DeFi Markets Update 2026-02-25

DeFi Rate vs SOFR, wstETH/ETH Looping, Yields on Kamino

Welcome to another DeFi Markets Update—your no-nonsense briefing on the cryptobanking plumbing and market pulse.

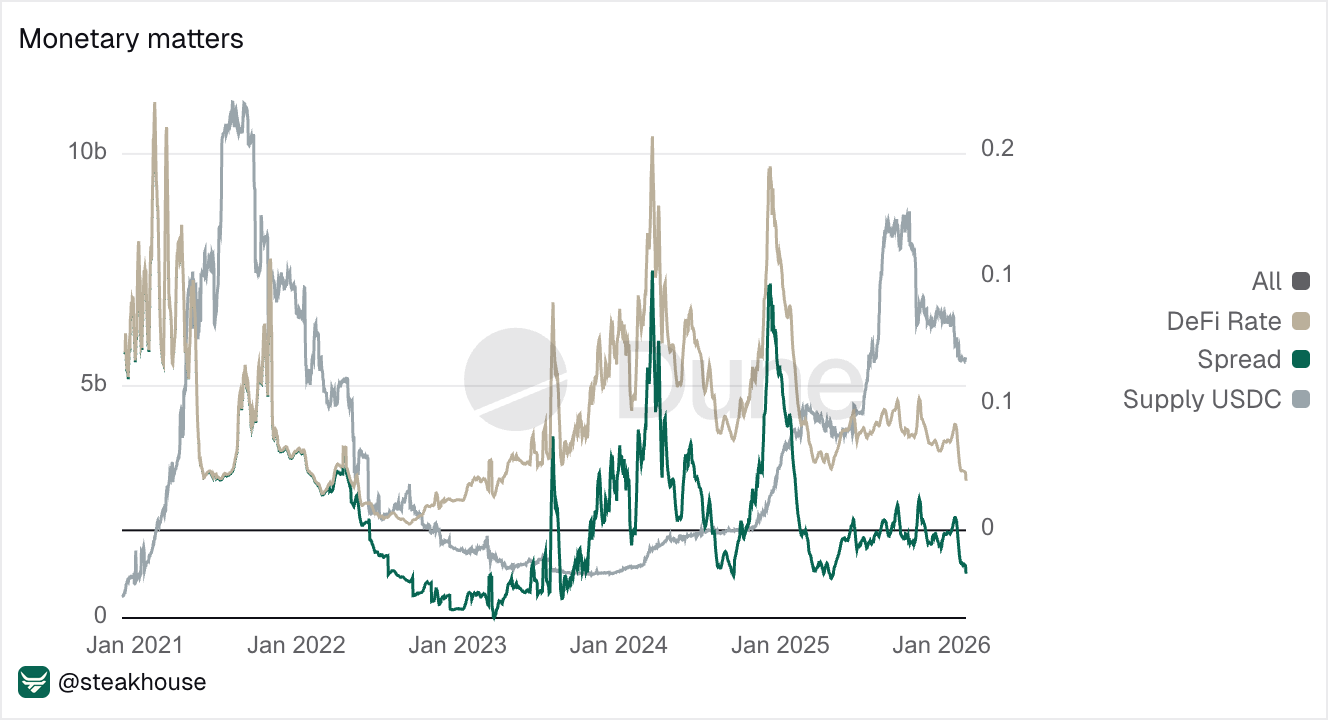

DeFi rates converging with SOFR despite different risk profiles

While historically uncorrelated, DeFi lending rates and SOFR have been converging since early 2025. The spread between the two was all over the place through 2021–23 but now tracks near zero, despite USDC supply fluctuating and SOFR moving from 4.3% to 3.6% in the past year.

Rate convergence with a risk-free benchmark (SOFR) is typically what you see as a market develops deeper liquidity, more sophisticated participants, and better pricing infrastructure.

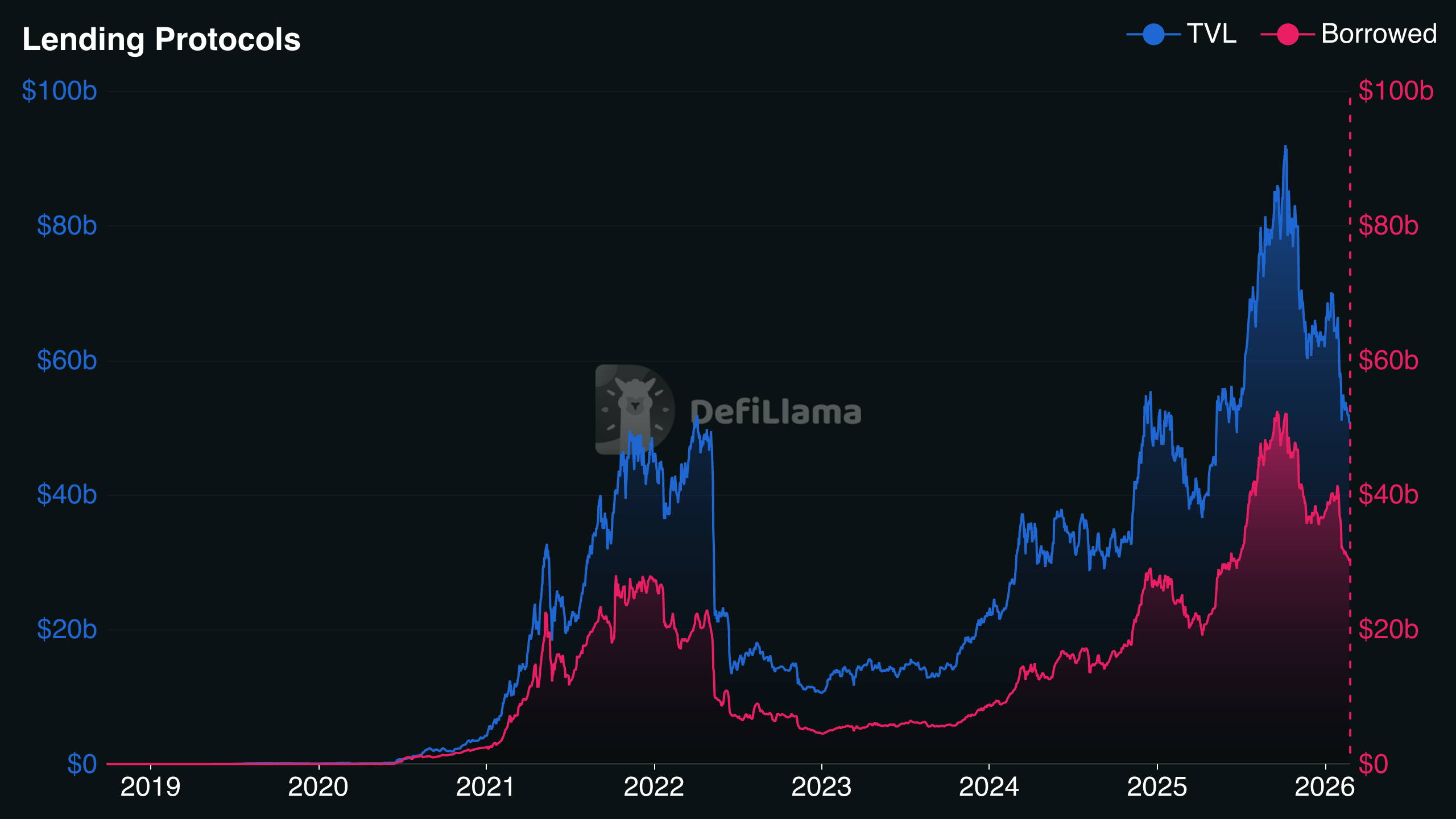

DeFi lending TVL has grown to $50B+, with institutional allocators now active across Aave, Morpho, and Compound, making it a structurally different market from 2021.

Tokenized money markets are driving convergence from the TradFi side. For example in 2025, Sky’s Spark allocated $1B to tokenized Treasuries, including $500M to BlackRock’s BUIDL, which is now around $2.6B AUM across eight chains. As T-bills become DeFi collateral, the gap between the “risk-free rate” and the “DeFi rate” keeps narrowing.

However, risk profiles haven’t converged. SOFR is overnight, Treasury-collateralised, and centrally cleared via FICC (near-zero credit risk), while DeFi lending is crypto-collateralised, smart-contract-intermediated, and exposed to oracle, liquidation, and depeg risks. So why is the spread converging if the risks still differ?

The compression likely reflects frictions (gas, bridging, off-ramp delays) that make on-chain capital sticky, plus persistent stablecoin demand in regions with limited dollar banking (e.g. stablecoin holdings relative to bank deposits increased from near 0 to 2.5–3% within 4 years in Latin America as mentioned in our last update), which isn’t directly arbitrageable against TradFi.

In equilibrium, DeFi rates should sit above SOFR to compensate for its specific risk stack. A near-zero spread suggests either the market is underpricing DeFi risk or structural demand frictions are compressing it artificially. More on the spread yield decomposition soon!

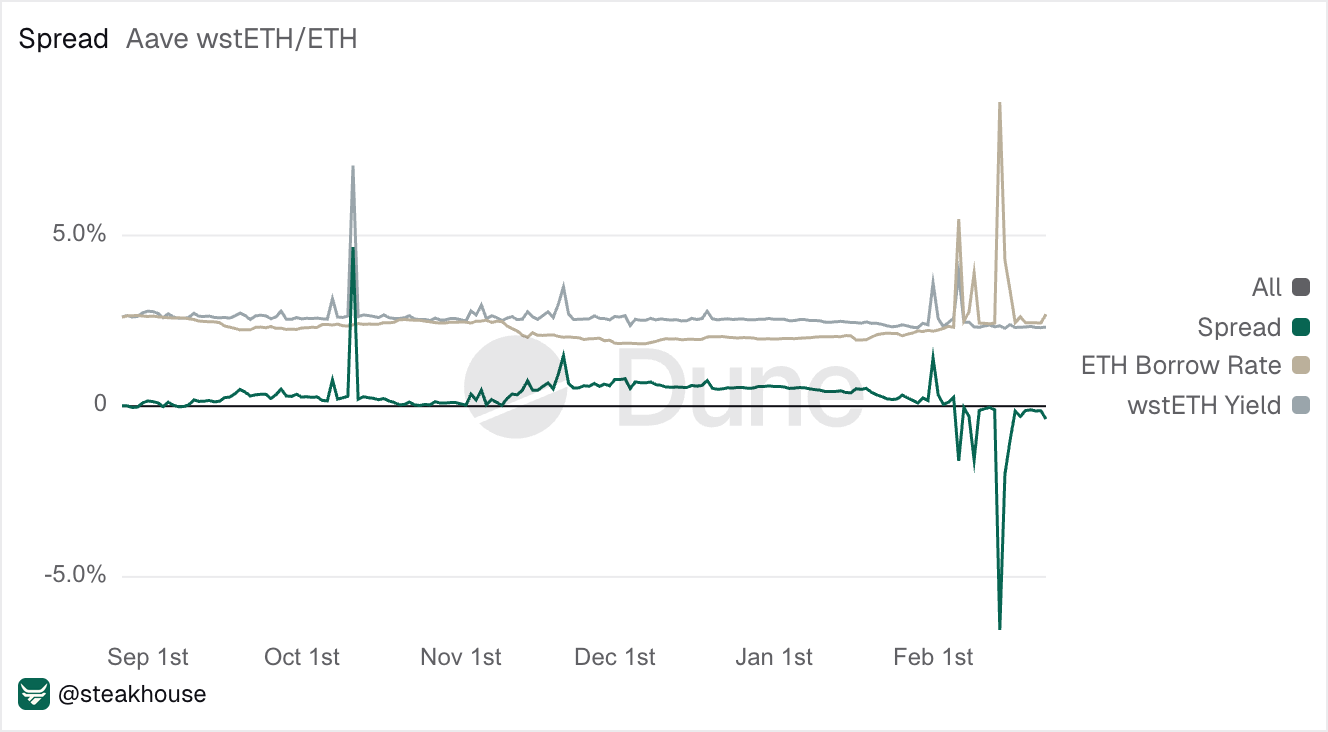

wstETH/ETH Looping: Flat Carry with Fat Tails

wstETH/ETH looping on Aave v3 Mainnet has been barely profitable over the past 6 months, with the strategy running at roughly breakeven as ETH borrow rates hover around 2–3% against wstETH yield of 2.5–3%.

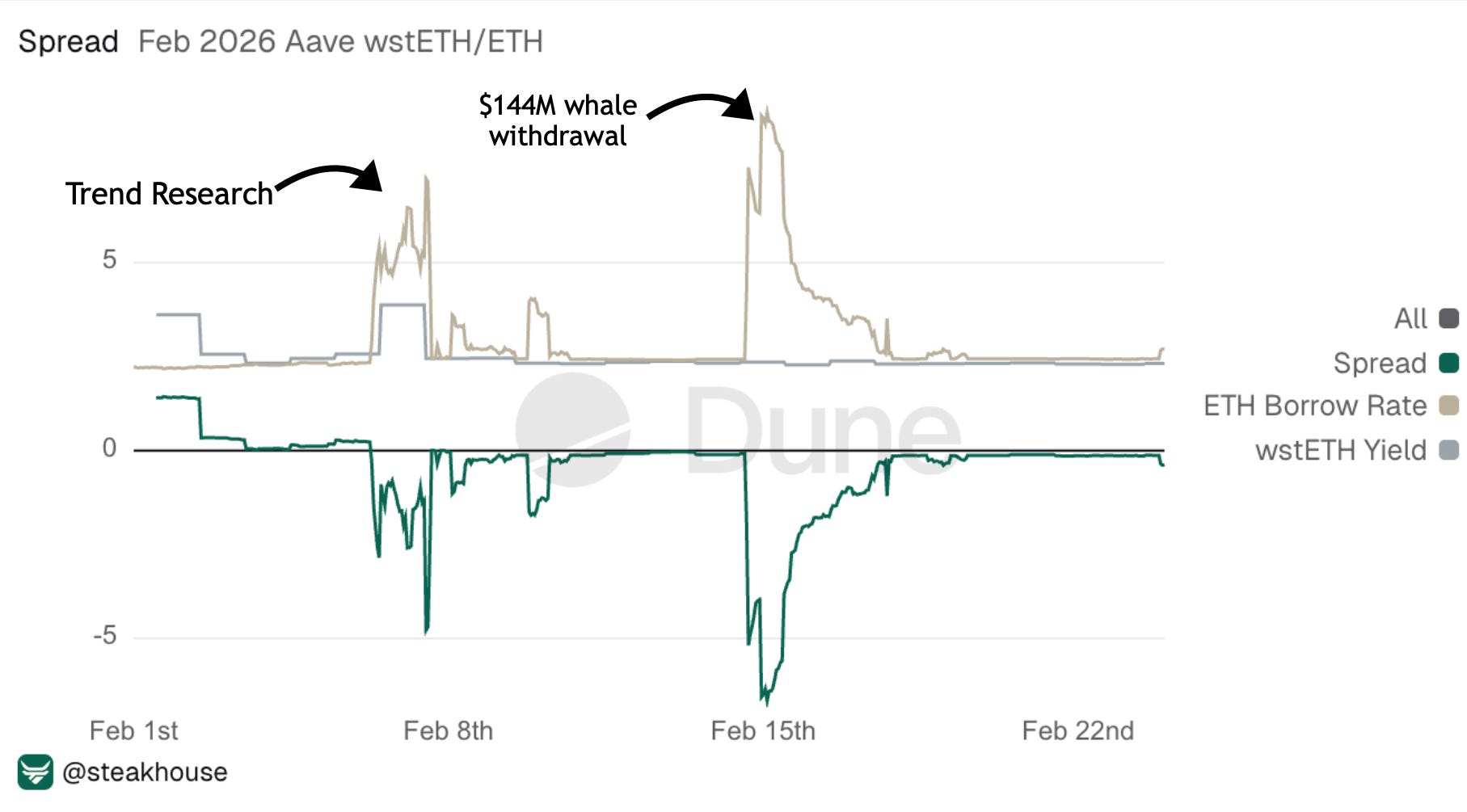

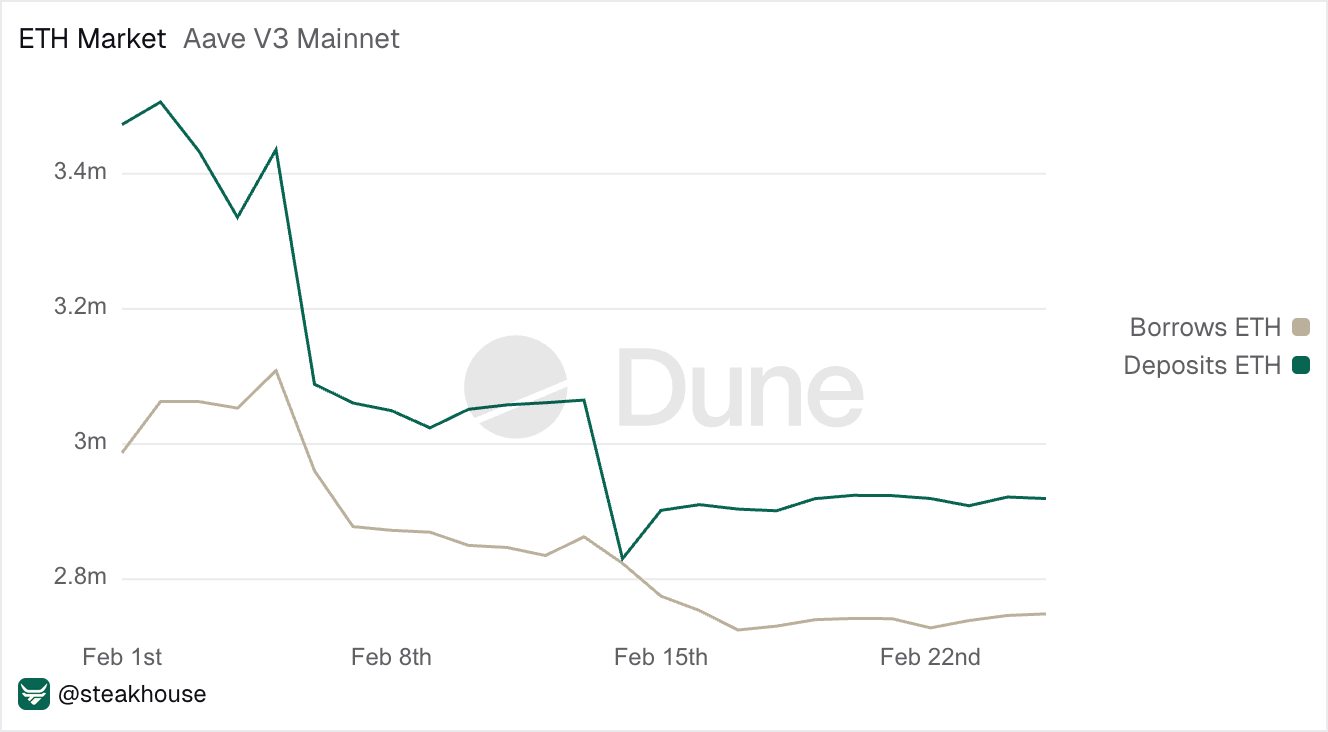

The WETH borrow rate spiked twice in February. The first spike (utilisation to 95.4%) was driven by Trend Research’s ~$2B leveraged ETH long on Aave, as ETH/USDT positions were unwound and 332k ETH were sold to repay their stablecoin debt. This deleveraging drained Aave’s ETH pool, spiking WETH borrow costs and reducing liquidity for the wstETH/ETH loop.

The second spike (utilisation to 99.85%) came when a $144M whale withdrawal hit an already thin pool. At both peaks, the wstETH/ETH carry spiked deeply negative.

Deposits dropped from 3.45M to 2.9M ETH in the first week of February as Trend unwound, compressing liquidity and pushing borrow rates up. The first spike resolved as borrows subsided and repayments outpaced withdrawals, gradually stabilising the pool’s liquidity. The second spike resolved through a combination of fresh deposits entering the pool and further borrow reductions.

Yields on Kamino

Steakhouse USDC High Yield on Kamino is currently earning circa 5% APY.

Utilisation sits at 89%, meaning most supplied USDC is actively deployed. Around 60% of the vault is allocated to the OnRe Market, the primary driver of the current yield.

OnRe is a Bermuda-licensed reinsurance platform bringing the $750B global reinsurance market on Kamino. ONyc generates yield from diversified underwriting performance and collateral income which is a return source that is structurally uncorrelated to crypto markets. NAV is priced in real time via Chainlink Data Streams, and independently attested by Apex.