($238m) Liquidations of Onchain Lending

What onchain lending's stress test revealed

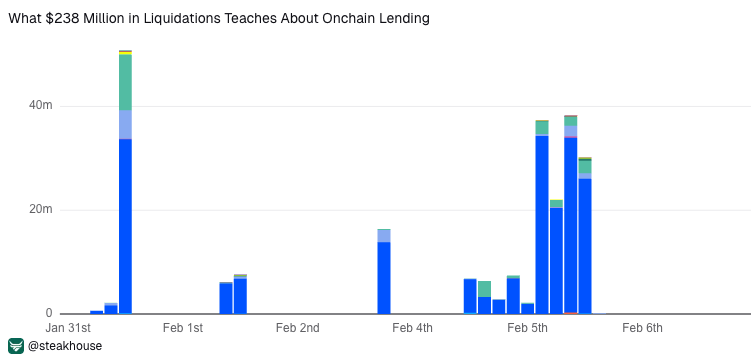

Between January 31 and February 6 2026, Morpho processed approximately $238 million in liquidations during one of the sharpest market drawdowns of the current cycle. Users of Steakhouse vaults experienced zero bad debt events and all our vaults maintained 100% liquidity throughout. This piece digs into how onchain liquidations work, why they concentrate in BTC-collateralized markets, and what the events of the last few weeks prove (or not) about onchain lending infrastructure.

This analysis reflects data available as of February 10, 2026.

Between late January and early February 2026, onchain credit markets experienced one of the sharpest drawdowns of the current cycle. BTC fell 17% over the week and ETH dropped 26%, with February 5 the worst single day at 14% and 15% respectively. This is already on the back of a precipitous contraction in October and another in November.

Across Morpho, approximately $238 million in borrower positions were liquidated in that period. Despite the extreme volatility, users of Steakhouse vaults, allocating to overcollateralized loan positions, absorbed no bad debt and always retained enough liquidity to withdraw their deposits if desired.

Liquidations are a crucial component of onchain lending. Market incentives wholly determine the way onchain repo markets work. Lenders are incentivized by the opportunity to earn an attractive return, secured by a buffer of overcollateralization. When too much liquidity enters the market, interest rates tend to decline either to incentivize lenders to leave or borrowers to borrow. When too little liquidity is available, interest rates tend to increase either to attract more lenders or incentivize borrowers to repay. When a loan position crosses ‘the line’ and hits a liquidation threshold, the smart contracts seize the collateral and auction it at a discount to incentivize arbitrageurs to cure the loan and safeguard lenders.

Liquidations are profitable for arbitrageurs, are loss-making for borrowers, and ensure lenders remain whole. When the price of borrower collateral rapidly declines, it is quite common for positions to become rapidly liquidatable. The distinction between borrower and lender profitability matters, and this piece explains why.

How liquidations actually work in Morpho markets

Morpho is a permissionless lending protocol where each lending market is isolated and parameterized. A single market pairs one collateral asset against one loan asset (e.g., cbBTC/USDC) with a defined liquidation loan-to-value threshold (LLTV), the maximum ratio of borrowed value to collateral value at which a position remains healthy. Above that line, the position is eligible for liquidation.

Steakhouse vaults offer curated but noncustodial reallocations across multiple Morpho markets. When users deposit USDC into a Steakhouse vault, they are lending capital to borrowers across all the markets the vault allocates to. The vault curator decides which markets to include and how to weight them. The borrowers in those markets post collateral and accrue interest for access to that capital.

Steakhouse Prime vaults allocate to blue-chip collateral markets only: generally high-quality tokenized Bitcoin, various flavors of ETH and, depending on rates, investment grade tokenized securities such as money market funds. BTC collateral markets generally operate at an 86% LLTV. A borrower who deposits $100 worth of cbBTC can borrow up to $86 in USDC before getting liquidated. If the price of cbBTC drops enough that the debt exceeds 86% of the collateral’s current value, third-party liquidators can repay part of the debt and seize a corresponding portion of the collateral plus a bonus on seized assets. The lender gets their principal back plus accrued interest and the liquidator keeps the spread.

This is the onchain equivalent of a margin call. The smart contract enforces the threshold automatically and the open liquidation market clears the position. Credit risk is bounded by the LLTV parameter and the speed of liquidation execution, not by the creditworthiness of the borrower.

Why the liquidations concentrate where they did

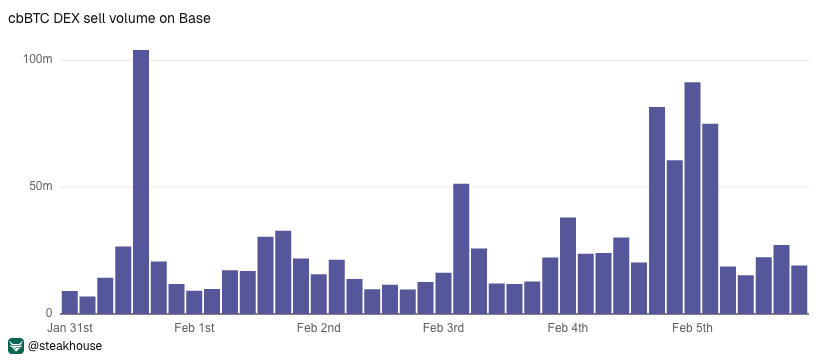

The largest Steakhouse vaults on Morpho share a common trait: heavy allocation to BTC collateral markets. The Steakhouse Prime USDC vaults on Base (over $750 million in deposits) allocates over 95% to the cbBTC/USDC market. The Ethereum Prime vault ($357 million) allocates roughly 95% to cbBTC and WBTC combined.

Combined, these three vaults hold over $1 billion in deposits with BTC collateral accounting for the vast majority of exposure. When BTC drops 17%, this is where liquidations happen. The arithmetic follows directly from the collateral composition.

The Coinbase integration in particular functions as what one might call a “DeFi mullet,” a fintech user experience in the front, powered by immutable smart contracts in the back. Coinbase users access a familiar lending interface. Under the hood, their USDC is deployed into noncustodial wallets that interact with Morpho markets where borrowers post cbBTC as collateral. Interest accrues in real time, and liquidations execute permissionlessly. The architecture performed as designed under stress.

What Steakhouse vault users experienced

Every Steakhouse vault continued to process withdrawals normally throughout the event. No queue, no gate, no delay. Users who wanted to exit could do so at any point.

Deposit behavior varied across vaults. The Coinbase vault on Base, with over 48,000 depositors, saw a steady decline from $360 million on January 31 to $298 million by February 10, a 17% outflow over eleven days. The largest single-day withdrawals came on February 5 and 6 ($16.6 million and $15 million respectively), coinciding with the sharpest price drops. These are rational responses from depositors who could exit at any time and chose whether to do so. The vault saw its first net positive flow on February 11.

The motivation of lenders appears to be largely yield-sensitive. Our vaults integrated by Coinbase saw APY compress from 3.13% to 2.71% over the period, a decline of 38 basis points. The dynamics are mechanical: when borrowers get liquidated, outstanding borrow demand decreases. Less demand for borrowed capital means lower rates for lenders. The yield compression post-crash is a live view of the market incentives playing out to normalize the lending market. Utilization rates (the proportion of liquidity in the repo markets being borrowed) settled around 80%, well within normal operating range with ample withdrawal capacity. Morpho’s repo markets are designed to seek equilibrium at around 90%.

Collateral segmentation: the Steakhouse High Yield experience

The clearest evidence that vault construction drives outcome under stress comes from comparing Prime and Smokehouse.

Steakhouse High Yield vaults allocate predominantly across markets collateralized by a wider range of collateral, such as yield-bearing stablecoin aggregators: sUSD, syrupUSDC, wsrUSD, and similar assets. The Ethereum High Yield vault ($73 million in current deposits) has less than 1% sitting in a cbBTC-collateralized market. LLTV parameters on stablecoin-aggregator markets are set at 91.5%, higher than Prime’s 86% on BTC markets, because, by being indexed to USD, these collateral types are not designed to experience price volatility.

During the February event, the stablecoin-aggregator collateral that constitutes the vast majority of the vault’s allocations did not reprice when BTC moved. The vault experienced no liquidation pressure from the drawdown. The vault did see modest outflows and yield compression through the period, consistent with reduced borrowing demand across the broader market.

The Prime/High Yield divergence is an illustration of the Morpho onchain repo system working as intended. Prime earns yield from borrowers who generally want leveraged exposure to BTC and ETH. Those borrowers pay interest against their loans, and they bear the liquidation risk. The High Yield vault earns yield from a different borrower profile: carry traders, structured position managers, and stablecoin protocol treasuries borrowing against yield-bearing stable assets. Different collateral, different borrower, different risk, different behavior under stress. Morpho’s isolated market design keeps both verticals from interacting adversely with each other.

The higher LLTV on stablecoin-derivative markets carries its own risks, as the November 2025 Stream Finance depeg demonstrated when several Morpho curators incurred bad debt on depegged collateral that Steakhouse vaults had no exposure to.

Risk cannot be removed, but hard cryptographic constraints can help manage them more transparently. Choosing between Prime and High Yield vault is a collateral-risk decision, and the events of February demonstrated what that decision looks like when tested.

What this event validates, and what it does not

The February liquidation event validated several properties of onchain lending infrastructure that are often asserted but rarely tested at scale.

Overcollateralization bounded lender losses to zero. Every liquidated borrower had posted collateral worth more than their outstanding debt. The 86% LLTV on Prime vaults created sufficient margin for orderly unwinding even during a 17% weekly BTC drawdown. Between January 31 and February 6, $234 million in Steakhouse vault liquidations ($238 million protocol-wide) did not generate any bad debt.

Permissionless liquidation markets cleared risk in hours, not days. Steakhouse vaults processed $108.5 million in liquidations on February 5 alone, demonstrating that open liquidation incentives attract sufficient third-party capital to process large volumes quickly.

Vault-level liquidity held under stress. Across nearly $1.7 billion in Steakhouse deposits, every vault maintained full redeemability. Morpho TVL protocol-wide declined from roughly $6.5 billion to under $5 billion at the trough before recovering to $5.8 billion. The protocol absorbed a 25-30% TVL contraction and continued operating normally.

Onchain lending is not without risk. Smart contract risk persists. Oracle risk persists. And the quality of the curator sitting between the protocol and the lender determines whether those risks are managed or ignored. Collateral underwriting, LLTV calibration, and real-time monitoring, are not features that come standard. They are decisions a curator makes before a single dollar is deposited, and they are the decisions that significantly influence whether a drawdown produces bad debt.

Liquidations are part of how overcollateralized lending works. To date, no lender in a Steakhouse vault has ever incurred bad debt on Morpho. While not a guarantee about the future, it is nonetheless a track record built on disciplined adherence to a risk management framework that prioritizes collateral underwriting and risk parameter discipline.

What to watch

Borrowing demand remains subdued. Prime USDC APYs have compressed to the 2.5-3.3% range, reflecting cautious leverage appetite in the aftermath. With the effective Fed Funds rate at 3.64%, onchain USDC lending rates currently sit below the risk-free rate, a reflection of the post-liquidation deleveraging across the market.

When leveraged positioning rebuilds, rates will follow. For now, the market is in a healthy deleveraging phase, and yields reflect that reality.

For more detail on Steakhouse vaults, risk parameters, and real-time monitoring, consult our Information Hub.

This content is for informational purposes only and does not constitute financial advice. DeFi lending involves risks including smart contract risk, collateral volatility, oracle risk, and liquidity risk. Past performance and historical yields are not indicative of future results. Users should conduct their own research and assess their risk tolerance before depositing into any vault product.