DeFi Markets Update 2026-04-14

Prime USDC Spread, Kamino Whitelisted Reserves, Stablecoins & Bank Deposits as Substitutes

Welcome to another DeFi Markets Update—your no-nonsense briefing on the cryptobanking plumbing and market pulse.

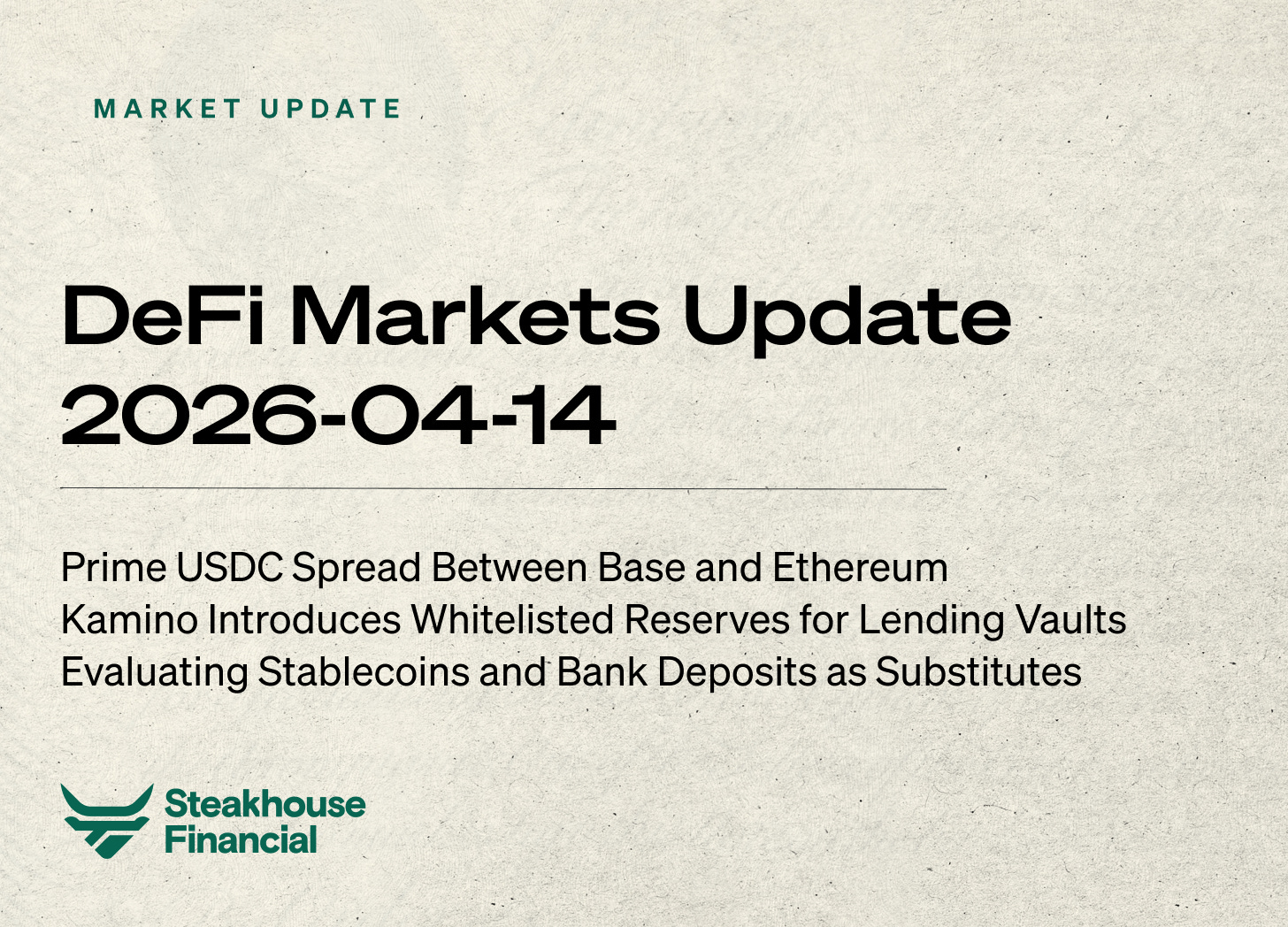

Prime USDC Spread Between Base and Ethereum

After the drop in mid January, the APY spread between Prime USDC on Base and Ethereum Mainnet has widened to its highest level this year of 1.8% APY.

Lenders have rotated towards Base to capture the higher yield, but the spread has still persisted. That suggests fresh supply is still being absorbed efficiently instead of fully arbitraging the gap away.

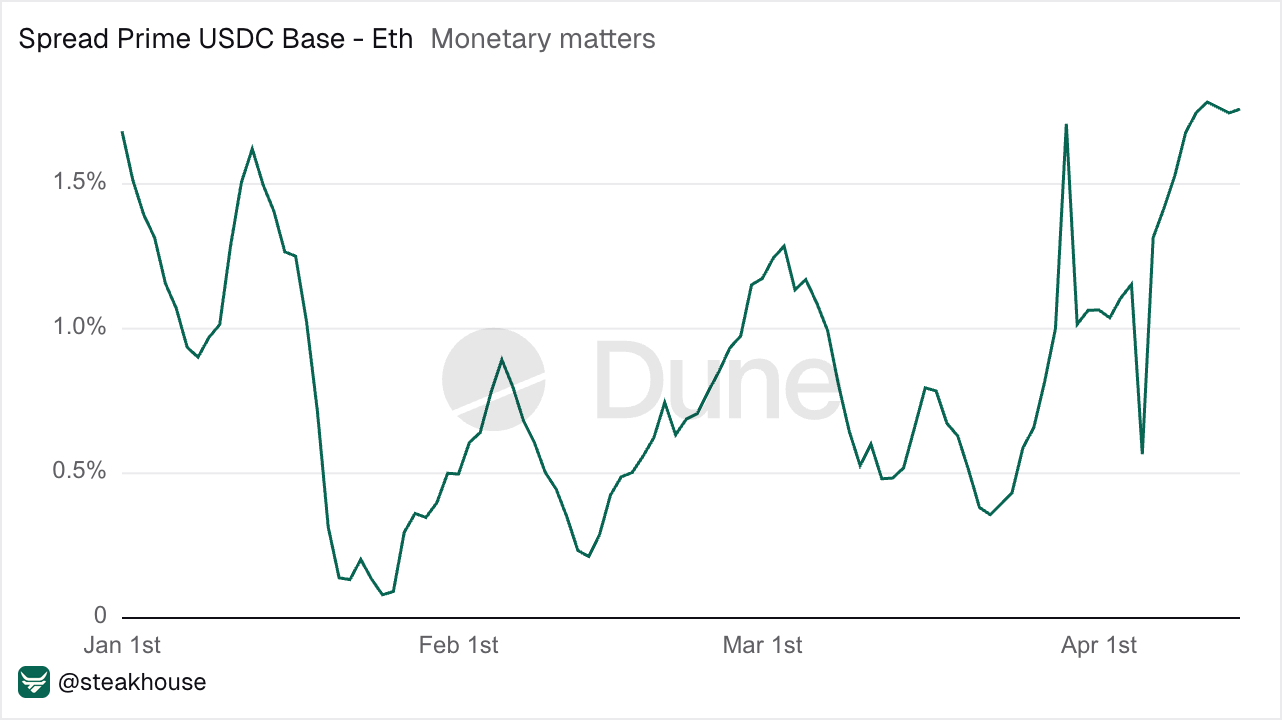

That divergence lines up with the underlying market activity. USDC borrowing demand is stronger on Base, especially in the large BTC-backed markets (Coinbase Borrow product). The cbBTC/USDC market on Base stands at $1.18B and grows, versus $310M on Ethereum which is shrinking with BTC price.

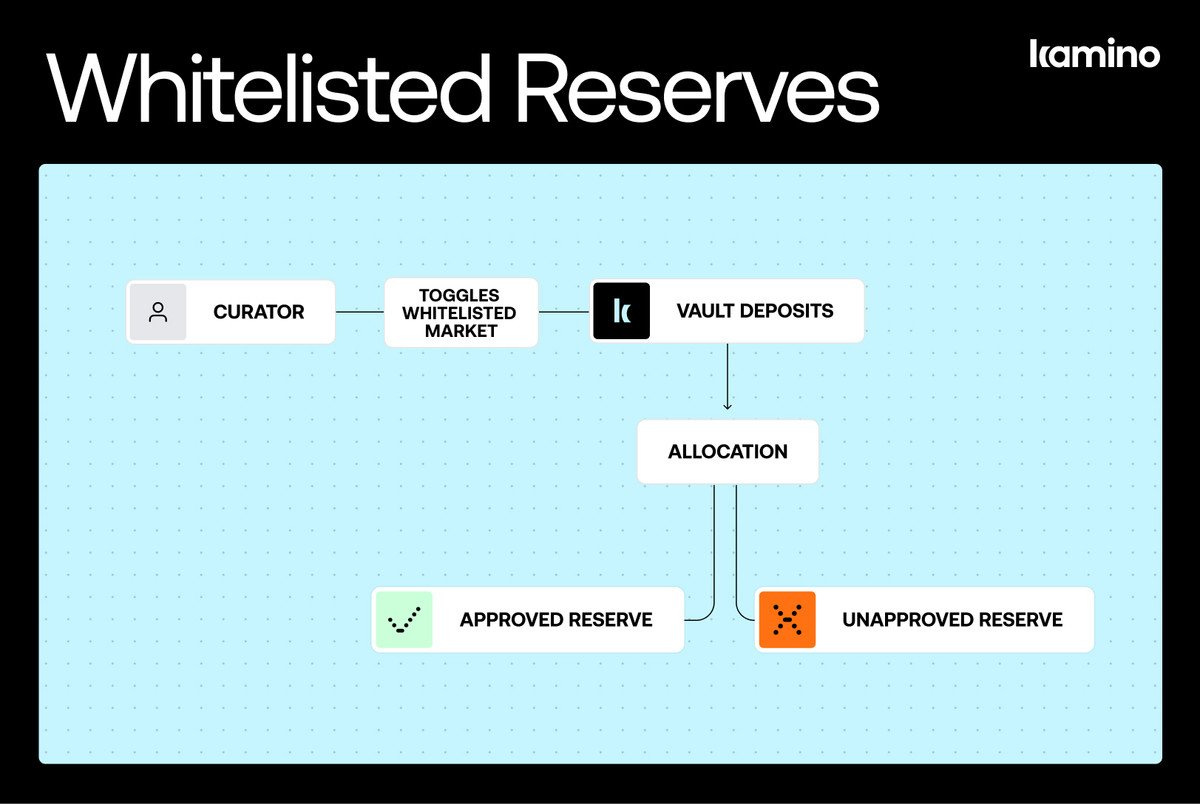

Kamino Introduces Whitelisted Reserves for Lending Vaults

Kamino introduced ‘Whitelisted Reserves’ for Lending Vaults, an irreversible smart contract setting for the curator that limits vault allocations and investments to reserves verified by the platform, and it is now enabled on all vaults shown on Kamino’s UI.

In practice, being whitelisted means vault capital is restricted to a protocol-level list of approved reserves maintained by Kamino, while curators can still manage allocations across those approved reserves. This gives depositors an extra protocol-level security layer around where vault capital can be deployed.

The change adds two onchain controls: one blocks new allocations to non-whitelisted reserves, and the other blocks depositor funds from flowing into non-whitelisted reserves; both should be enabled together for full coverage.

The main benefit is that a compromised vault admin key cannot redirect funds into a fake or unvetted reserve, which reduces the chance of depositor capital being drained through that attack path and strengthens the security of the vault structure.

Withdrawals remain available regardless of whitelist status, curators can still de-allocate from reserves, and depositors can still enter or exit subject to available liquidity, so the change improves deployment controls without disrupting the withdrawal path.

Evaluating Stablecoins and Bank Deposits as Substitutes

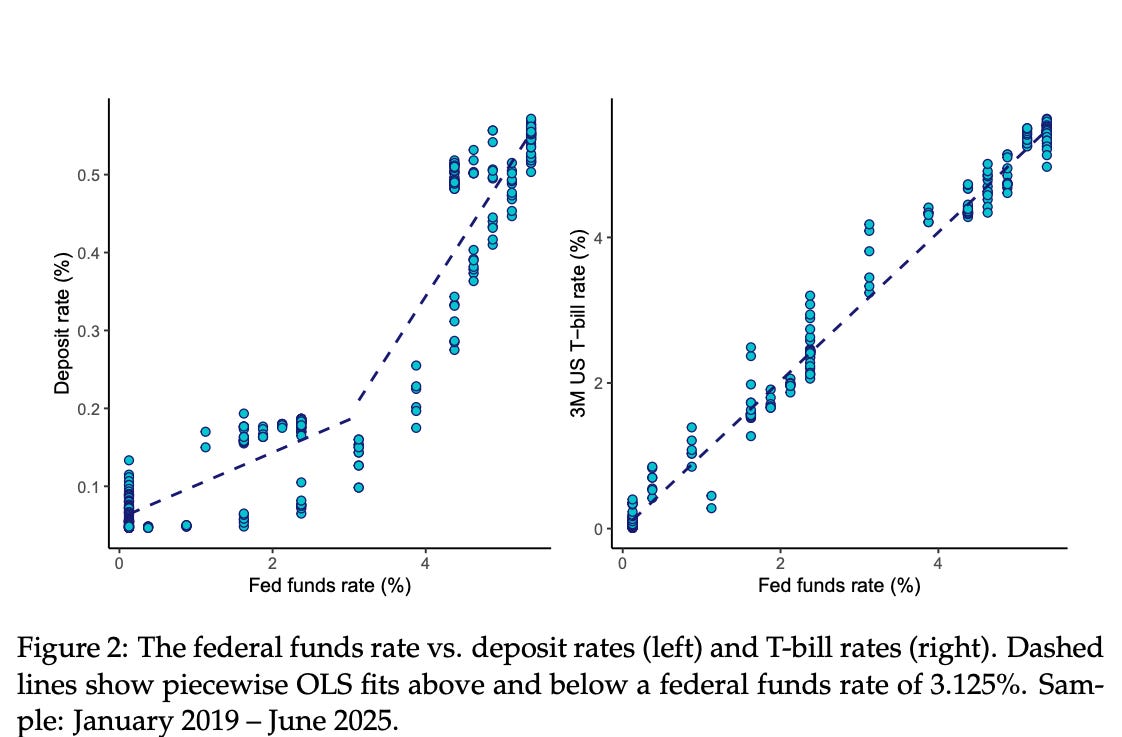

Stablecoin and bank deposit demand may overlap, especially when users are deciding where to park dollar balances. To evaluate that idea, we can look at the March 2026 paper by Rashad Ahmed and Inaki Aldasoro, Are Stablecoins and Bank Deposits Substitutes?, which studies whether these money-like dollar instruments compete for the same pool of cash, using weekly U.S. data from January 2019 to June 2025.

The authors’ mechanism is that deposits and stablecoins both serve money-like functions, so users can shift between them when relative attractiveness changes. Once Fed rates move above circa 3.125%, banks start passing more of those increases through to depositors, which is the key pattern they use to isolate deposit repricing shocks that are associated with slower stablecoin market cap growth.

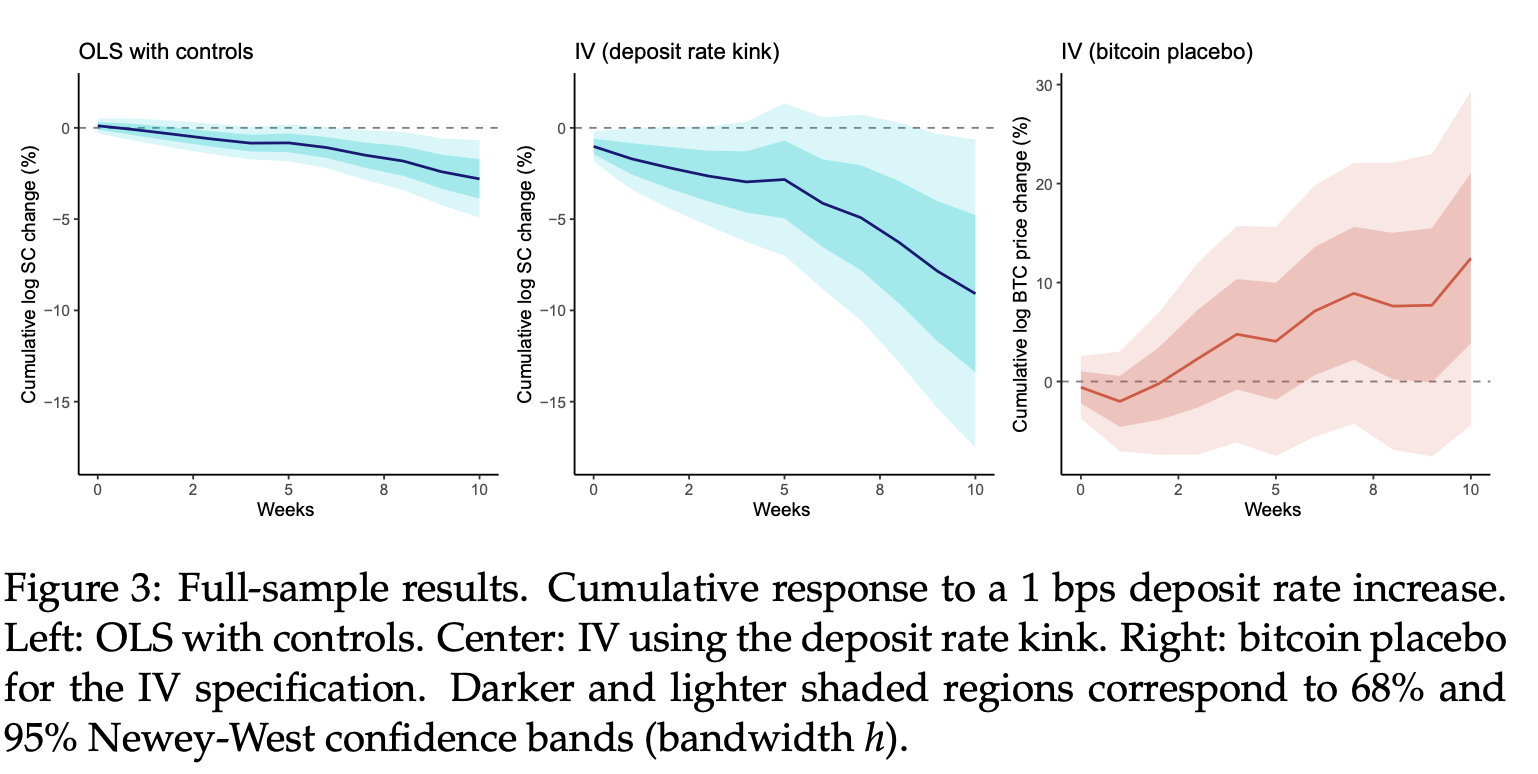

They test this in two steps. First, they run an Ordinary Least Squares (OLS) regression, which uses the raw observed relationship between weekly deposit-rate changes and stablecoin growth. They then add an Instrumental Variables (IV) approach, which uses the deposit-rate kink in Figure 2 to isolate the part of deposit-rate moves that comes from banks passing through more of Fed tightening once rates are above about 3.125%. Both estimates are negative, implying weaker growth in reserve-backed stablecoin market capitalisation after deposit rate increases, not necessarily an outright decline in supply.

On the right of Figure 3, the authors run a bitcoin placebo within the IV framework to test whether the result is specific to stablecoins instead of reflecting a broader crypto or macro cycle. Because BTC does not serve the same money-like role as reserve-backed stablecoins, a significant BTC response would weaken the substitution interpretation. The paper finds no statistically significant BTC response, which the authors treat as supportive of a stablecoin-specific effect.

The BTC placebo result should be read carefully. Zero stays within the 95% confidence band throughout the horizon, which means the BTC estimate is not statistically distinguishable from zero at that level. It does not mean the BTC effect is precisely estimated at zero, since the confidence bands remain wide across the horizon.

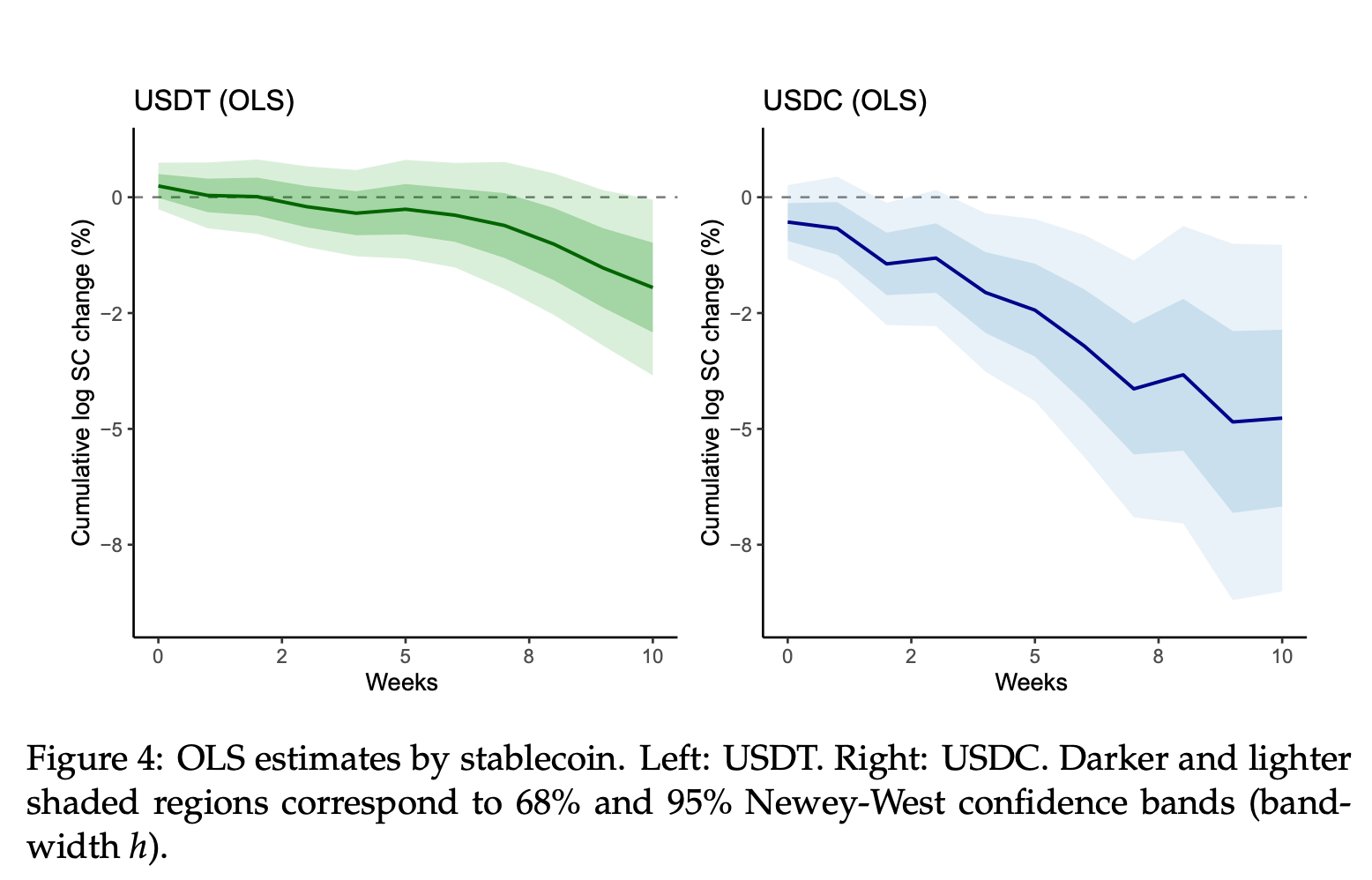

Moreover, the paper also finds a stronger effect for USDC than for USDT, which the authors interpret as consistent with USDC’s closer links to U.S. institutional and DeFi users, while USDT demand is more associated with offshore and emerging-market usage.

Overall, the paper supports a plausible substitution narrative between bank deposits and stablecoins, but the evidence is concentrated in a specific U.S. high-rate setting and is stronger for some parts of the market, especially USDC, than for the stablecoin sector as a whole.