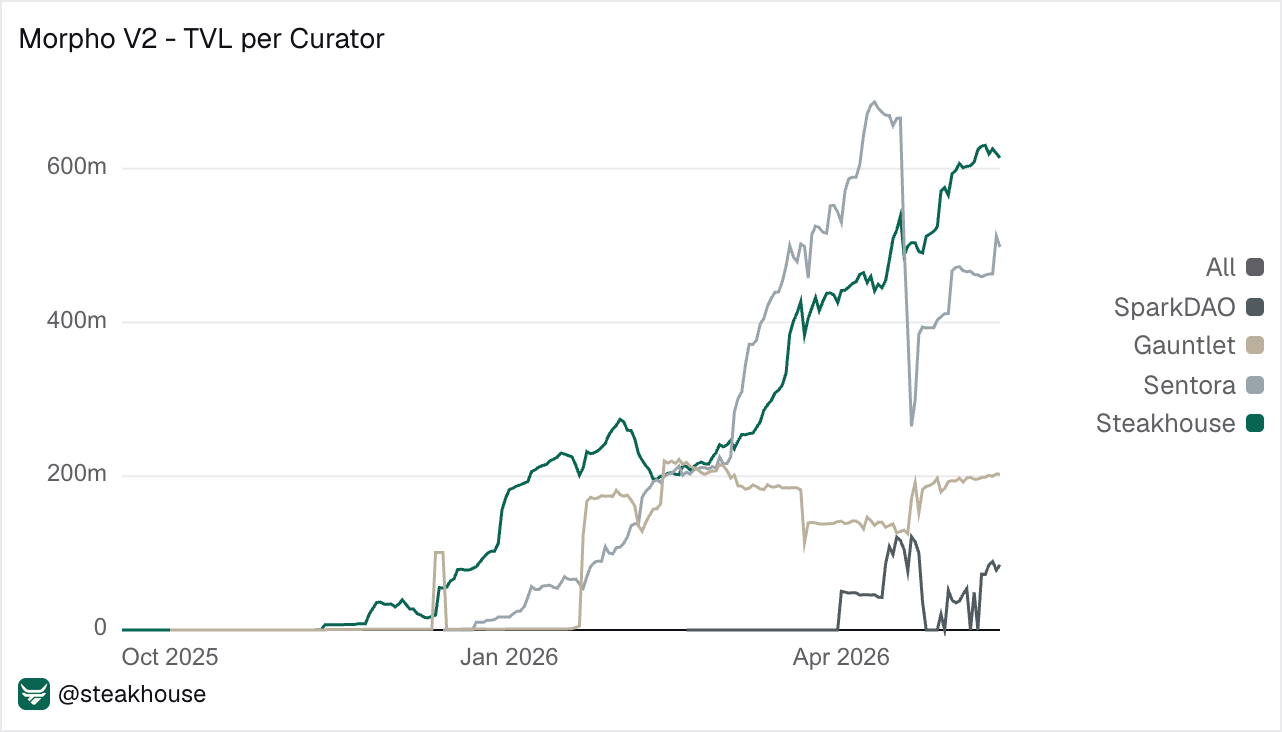

Morpho V2 adoption also continues to scale, with Steakhouse leading V2 vault TVL. Users with V1 positions can migrate into equivalent V2 vaults with similar risk-return profiles through the Steakhouse App, including Box Vaults for Term and Turbo strategies. [read more here]

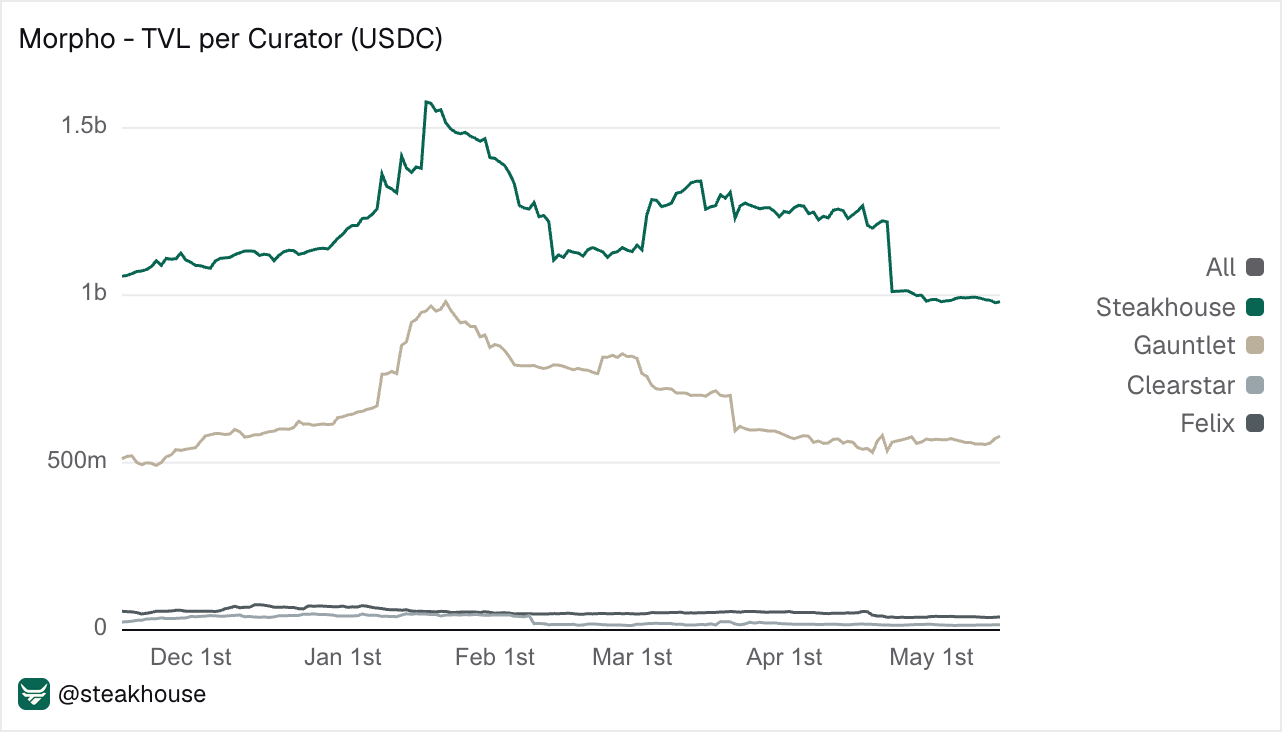

Steakhouse now curates around Two-Thirds of total USDC TVL on Morpho on all chains. Our Prime USDC vault on Base is also the largest vault on Morpho and was used as a benchmark in Morpho’s Q1 report.

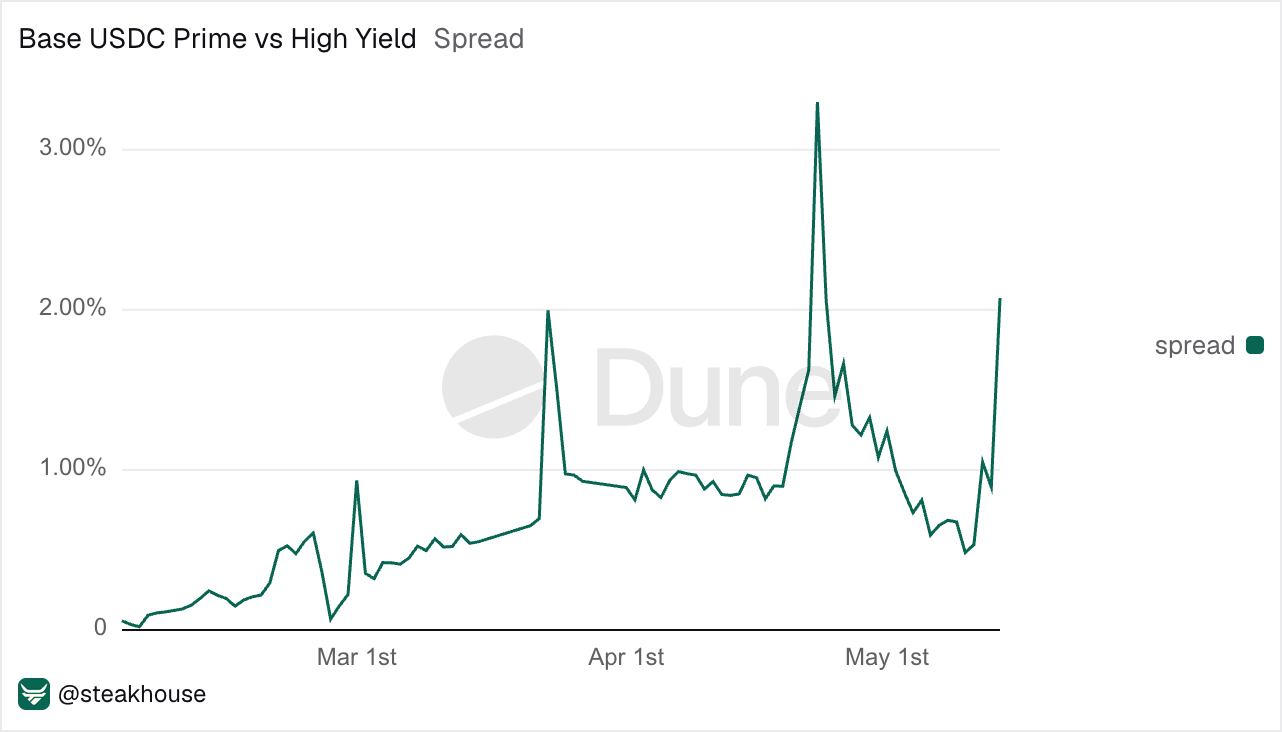

The spread between our Base Prime USDC and High Yield USDC vaults is widening again and is now above 2%. Prime continues to offer the more conservative USDC exposure, while High Yield rewards users willing to take on a broader collateral mix.

EtherFi: New Markets coming to Morpho

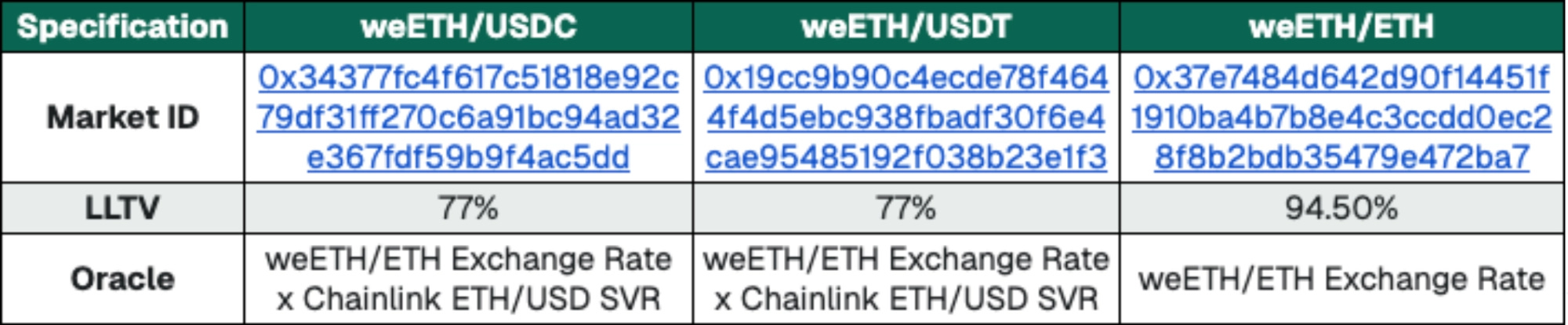

Steakhouse vaults are onboarding weETH from EtherFi as eligible collateral across both ETH and USD lending markets. This includes new weETH/USDC, weETH/USDT and weETH/ETH markets deployed using our meta oracle setup.

The review was benchmarked against both the internal Steakhouse risk framework and Lido’s wstETH architecture, which serves as the engineering baseline for Prime vaults. weETH was previously only eligible in Steakhouse High Yield vaults, but after the hardening process it now meets the threshold for Prime inclusion, positioning it as a more institutionally-grade collateral asset.

EtherFi strengthened governance by moving key powers behind longer timelocks, expanding multisigs with external signers, and reducing instant internal control over upgrades. Additionally, after the rsETH bridge exploit, EtherFi hardened its LayerZero setup by pinning message libraries and DVNs, requiring 4/4 DVN approval, and adding stricter rate limits to reduce exploit damage.

Before the new Prime markets went/go live, they entered a 7-day Steakhouse timelock period during which vault users could veto the onboarding through the Aragon DAO mechanism.

Are Stablecoins Actually Stable?

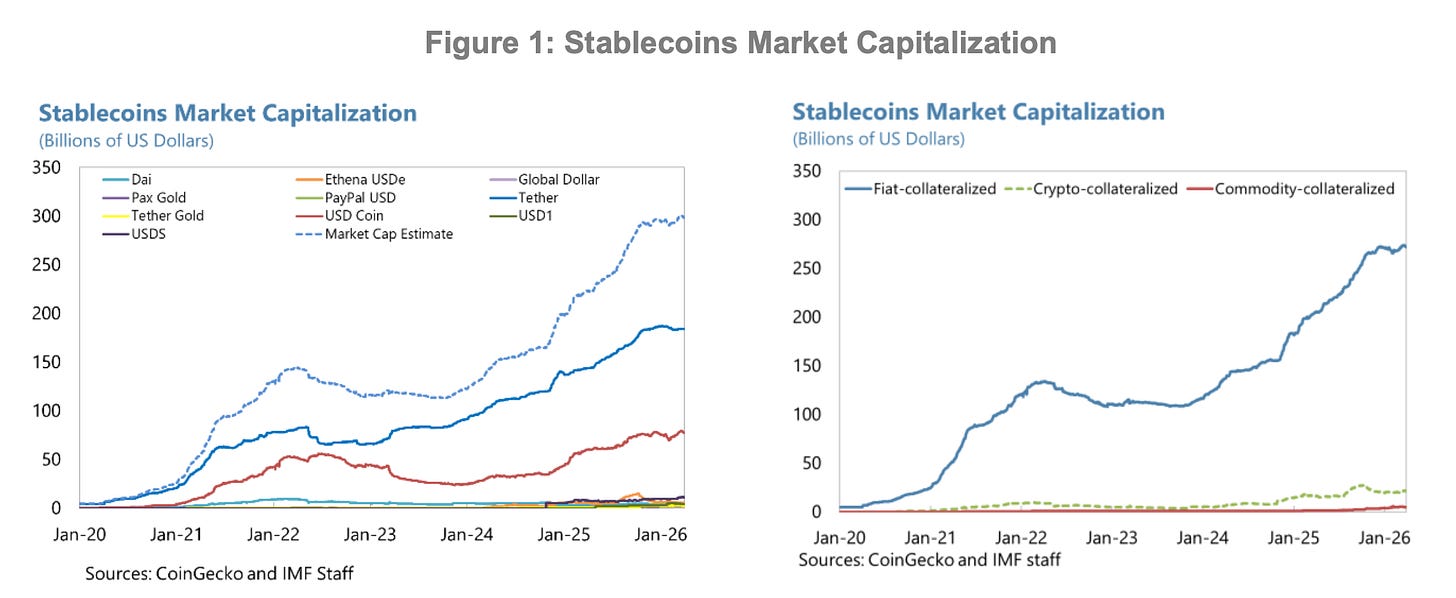

A new IMF paper, ‘Making Stablecoins Stable’, argues that stablecoin stability depends on the reserve structure behind the peg. Stablecoins have grown from a crypto-native settlement tool into a large dollar-denominated money layer, with most supply concentrated in fiat-backed assets and dominated by USDC and USDT. As stablecoins move further into payment regulation after the GENIUS Act, the key question becomes whether reserve structures can support 1:1 redemption during stress.

Stablecoins promise 1:1 redemption, while issuers back liabilities with assets carrying credit, liquidity or duration risk. The 2023 USDC depeg after Circle’s exposure to SVB showed that high-quality reserve structures can still face confidence shocks when part of the backing sits inside the banking system. The peg therefore depends on solvency, liquidity and market confidence during redemption stress.

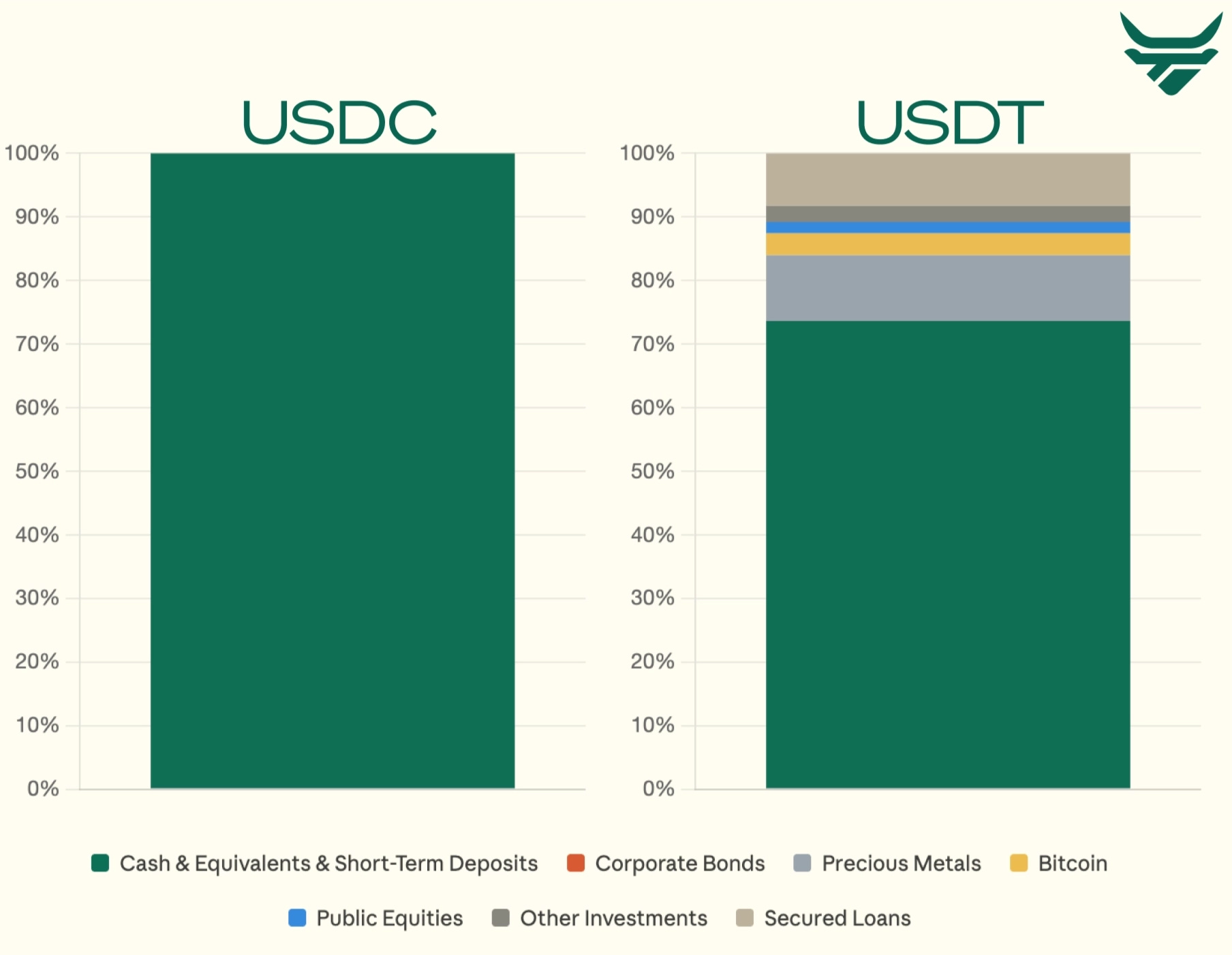

However this raises an obvious question: How relevant is this for today’s market, given that USDC has highly cash-like backing and USDT reports a large share of cash-equivalent reserves?

The authors use central bank money as the benchmark for stability: instant redemption at par, deep liquidity and no-questions-asked acceptance. In our view, this comparison is too narrow, as almost no one holds central bank money at scale. The more relevant comparison is with commercial banks, which are also regulated private entities issuing money-like instruments used across payments and savings.

Under that comparison, regulated stablecoins have a stronger structural argument. GENIUS and MiCA-style frameworks push issuers toward cash, short-term government debt and other highly liquid reserve assets. Banks, by contrast, issue money-like deposits against a broader and less liquid asset base. Therefore, regulated stablecoins may already have safer and more liquid reserve backing than traditional bank deposits, which challenges the paper’s framing of stablecoin stability.

The more interesting policy question is whether stablecoins are being held to a higher standard than the banking system they are compared against. Large issuers already show that highly liquid reserve structures can still be profitable at scale. Like USDT, which has built a significant excess reserve buffer, giving token holders an additional layer of protection before liabilities are impaired. The debate should therefore distinguish fully reserved payment money from fractional-reserve bank money as stablecoins move further into mainstream payments.